Final Accounts are prepared to know the financial position of the business at the end of a financial period. It is also known as the Financial statement of the business.

What is Final Accounts

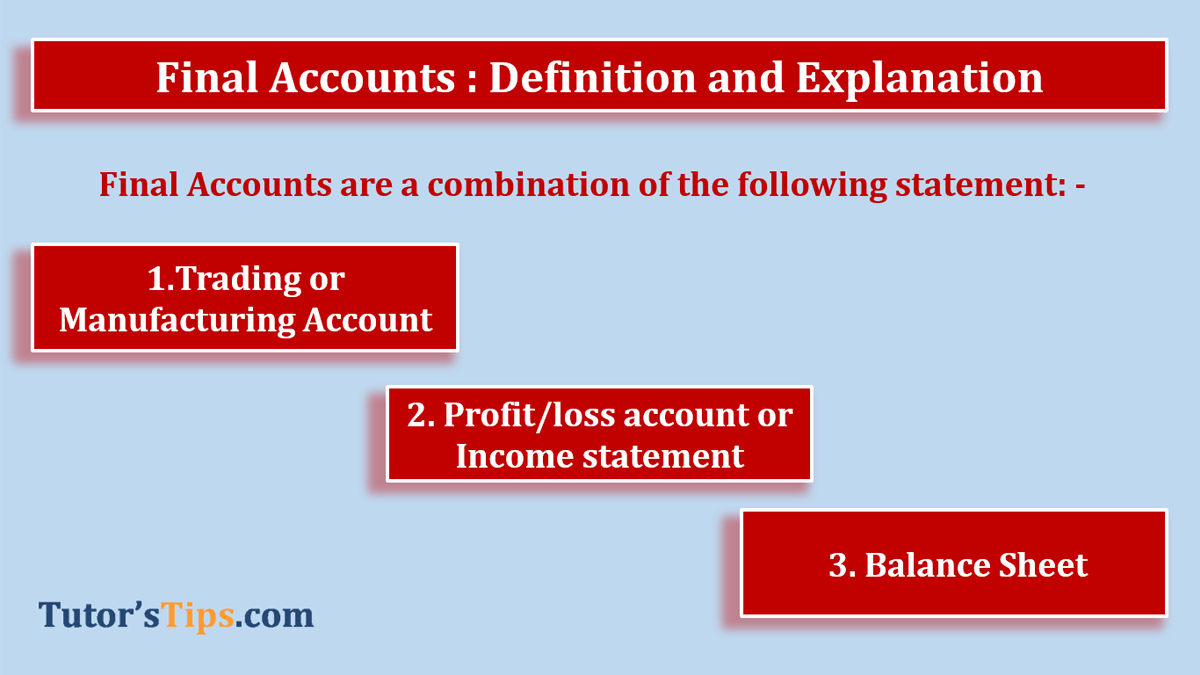

Final Accounts gives an idea about the profitability and financial position of a business to its management, owners, and other interested parties. It is a combination of the following statement: –

- Trading Account

- Profit and loss account

- Balance Sheet

Every businessman started a business to earn some income from it. Profit is the net income that the owner gets from the business. To calculate profit or loss, An accountant has made the final accounts for the business for a particular accounting period(i.e. One year starts from 1st April and end 31st March).

On the basis of the Trial balance, An accountant prepared the final accounts or financial statement for the particular period of time for reporting the management of the business. The final accounts are prepared to throw light on the financial results of the operation of the business during the particular accounting period of time and the financial position of the business at that period of time.

The feature of Final Accounts: –

- To know the Profitability of the business: – Final accounts help to business to get know the profitability of the business in a particular accounting year.

- Financial Strength: – Final account provide information about the financial strength of the business. it means, help in deciding whether the business can purchase new assets with its own fund or not.

- Forecasting and Budgeting: – Final Accounts are the basis of the forecasting and the budgeting for the top management. On the basis of last year’s final accounts, management decides the business new goal for the current year and preparing the budget for expenses.

- Communication:- We need final accounts or financial Statements to communicate our financial position with different parties (i.e. Investors, Lenders of Money, Supplier and Trade Creditors and Government etc.)

- Growth Rate of business: – With the help of the final account can calculate the growth rate or our business by comparing the financial statement of the current year with last year.

Statement Involve in the Final accounts: –

1. Trading Account:-

A trading or Manufacturing account is prepared to find out the gross profit of the business for the particular accounting period. It is calculated by comparing the net sale with the cost of goods sold(COGS).

Gross Profit/Loss = Net Sale – COGS

Net Sale = Total Sale (Cash sale + Credit Sale) – Sale Returned/Returned Inward

Cost of Goods Sold = Opening Stock + Net Purchase + Direct Expenses – Closing Stock.

- Opening Stock = Stock we have in hand at the start of the accounting year.

- Net Purchase = Total Purchase (Cash Purchase + Credit Purchase ) – Purchase Returned/Returned Outward

- Direct Expenses = All expenses which are directly related to purchasing of goods and converting them into saleable condition.

- Closing Stock = Stock we have in hand at the end of the accounting year.

The format of Trading Account:-

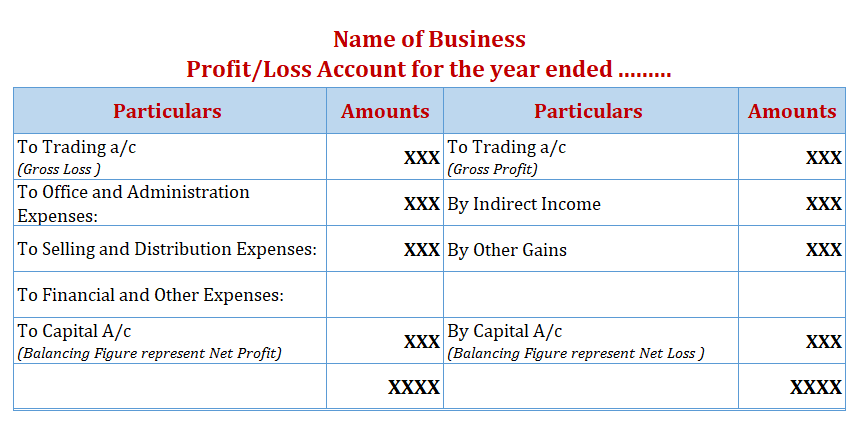

2. Profit and loss account: –

A profit and loss account or Income statement is prepared to find out the Net Profit/loss of the business for the particular accounting period. It is calculated by comparing the Gross Proft/Loss with indirect income and expenses.

Net Profit/Loss = Gross Profit/Loss + Indirect Income – Indirect Expenses

- Indirect Income = Other incomes which are earned from other than the main operation of the business.

- Indirect Expense = All business expenses other than direct expenses.

The format of Profit and Loss Account:-

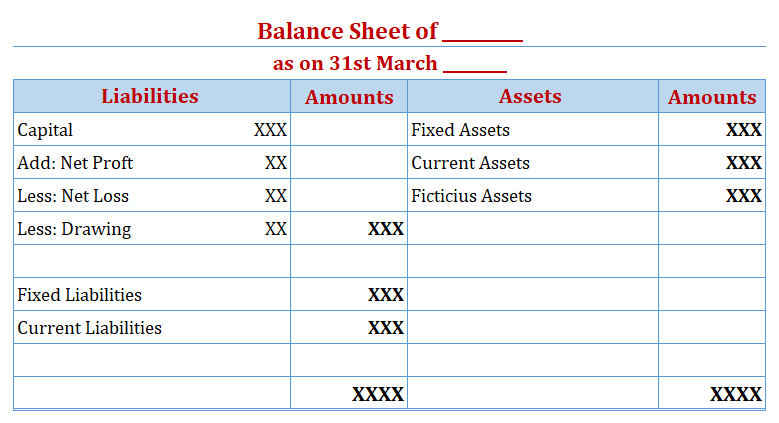

3. Balance Sheet: –

The Balance sheet is the statement showing the position of the assets and liabilities of the business in a particular accounting period. The value of assets shows which we can realize from the market and The value of Liabilities shows which we have to pay in future. it is the basis of the following account equation.

Assets = Capital + Liabilities

The format of the Balance Sheet: –

Users of final account: –

- Management:- Management use final accounts or financial statement for preparing a plan and budget for the next year.

- Investors: – Investors are the persons who invest their money into the business. Before making an investment they want to know the earning capacity of an enterprise. So, The Final accounts provide all this information to them.

- Lenders of Money: – Lenders of Money are the persons who lent their money to an enterprise. They want to know the repaying capacity of the business. So, The Final accounts provide all this information to them.

- Taxation Authorities: – Taxation Authorities collect taxes from the business on net profit for the year. To Know the net profit we need the Final accounts or Financial Statements for the year.

- Government: – On the basis of the financial statement, Government authorities determine the progress of various industries and the need for financial help. Various Taxation is levied by the government after analyzing the financial statements.

- Others Parties: – These are shown as follow: –

- Bankers

- Employees

- Creditors

- Stock Exchange authorities

- researchers

- economists

- customers

- Etc.

Thanks for reading the topic of Final Accounts, please comment your feedback whatever you want.

If you have any questions please ask us by commenting.