Question No 19 Chapter No 19

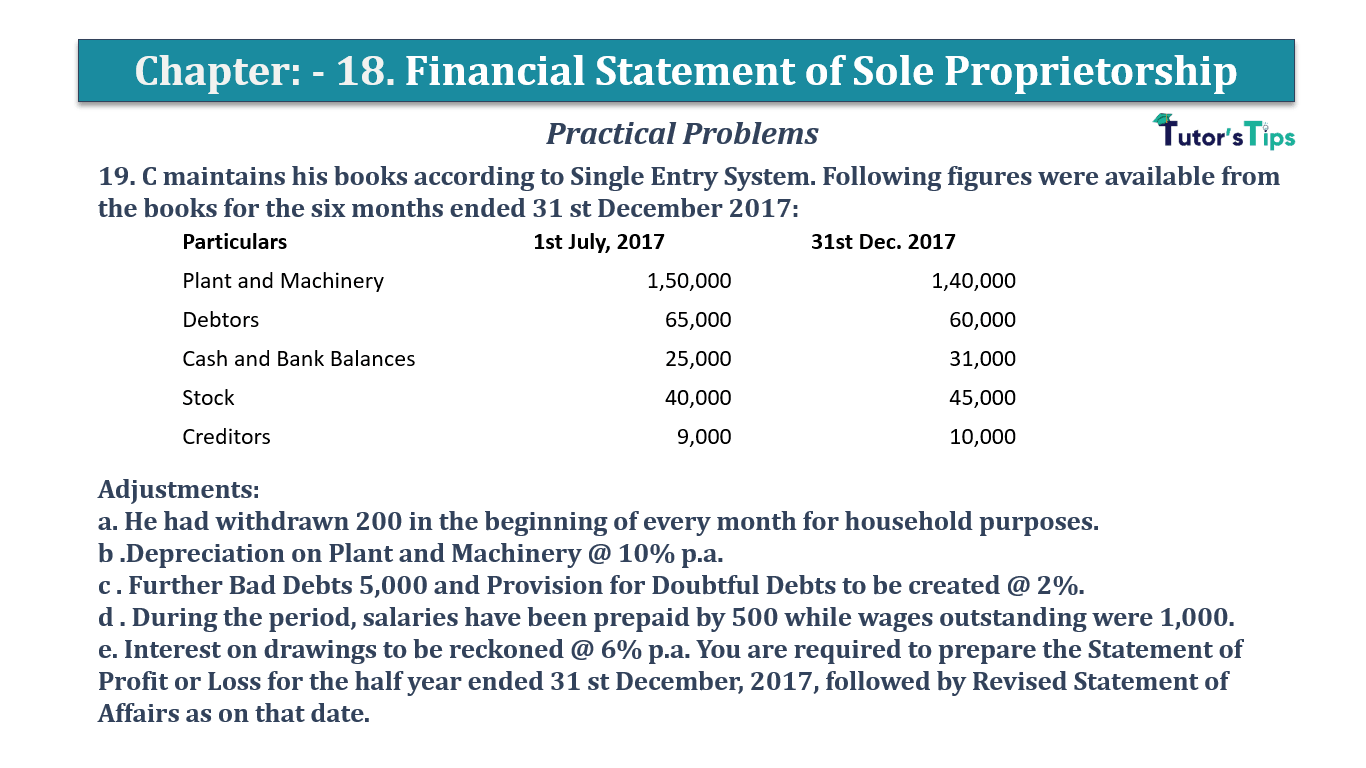

19. C maintains his books according to Single Entry System. Following figures were available from the books for the six months ended 31 st December 2017:

| Particulars | 1st July, 2017 | 31st Dec. 2017 |

| Plant and Machinery | 1,50,000 | 1,40,000 |

| Debtors | 65,000 | 60,000 |

| Cash and Bank Balances | 25,000 | 31,000 |

| Stock | 40,000 | 45,000 |

| Creditors | 9,000 | 10,000 |

Adjustments:

a. He had withdrawn 200 in the beginning of every month for household purposes.

b .Depreciation on Plant and Machinery @ 10% p.a.

c . Further Bad Debts 5,000 and Provision for Doubtful Debts to be created @ 2%.

d . During the period, salaries have been prepaid by 500 while wages outstanding were 1,000.

e. Interest on drawings to be reckoned @ 6% p.a. You are required to prepare the Statement of Profit or Loss for the half year ended 31 st December, 2017, followed by Revised Statement of Affairs as on that date.

The solution of Question No 19 Chapter No 19:-

| Statement of Affairs as on July 01,2017 |

|||||

| Liabilities |

Amount | Assets | Amount | ||

| Creditors | 6,270 | Cash and Bank balances | 25,000 | ||

| Debtors | 65,000 | ||||

| Stock | 40,000 | ||||

| Plant and Machinery | 1,50,000 | ||||

| Capital | 2,71,000 | ||||

| 2,80,000 | 2,80,000 | ||||

| Statement of Affairs as on December 31,2017 |

|||||

| Liabilities |

Amount | Assets | Amount | ||

| Creditors | 10,000 | Cash and Bank balances | 31,000 | ||

| Outstanding Wages | 1,000 | Debtors | 60,000 | ||

| Stock | 45,000 | ||||

| Plant and Machinery | 1,40,000 | ||||

| Prepaid Salary | 500 | ||||

| Capital | 2,65,500 | ||||

| 2,76,500 | 2,76,500 | ||||

| Statement of Profit or Loss for the half year ended December 31,2017 |

||

| Particular |

Amount | |

| Capital at the end of the year | 2,65,500 | |

| Add: Drawings made during the year | 1,200 | |

| Adjusted capital at the end of the year | 2,66,700 | |

| Less: Capital in the beginning of the year | 2,71,000 | |

| Gross Loss Profit before Adjustment | 4,300 | |

| Less: Interest on Drawings | 21 | |

| Add: Depreciation on Plant and Machinery | 7,000 | |

| Bad Debt | 5,000 | |

| Provision for Doubtful Debts | 1,100 | |

| Net Loss Profit After Adjustment | 17,379 | |

| Statement of Affairs After adjustments as on December 31, 2017 |

|||||

| Liabilities |

Amount | Assets | Amount | ||

| Creditors | 10,000 | Cash and Bank balances | 31,000 | ||

| Outstanding Wages | 1,000 | Stock | 45,000 | ||

| Capital | 2,71,000 | Debtors | 60,000 | ||

| Less: Net Loss | 17,379 | Less: Bad Debts | 5,000 | ||

| Less: Drawings | 1,200 | Less: Provision for D.D. | 1,100 | 53,900 | |

| Less: Interest on Drawings | 21 | 2,52,400 | Plant and Machinery | 1,40,000 | |

| Less: Depreciation | 7,000 | 1,33,000 | |||

| Prepaid Salary | 500 | ||||

| 2,63,400 | 2,63,400 | ||||

Working Notes

To calculate the Amount of Deprecation charged on Plant and Machinery

Depreciation = Value of Asset X Rate of Depreciation X Period

Value of Asset = 1,40,000

Rate of Depreciation = 10%

Period = from 01/07/2017 to 31/12/2017 i.e.6months

(from the date of purchase/Beginning balance to end of the financial year)

=1,40,000 X10/100 X 6/12

Depreciation = 7,000

The calculation of Amount of Provision for Doubtful Debts

Provision for Doubtful Debts= Sundry Debtors – Further Bad Debts X Rate of Provision

Sundry Debtors = 60,000

Rate of Provision = 2%

60,000 -5,000 X2/100

Provision For Doubtful Debts= 1,100

Calculation of Amount of Interest on Drawings:

| Date |

Amount | Months | Product |

| Jul. 01, 2017 | 200 | 6 | 1,200 |

| Aug. 01, 2017 | 200 | 5 | 1,000 |

| Sep. 01, 0217 | 200 | 4 | 800 |

| Oct. 01, 0217 | 200 | 3 | 600 |

| Nov. 01, 2017 | 200 | 2 | 400 |

| Dec. 01, 2017 | 200 | 1 | 200 |

| Total | 4,200 | ||

Interest on Drawings

4,200 X6/100 X 1/12

Interest on Drawing = 21

Final Accounts: Meaning, Definition and Explanation

Profit and Loss Account: Meaning, Format & Examples

Balance Sheet: Meaning, Format & Examples

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of previous Chapters: –

-

- Chapter No. 1 – Introduction to Accounting

- Chapter No. 2 – Basic Accounting Terms

- Chapter No. 3 – Theory Base of Accounting, Accounting Standards and International Financial Reporting Standards(IFRS)

- Chapter No. 4 – Bases of Accounting

- Chapter No. 5 – Accounting Equation

- Chapter No. 6 – Accounting Procedures – Rules of Debit and Credit

- Goods and Services Tax(GST)

- Chapter No. 7 – Origin of Transactions – Source Documents and Preparation of Vouchers

- Chapter No. 8 – Journal

- Chapter No. 9 – Ledger

- Chapter No. 10 – Special Purpose Books I – Cash Book

- Chapter No. 11 – Special Purpose Books II – Other Books

- Chapter No. 12 – Bank Reconciliation Statement

- Chapter No. 13 – Trial Balance

- Chapter No. 14 – Depreciation

- Chapter No. 15 – Provisions and Reserves

- Chapter No. 16 – Accounting for Bills of Exchange

- Chapter No. 17 – Rectification of Errors

- Chapter No. 18 – Financial Statements of Sole Proprietorship

- Chapter No. 19 – Adjustments in preparation of Financial Statements

- Chapter No. 20 – Accounts from incomplete Records – Single Entry System

- Chapter No. 21 – Computers in Accounting

- Chapter No. 22 – Accounting Software – Tally

- Chapter No. 5 – Accounting Equation

- Chapter No. 6 – Accounting Procedures – Rules of Debit and Credit

- Goods and Services Tax(GST)

- Chapter No. 8 – Journal

- Chapter No. 9 – Ledger

- Chapter No. 10 – Special Purpose Books I – Cash Book

Check out T.S. Grewal +1 Book 2019 @ Official Website of Sultan Chand Publication

T.S. Grewal’s Double Entry Book Keeping