Time of Supply

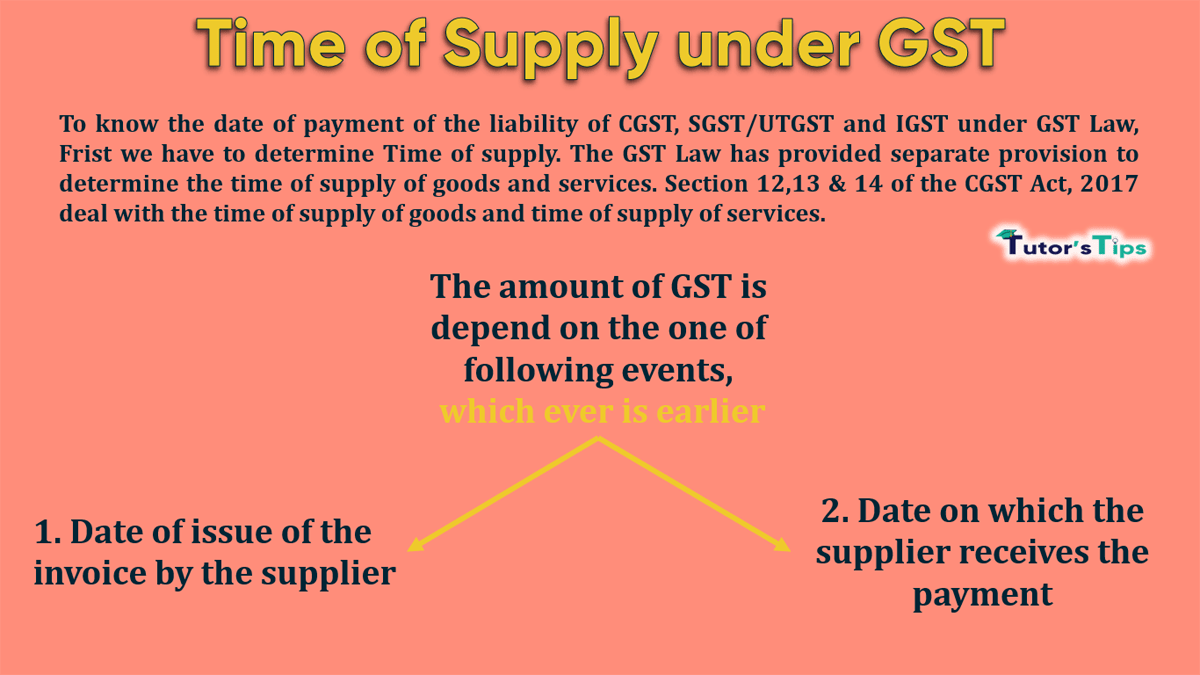

To know the due date of payment of the liability of CGST, SGST/UTGST and IGST under GST Law, Frist we have to determine Time of Supply. The GST Law has provided a separate provision to determine the time of supply of goods and services. Section 12,13 & 14 of the CGST Act, 2017 deal with the time of supply of goods and time of supply of services.

1. How to determine the TOS of goods.

Time of supply of goods determined by the following event: –

Earliest of the following: –

- Date of issue of the invoice by the supplier. (If the invoice is not issued, then the last date on which the supplier is legally bound to issue the invoice with respect to the supply).

OR

- The date on which the supplier receives the payment: –

- The date of the supplier records the payment in his books

OR

- The date on which the payment credited to his bank account.

Example:-

- Date of issue of an invoice is 21/02/2018

- Date of receipt of payment in bank account 15/01/2018

- Date of records the payment in the books of supplier 16/01/2018

Time of Supply will be whichever earliest 15/01/2018

2. How to determine the TOS of Services.

Earliest of the following dates:

The Date of issue of the invoice by the supplier (If the invoice is issued within the legally prescribed period under section 31(2) of the CGST Act) or the date of receipt of payment, whichever is earlier?

OR

The Date of the provision of service (If the invoice is not issued within the legally prescribed period under section 31(2) of the CGST Act) or the date of receipt of payment, whichever is earlier?

OR

The date on which the recipient shows the receipt of service in his books of account, in case the aforesaid two provisions do not apply

3. If the payment made in excess of invoice value?

If payment made against an invoice is excess from invoice value up to Rs. 1,000/- than supplier can pay tax on excess payment when the next invoice will be generated for the same party.

For example: –

If Firm “AB Co.” make payment of Rs. 5,000/- on 09/01/2018 to a firm “BC Co.” and “BC Co” supply goods on 21/01/2018 to “AB Co.” and generate the invoice for Rs. 4,400/-. Then the Time of supply of goods is 09/01/2018. The date of the invoice of the next supply to “AB Co.” is 12/02/2018, then the supplier has the option to treat the time of supply of balance amount either 09/01/18 or 12/02/2018.

4. How to determine the TOS of goods when the tax is to be paid on reverse charge basis?

Whichever is the earliest form following:-

- The date of receipt of goods.

OR

- The date on which the recipient recorded the payment in his books.

OR

The date on which the payment debited from his bank account.

OR

- The date immediately following 30 days from the date of issue of the invoice. or any other legal document in lieu of invoice by the supplier.

If we cannot determine the time of supply in an aforesaid manner, then the time of supply will be the date of record of a transaction in the books of accounts of the recipient.

5. How to determine the TOS of services when the tax is to be paid on reverse charge basis?

Whichever is the earliest form following:-

- The date on which the recipient recorded the payment in his books.

OR

The date on which the payment debited from his bank account.

OR

- The date immediately following 60 days from the date of issue of the invoice or any other legal document in lieu of invoice by the supplier.

If we cannot determine the TOS in an aforesaid manner, then the time of supply will be the date of record of the transaction in the books of accounts of the recipient.

6. TOS of goods or services related to an addition to the value of supply by way of interest, late fees or penalty.

TOS of goods or services related to an addition to the value of supply by way of interest, late fees or penalty will be the date on which supplier receives that additional amount.