Composition scheme under GST(Goods and Services Tax) is a very convenient scheme made for small-scale industries or businesses. In this scheme, the taxpayer has a fixed rate of tax on their aggregate turnover. Any taxpayer can opt this scheme if their aggregate turnover is less than 1.5 Crore or 75 lacs (latest update as per 23RD GST Council meeting held on 10th Nov 2017) in North-Easter states and Himachal Pradesh.

Key feature: –

- Fixed Rate of Tax on Aggregate Turnover

- ITC (Input Tax credit) not eligible

- Only eligible for intra-state supplies

- The bill of supply is not a tax invoice.

- Eligibility made on basis of Aggregate supplies

- Monthly Returns are not required file only Quarterly Returns

- Not need to maintain records.

- Single time Tax payment and easy to calculate.

- Reduce the workload on small business who trying to grow.

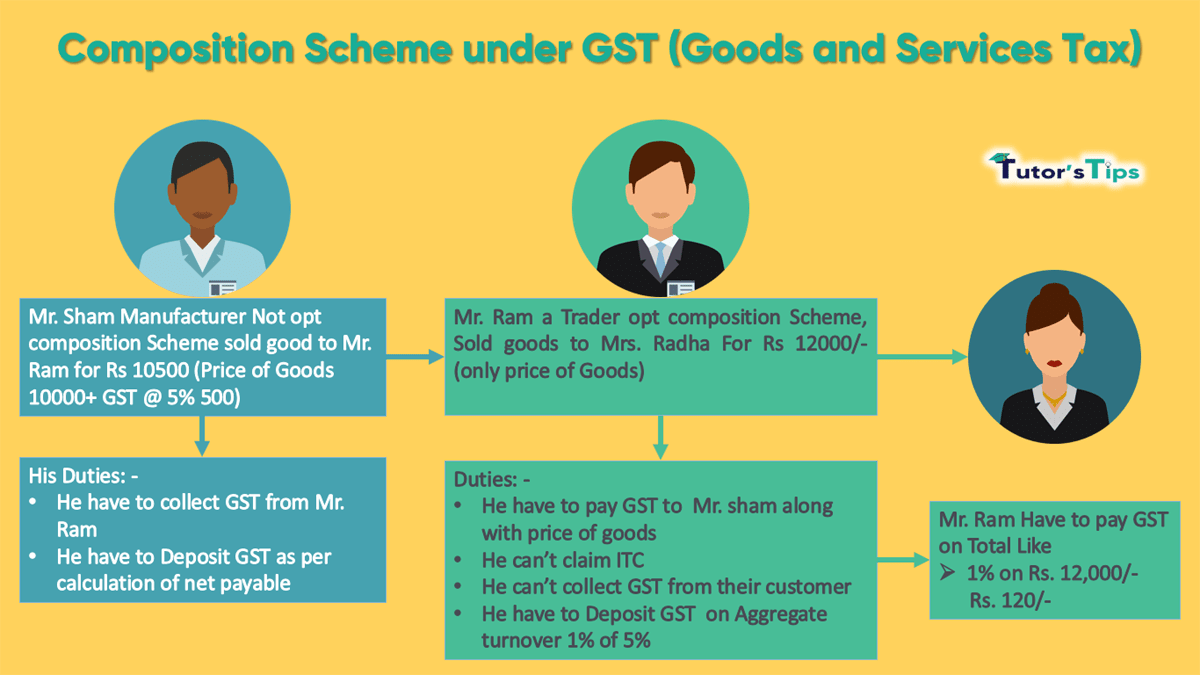

You can understand much better in an example given below: –

")

GST Percentage to be payable as per your type of business shown under: –

")

Who can opt Composition scheme under GST?

Anyone who can fulfil the following conditions: –

- Whose aggregate turnover is less than 1.5 Crore or 75 lacs in North-Easter states and Himachal Pradesh?

- Who is dealing with intra-state supplies only?

- Who is not supplying your goods through E-Commerce marketplace?

- Who is dealing with exempted supplies of goods under GST?

- Who is not the Casual taxable person?

- Who is not a Non-Resident taxable person?

- Who is not dealing with tobacco, pan masala, and ice cream?

- All Services provider expect restaurant related services.

Following are some condition which has to fulfil availing composition scheme under GST

All the above requirements are conditions but some more as following: –

- All business registered with the same PAN are treated as composition supply and total aggregate turnover will be fall within the threshold limit.

- The taxpayer has to mention “Composite taxable person” on their every bill of supply, notice and signboard place at their business premises.