Usha 2024 – Class 12

Usha-2024-Part I – Solution

Usha-2024-Part II – Solution

Book Solutions

Class +1 – Accountancy

Usha Publication Book’s Solution – PSEB

Unimax Publications Book’s Solution – PSEB

D K Goel Book’s Solution – ISC

T.S. Grewal’s Book’s Solution – CBSE

Class +2 – Accountancy

Usha Publication – Part I – Solution

Usha Publication – Part II – Solution

Unimax Publications Part 1 – Solution

Unimax Publications Part 2 – Solution

T.S. Grewal’s Book Part – A Vol. I – Solution

T.S. Grewal’s Book Part – A Vol. II – Solution

T.S. Grewal’s Book Part B – Solution

V K Publications Part B– Solution

Video Lectures

Video Lectures Class 11

Accounts

Business Studies

Economics

Video Lectures Class 12

Accounts

Business Studies

Economics

Store

Financial Accounting

Ads loading…

Question 40 Chapter 2 – Unimax Class 12 Part 1 – 2021

Cheque : Meaning , Types and Explanation

Negotiable Instrument: Meaning and Explanation

Promissory Note: Meaning and Explanation

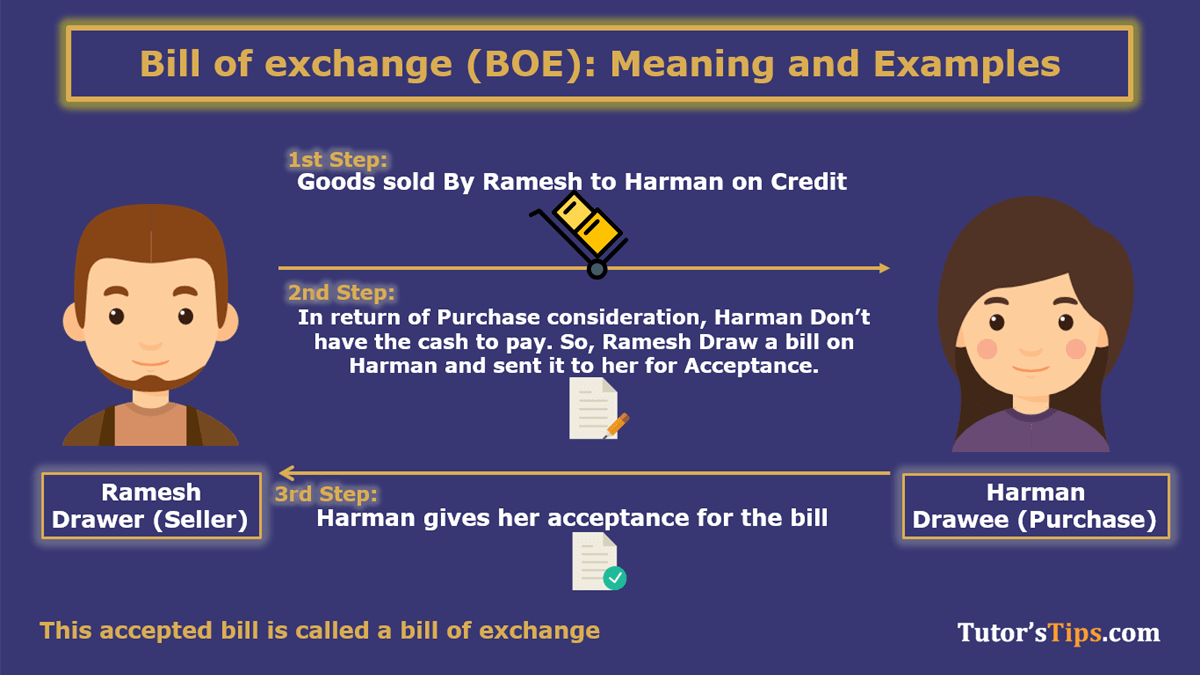

Bill of exchange (BOE): Meaning and Examples

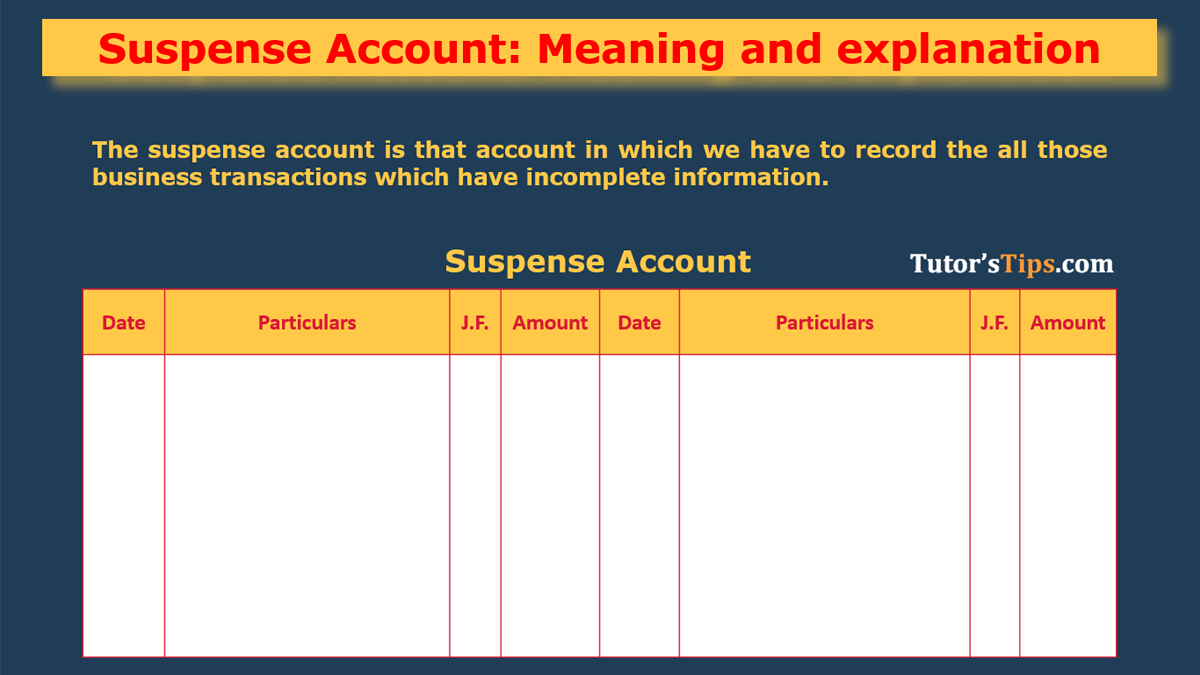

Suspense Account: Meaning and explanation

Error Rectification in accounting – Explanation with examples

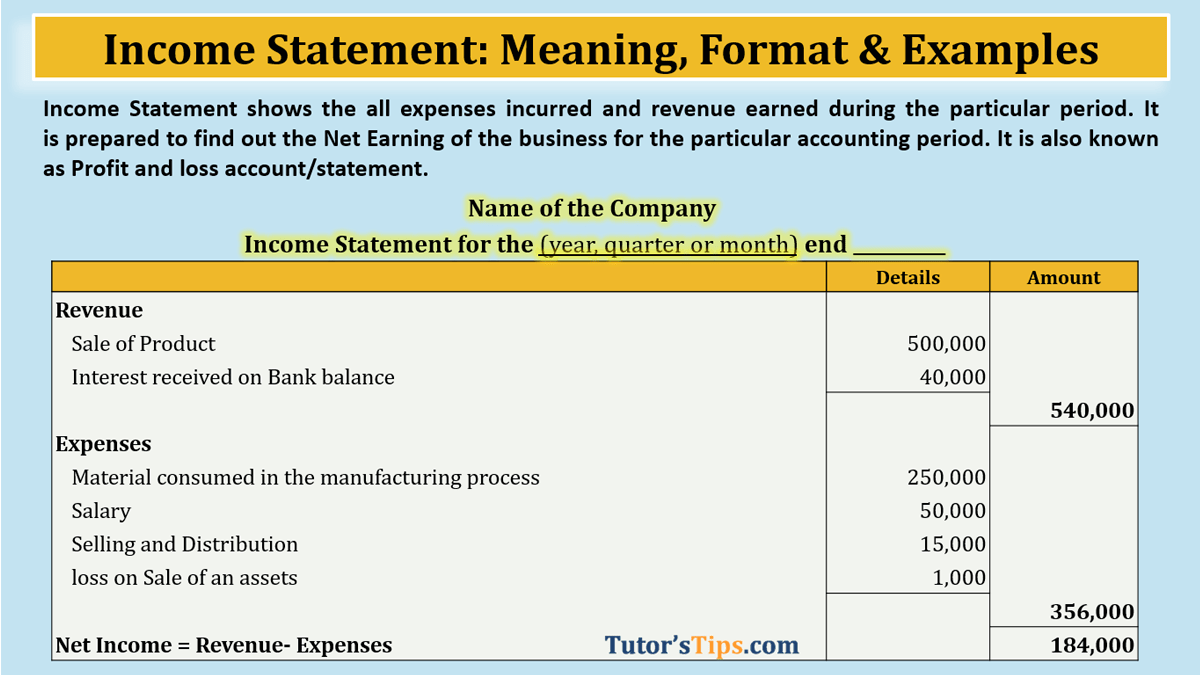

Income Statement: Meaning, Format & Examples

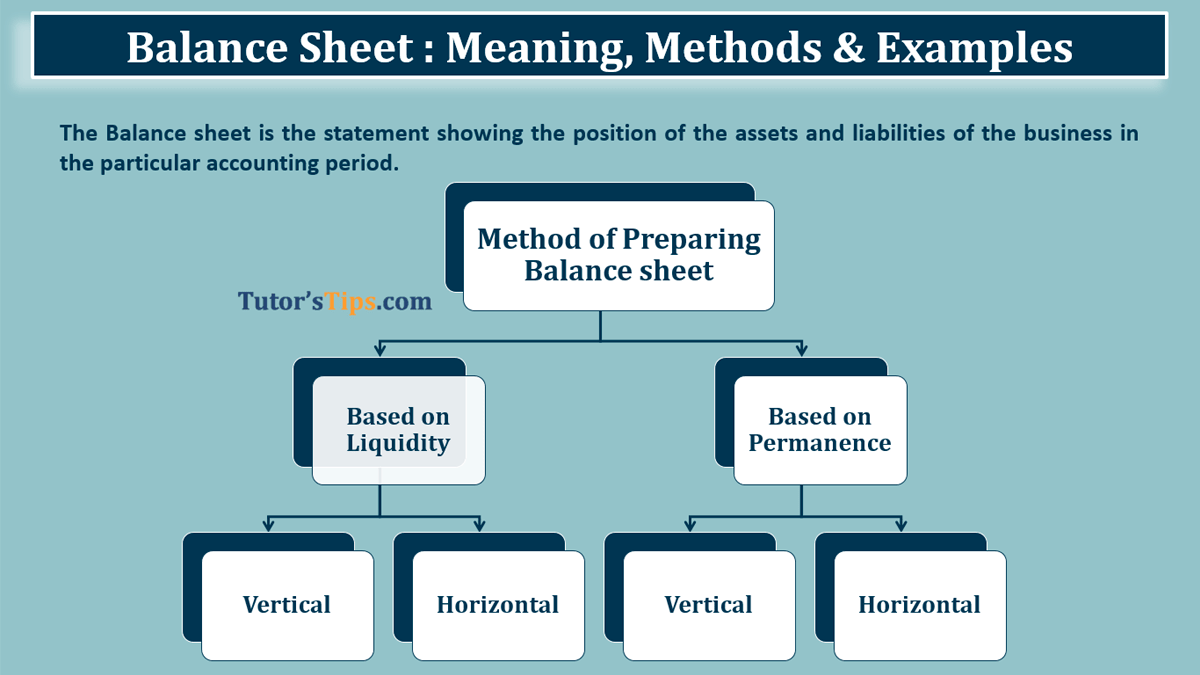

Balance Sheet: Meaning, Format & Examples

Profit and Loss Account: Meaning, Format & Examples

Ads loading…

Advertisement

1

2

…

7

Crazy Pachinko bonus

statistiky Crazy Time

Crazy Time live Italia

Coin Flip Crazy Time

hur spelar man Crazy Time

Royal Reels casino

Crazy Time strategies UK

ATG App Sverige

error:

Content is protected !!