Usha 2024 – Class 12

Usha-2024-Part I – Solution

Usha-2024-Part II – Solution

Book Solutions

Class +1 – Accountancy

Usha Publication Book’s Solution – PSEB

Unimax Publications Book’s Solution – PSEB

D K Goel Book’s Solution – ISC

T.S. Grewal’s Book’s Solution – CBSE

Class +2 – Accountancy

Usha Publication – Part I – Solution

Usha Publication – Part II – Solution

Unimax Publications Part 1 – Solution

Unimax Publications Part 2 – Solution

T.S. Grewal’s Book Part – A Vol. I – Solution

T.S. Grewal’s Book Part – A Vol. II – Solution

T.S. Grewal’s Book Part B – Solution

V K Publications Part B– Solution

Video Lectures

Video Lectures Class 11

Accounts

Business Studies

Economics

Video Lectures Class 12

Accounts

Business Studies

Economics

Store

Goods and Services Tax (GST)

Ads loading…

GST Invoice Format 3.0| Free Dynamic Excel sheet

Place of Supply of Services under GST

Place of Supply of Goods under GST

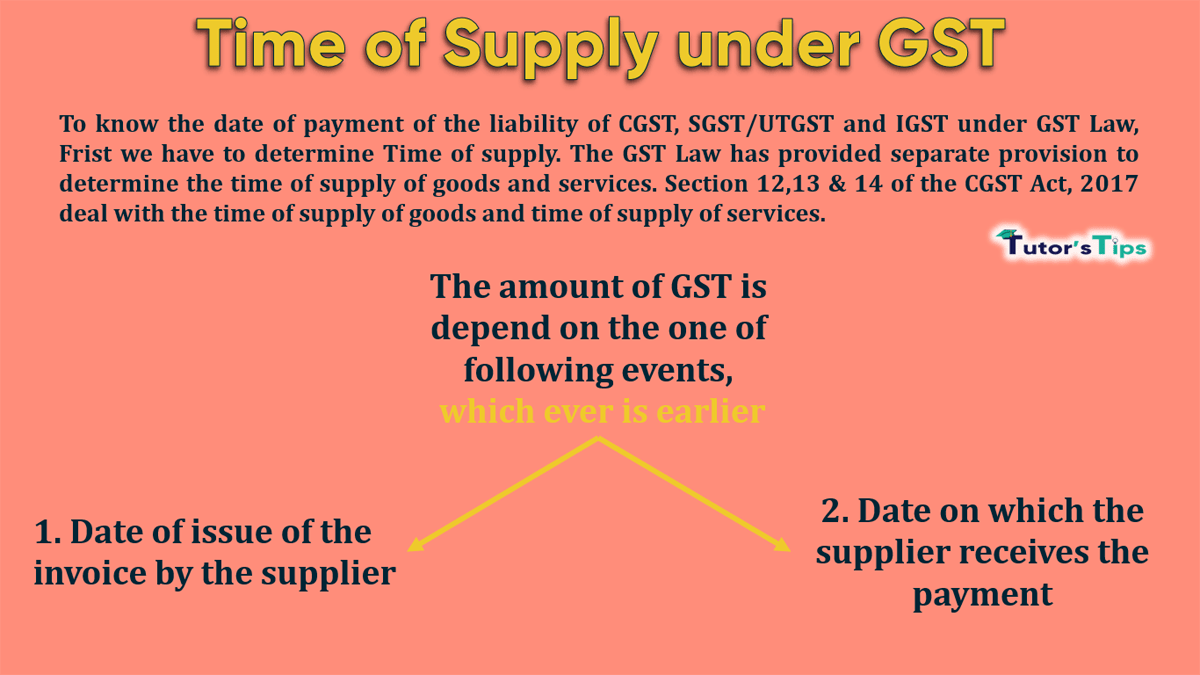

Time of Supply under GST

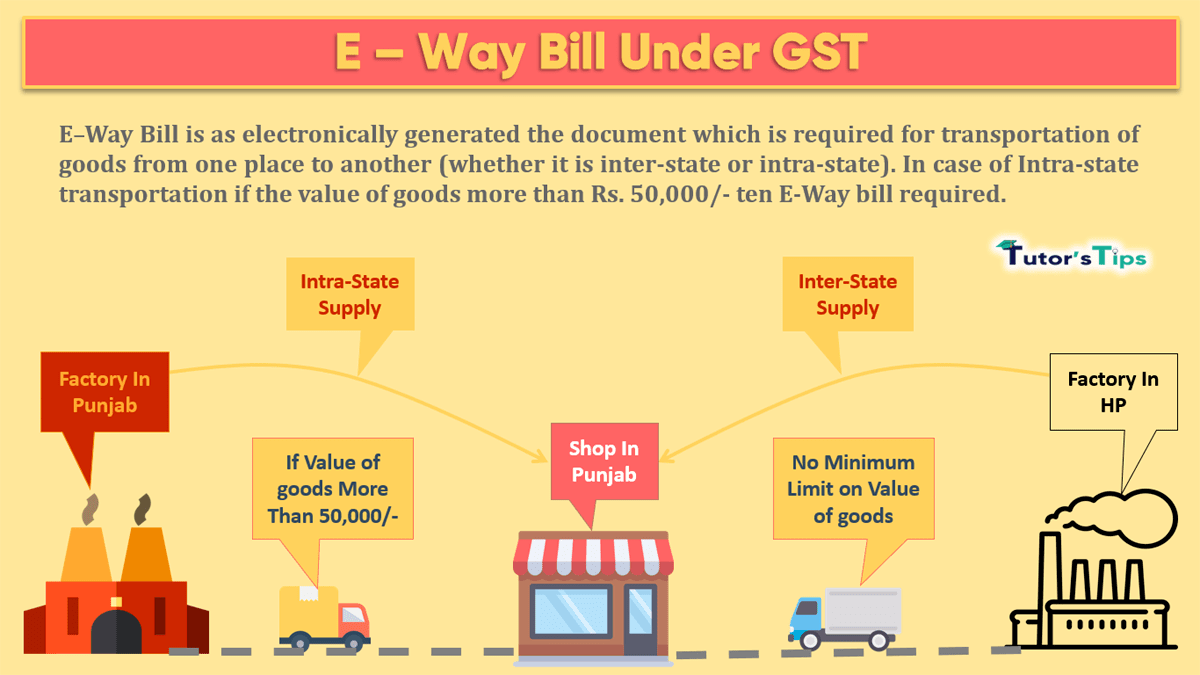

E–Way Bill under GST

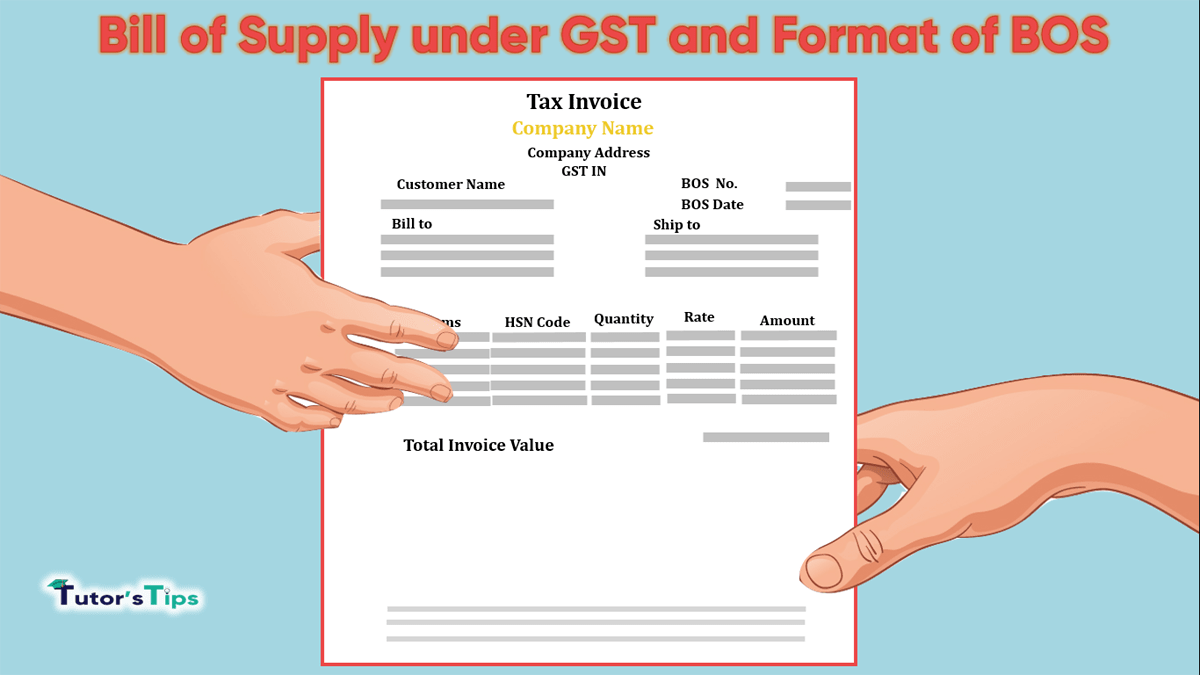

Bill of Supply under GST and Format of BOS

GST Invoice Format In India |Dynamic Excel sheet

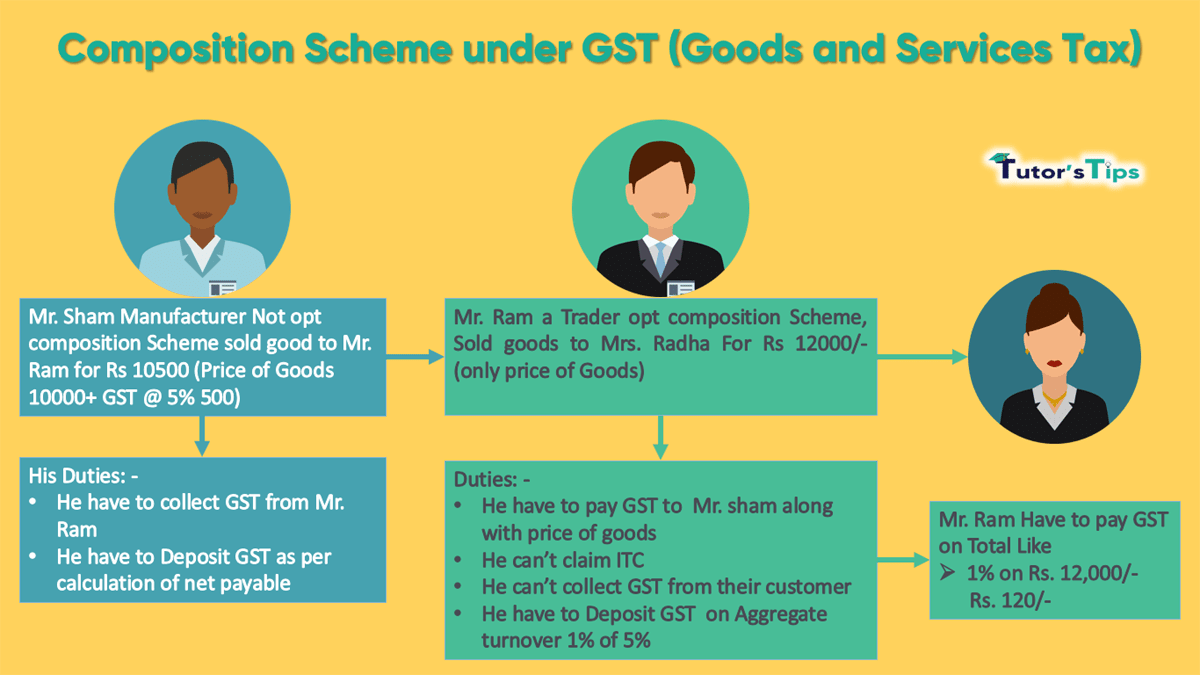

Composition Scheme under GST(Goods and Services Tax)

Exemption from GST Registration | Examples

Whom to Register under GST act 2017

Ads loading…

Advertisement

1

2

Crazy Pachinko bonus

statistiky Crazy Time

Crazy Time live Italia

Coin Flip Crazy Time

hur spelar man Crazy Time

Royal Reels casino

Crazy Time strategies UK

ATG App Sverige

error:

Content is protected !!