Question 65 Chapter 5 of +2-A

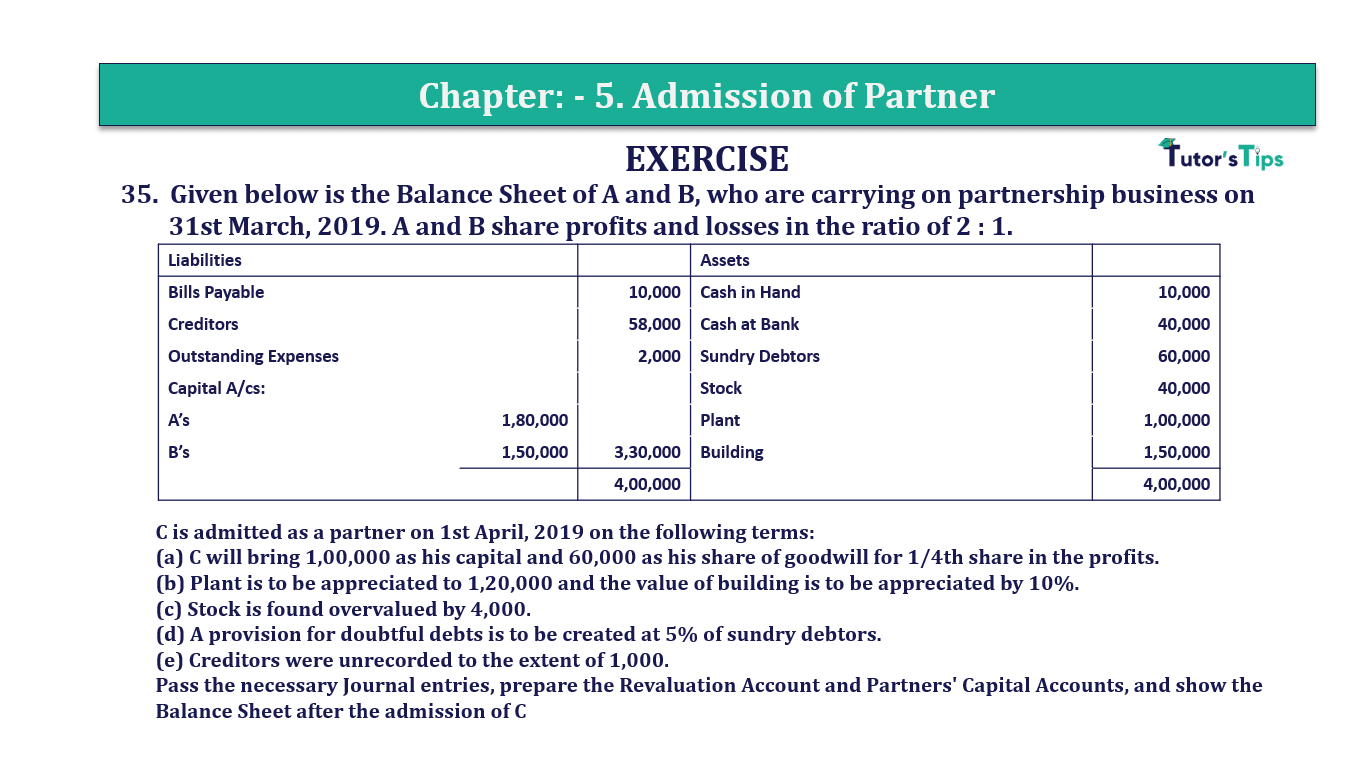

65. Given below is the Balance Sheet of A and B, who are carrying on partnership business on 31st March, 2019. A and B share profits and losses in the ratio of 2 : 1.

| Liabilities | Assets | |||

| Bills Payable | 10,000 | Cash in Hand | 10,000 | |

| Creditors | 58,000 | Cash at Bank | 40,000 | |

| Outstanding Expenses | 2,000 | Sundry Debtors | 60,000 | |

| Capital A/cs: | Stock | 40,000 | ||

| A’s | 1,80,000 | Plant | 1,00,000 | |

| B’s | 1,50,000 | 3,30,000 | Building | 1,50,000 |

| 4,00,000 | 4,00,000 |

C is admitted as a partner on 1st April, 2019 on the following terms:

(a) C will bring 1,00,000 as his capital and 60,000 as his share of goodwill for 1/4th share in the profits.

(b) Plant is to be appreciated to 1,20,000 and the value of building is to be appreciated by 10%.

(c) Stock is found overvalued by 4,000.

(d) A provision for doubtful debts is to be created at 5% of sundry debtors.

(e) Creditors were unrecorded to the extent of 1,000.

Pass the necessary Journal entries, prepare the Revaluation Account and Partners’ Capital Accounts, and show the Balance Sheet after the admission of C

The solution of Question 65 Chapter 5 of +2-A: –

| Date | Particulars |

L.F. | Debit | Credit | |

| Revaluation A/c | Dr | 1,60,000 | |||

| To C’s Capital A/c | 1,00,000 | ||||

| To Premium for Goodwill A/c | 60,000 | ||||

| (Being C brought his share of goodwill and capital in cash) | |||||

| Premium for Goodwill A/c | Dr | 60,000 | |||

| To A’s Capital A/c | 40,000 | ||||

| To B’s Capital A/c | 20,000 | ||||

| (Being Premium for goodwill distributed between X, Y and Z in sacrificing ratio i.e. 3:1) | |||||

| Plant A/c | Dr | 20,000 | |||

| Building A/c | Dr | 15,000 | |||

| To Revaluation A/c | 35,000 | ||||

| (Increase in value of plant and Building of transferred to Revaluation Accounts) | |||||

| Revaluation A/c | Dr | 8,000 | |||

| To Stock A/c | 4,000 | ||||

| To Provision for Doubtful Debts A/c | 3,000 | ||||

| To Creditors A/c (Unrecorded) | 1,000 | ||||

| (Being Decrease in stock, creation of Provision for Doubtful Debt and transferred to Revaluation Account. Unrecorded Creditors recorded in the books) | |||||

| Revaluation A/c | Dr | 27,000 | |||

| To A’s Capital A/c | 18,000 | ||||

| To B’s Capital A/c | 9,000 | ||||

| (Being Profit on revaluation account distributed between A and B in their old ratio) | |||||

| Revaluation A/c |

|||||

| Particular |

Amount | Particular | Amount | ||

| Stock | 4,000 | Plant | 20,000 | ||

| Provision for Doubtful Debts | 3,000 | Building | 15,000 | ||

| Creditors (Unrecorded) | 1,000 | ||||

| Profit transferred to | |||||

| A’s Capital | 18,000 | ||||

| B’s Capital | 9,000 | 27,000 | |||

| 35,000 | 35,000 | ||||

| Partners’ Capital Accounts the year ended 31st March, 2019 |

|||||||

| Particulars | A | B | C | Particulars | A | B | C |

| By Balance B/d | 1,80,000 | 1,50,000 | – | ||||

| By Cash A/c | – | – | 1,00,000 | ||||

| By Premium for Goodwill A/c | 40,000 | 20,000 | – | ||||

| By Revaluation A/c | 18,000 | 9,000 | – | ||||

| To Balance c/d | 2,38,000 |

1,79,000 | 1,00,000 | ||||

| 2,38,000 | 1,79,000 | 1,00,000 | 2,38,000 | 1,79,000 | 1,00,000 | ||

| Balance Sheet |

|||||

| Liabilities |

Amount | Assets | Amount | ||

| Bills Payable | 32,950 | Cash in Hand | 10,000 | ||

| Creditors | 59,000 | Cash at Bank | (40,000+ 1,60,000) | 2,00,000 | |

| Capital: | Stock | (40,000 – 4,000) | 36,000 | ||

| A’s | 2,38,000 | Sundry Debtors | 60,000 | ||

| B’s | 1,79,000 | Less: Provision for D. Debts | 3,000 | 57,000 | |

| C’s | 1,00,000 | 5,17,000 | Plant | 1,20,000 | |

| Outstanding Expenses | 2,000 | Building | 1,65,000 | ||

| 5,88,000 | 5,88,000 | ||||

Working Note:-

| Old Ratio of A and B | = | 3 : 2 |

| C is admitted for 1/8th share of profit |

Let the total share of the business = 1

Remaining share of A and B after C’s Admission = Total Share – C’s Share

| Remaining share | = | 1 | – | 1 |

| 8 |

| = | 8 – 1 | |

| 8 |

| = | 7 | ||

| 8 |

To Calculate to New Ratio distribute the remaining share in the old ratio of old partners’

New Ratio = Combined share of A and B X Old Ratio

| A’s New Ratio | = | 7 | X | 3 |

| 8 | 5 |

| = | 21 | ||

| 40 |

| B’s New Ratio | = | 7 | X | 2 |

| 8 | 5 |

| = | 14 | ||

| 40 |

| C’s New Ratio | = | 1 | X | 5 |

| 8 | 5 |

| = | 5 | ||

| 40 |

New Profit sharing Ratio between A ,B and C = 21 : 14 : 5

| Average Profit | = | Total Profit for past given years |

| Number of years |

| = | 21,000 + 24,000 + 25,560 | |

| 3 |

| = | 70,560 | |

| 3 | ||

| = | 23,520 |

| Number of years’ purchase | = | 2 |

| Goodwill | = | Average Profit X Number of years’ purchase |

| Goodwill | = | 23,520 X 2 |

| Goodwill | = | 47,040 |

| C’s Share of Goodwill | = | Firm’s Goodwill X Share of HinaS |

| = | 47,040 | X | 1 | |

| 8 | ||||

| = | 5,880 |

Sacrificing Ratio of A and B = 3 : 2

| A will get Share of Goodwill | = | C’s Goodwill X Sacrifice share of A |

| = | 5,880 | X | 3 | |

| 5 | ||||

| = | 3,528 |

| B will get Share of Goodwill | = | C’s Goodwill X Sacrifice share of B |

| = | 5,880 | X | 2 | |

| 5 | ||||

| = | 2,352 |

Distribution of Profit from Revaluation Account (in old ratio)

| A will get | = | 750 | X | 2 |

| 3 | ||||

| = | 500 |

| B will get | = | 750 | X | 1 |

| 3 | ||||

| = | 250 |

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication