Question No 11 Chapter No 10

Enter the following transaction in the cash book of Chandrika of Chandigarh:

| 2018 | Rs | |

| Jan.1 | Chandrika commences business with Cash | 1,00,000 |

| Jan.3 | She opened a Bank current Account with her Saving Account cheque | 19,00,000 |

| Jan.4 | She receives a cheque from Kirti & Co. on account | 60,000 |

| Jan.7 | She pays into Bank Kirti & Co.’s cheque | 60,000 |

| Jan.10 | She advanced Ratan & Co. by cheque | 35,000 |

| Jan.12 | Tripathi & Co. pays into Bank Account | 47,500 |

| Jan.15 | She receives a cheque from Warsi and allows him to discount Rs 3,500 | 45,000 |

| Jan.20 | She receives cash Rs 7,500 and cheque Rs 10,000 from Kalyan against Credit Balance | |

| Jan.25 | She pays into Bank, including cheque received on 15th and 20th January | 1,00,000 |

| Jan.27 | She pays by Cheque for purchases of Rs 27,500 plus CGST and SGST @6% each | |

| Jan.28 | Cheque received from Warsi was dishonoured | |

| Jan.30 | She pays sundry expenses in cash | 50 |

| Jan.30 | She pays John & Co. in cash and is allowed discount Rs3,500 | 37,500 |

| Jan.31 | She pays office rent Rs 20,000 plus CGST and SGST @6% each by cheque | |

| Jan.31 | She draws a cheque for office use | 40,000 |

| Jan.31 | She pays staff salaries by cheque | 30,000 |

| Jan.31 | She pays Cash for stationery Rs2,500 plus CGST and SGST @6% each | |

| Jan.31 | She purchases goods for cash Rs12,500 plus CGST and SGST @6% each | |

| Jan.31 | She pays Jagpal by cheque for commission Rs30,000 plus CGST and SGST@6% each | |

| Jan.31 | She receives a cheque for a commission of Rs 50,000 plus CGST and SGST @6% each from Raghubir & Co. and pays the same into Bank | |

| Jan.31 | Cash sale Rs 45,000 Plus CGST and SGST @6% each |

The solution of Question No 11 Chapter No 10: –

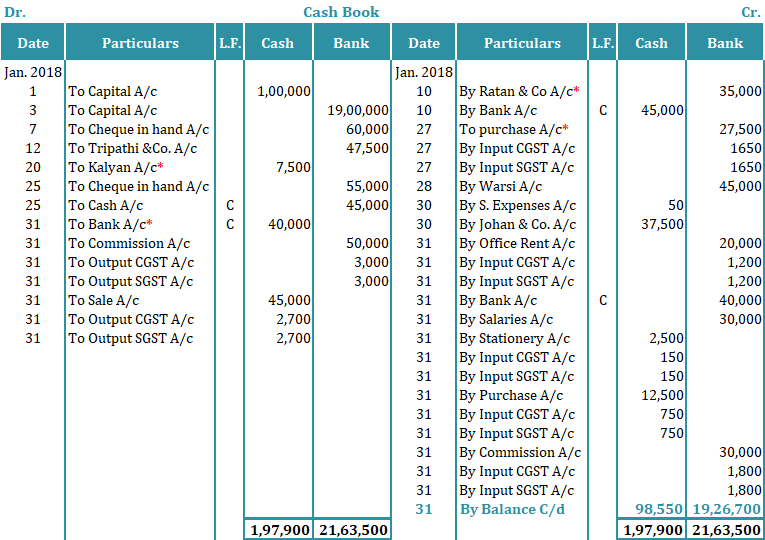

Note: - we have shown the both side speratly because it is very wide and defficult to understand. Please check image to understand the actual or real format of cash book.

In the Books of Chandrika, Chandigarh

| Dr. | Cash Book | |||

| Date | Particulars |

L.F. | Cash | Bank |

| Jan. 2018 | ||||

| 1 | To Capital A/c | 1,00,000 | ||

| 3 | To Capital A/c | 19,00,000 | ||

| 7 | To Cheque in hand A/c | 60,000 | ||

| 12 | To Tripathi &Co. A/c | 47,500 | ||

| 20 | To Kalyan A/c* | 7,500 | ||

| 25 | To Cheque in hand A/c | 55,000 | ||

| 25 | To Cash A/c | C | 45,000 | |

| 31 | To Bank A/c* | C | 40,000 | |

| 31 | To Commission A/c | 50,000 | ||

| 31 | To Output CGST A/c | 3,000 | ||

| 31 | To Output SGST A/c | 3,000 | ||

| 31 | To Sale A/c | 45,000 | ||

| 31 | To Output CGST A/c | 2,700 | ||

| 31 | To Output SGST A/c | 2,700 | ||

| 1,97,900 | 21,63,500 | |||

| Cash Book | Cr. | |||

| Date | Particulars |

L.F. | Cash | Bank |

| Jan. 2018 | ||||

| 10 | By Ratan & Co A/c* | 35,000 | ||

| 10 | By Bank A/c | C | 45,000 | |

| 27 | To purchase A/c* | 27,500 | ||

| 27 | By Input CGST A/c | 1650 | ||

| 27 | By Input SGST A/c | 1650 | ||

| 28 | By Warsi A/c | 45,000 | ||

| 30 | By S. Expenses A/c | 50 | ||

| 30 | By Johan & Co. A/c | 37,500 | ||

| 31 | By Office Rent A/c | 20,000 | ||

| 31 | By Input CGST A/c | 1,200 | ||

| 31 | By Input SGST A/c | 1,200 | ||

| 31 | By Bank A/c | C | 40,000 | |

| 31 | By Salaries A/c | 30,000 | ||

| 31 | By Stationery A/c | 2,500 | ||

| 31 | By Input CGST A/c | 150 | ||

| 31 | By Input SGST A/c | 150 | ||

| 31 | By Purchase A/c | 12,500 | ||

| 31 | By Input CGST A/c | 750 | ||

| 31 | By Input SGST A/c | 750 | ||

| 31 | By Commission A/c | 30,000 | ||

| 31 | By Input CGST A/c | 1,800 | ||

| 31 | By Input SGST A/c | 1,800 | ||

| 31 | By Balance C/d | 98,550 | 19,26,700 | |

| 1,97,900 | 21,63,500 | |||

All transactions which are highlighted with (*) are explained as following as follows: –

*Oct. 7 Bought goods for Rs 15,000 plus IGST@12% against Cheque

The calculation of Amount of CGST and SGST @ 6% each

15,000 * 12% = 1,800/-

*Oct. 8 Bought goods for 5,000 plus CGST and SGST@6% each

The calculation of Amount of CGST and SGST @ 6% each

5,000 * 6% = 300/- each

*Oct. 18 Ramesh who owed Rs 5,000 became Bankrupt and Paid us 50 paise in a rupee

The calculation of the Amount of Bad Debts

5,000 X .50

2,500/-

*Oct. 27 Sold goods for Rs 11,000 Plus CGST and SGST @6% against Cash

The calculation of Amount of CGST and SGST @ 6% each

11,000 * 6% = 660/- each

*Oct. 28 Received a cheque for goods sold for Rs 9,000 plus CGST and SGST @6% each

The calculation of Amount of CGST and SGST @ 6% each

9,000 * 6% = 540/- each

To understand more about cash book please check out following links: –

Cash Book | Types of Cash Book | Subsidiary Books

Single Column Cash Book | Explained with Example

Double Column Cash Book | Explained with Example

Triple Column Cash Book | Explained with Example

Petty Cash Book | Example | Subsidiary Books

Thanks Please share with your friends

Comment if you have any question.

Also, Check out previous Chapters: –

- Chapter No. 5 – Accounting Equation

- Chapter No. 6 – Accounting Procedures – Rules of Debit and Credit

- Goods and Services Tax(GST)

- Chapter No. 8 – Journal

- Chapter No. 9 – Ledger

Check out T.S. Grewal +1 Book 2019 @ Oficial Website of Sultan Chand Publication

T.S. Grewal’s Double Entry Book Keeping