Petty Cash book is the fourth type of cash book. In this article, we will discuss the meaning of Petty Cash Book, methods of payment, and types of petty cash books.

What is Petty Cash Book?

First of all, you have to know the meaning of petty cash. Petty cash means the small amount of cash in the hand of the petty cashier for the payment of routine petty(small) expenses. The petty cashier prepares the statement of receipt and payment of petty cash, which is known as the petty cash book.

In other words, When the head cashier pays some amount of cash to a petty cashier for petty expenses then the cashier prepared a statement of petty expenses which are paid by him for a fixed period of time. This statement is known as petty cash book. It has a standardized format and can be prepared in the two types of presentation which we will discuss in this article. We will also discuss the way to pay cash to the petty cashier by the head cashier.

Here are some examples of Petty Expenses like: Postage, stationery, Photostate,staff wellfare,Newpapers, Carriage, etc.

Methods to pay cash to the petty cashier by the Head Cashier:

The different methods to pay the cash to the petty cashier by the head cashier are shown as following: –

- When Needed

- Fixed amount for a fixed period

- Imprest account

1. When Needed:

In this system, the head cashier pays cash to the Petty cashier when he needs it means he had spent all the cash received before.

2. Fixed amount for a fixed period:

In this system, the Head cashier pays a fixed amount to the petty cashier for a fixed time (it may be for a day, a week, or a month)

3. Imprest account

This system is generally followed by most of the business concerns. Under this system, the total petty expenses for a particular period are estimated and that amount is advanced by the Head Cashier to the Petty Cashier. This amount is called Imprest Cash.

Type of Petty Cashbook:

- Simple

- Columnar or Analytical

1. Simple Petty Cash Book:

It is almost similar to a simple cash book. For small-scale businesses, a simple petty cash book is sufficient. The format of this is shown below:

Detail of Columns in Simple Petty Cash Book: –

The detail of all columns are given as follows: –

1. Debit / Receipts: –

The amount received from the head cashier will be entered in this column.

2. C. B. Folio: –

C. B. folio means cash book folio. The cash payment to the petty cashier record in the main cash book and the page no. or entry number of the main cash book written in this column.

3. Date: –

The date of cash receipt and payment will be entered in this column.

4. Particulars: –

Details of the transaction recorded in this column.

5. V. No.:-

V. No. means voucher number. In an accounting system, we have to provide voucher numbers to each and every single transaction for rechecking or maintaining the record in a systematic way. These numbers will be entered in this column.

6. L. F.: –

L.F. means Ledger folio. The petty cash book is the original entry book so we will post these all transactions in the ledger. So, page no. of the ledger book on which this transaction is recorded will be entered in this column.

7. Credit / Payments.

The payment amount of the transaction of all petty expenses met by the petty cashier will be recorded in this column.

Example of Simple Petty Cash Book: –

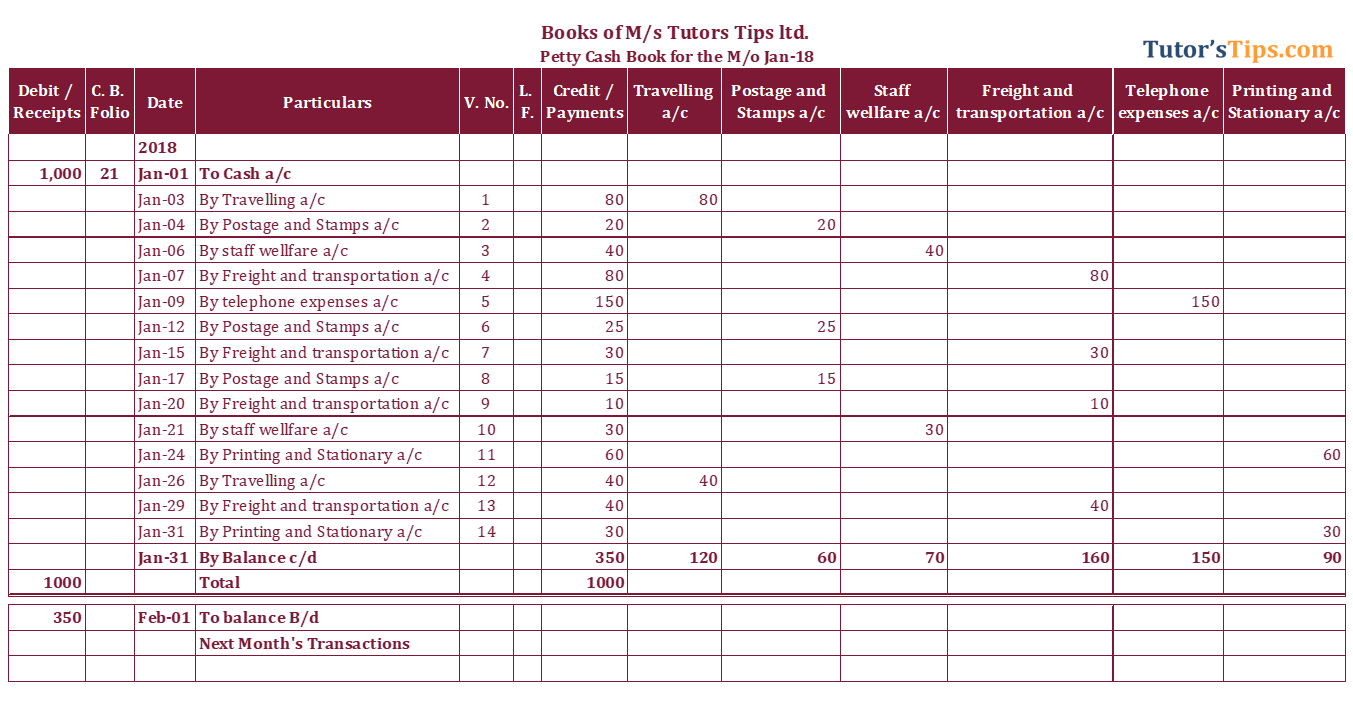

Prepare a petty cash book in the books of M/s Tutors Tips ltd. on the basis of the following transactions.

| Date | V. No. | Particulars | Amount |

| 2018 | |||

| Jan 1 | 1(Receipt No.) | Cash received from head Cashier with C.B entry No. 21 | 1,000 |

| Jan 3 | 1 | Traveling Expenses paid for the tour of Mr. Aman | 80 |

| Jan 4 | 2 | Revenue stamps purchased | 20 |

| Jan 6 | 3 | Staff tea and snacks expenses paid | 40 |

| Jan 7 | 4 | Freight paid on the purchase of goods | 80 |

| Jan 9 | 5 | Telephone Expenses Paid | 150 |

| Jan 12 | 6 | Revenue stamps purchased | 25 |

| Jan 15 | 7 | Freight paid | 30 |

| Jan 17 | 8 | Telegram charges paid | 15 |

| Jan 20 | 9 | Paid for carriage | 10 |

| Jan 21 | 10 | Refreshments Exp of staff | 30 |

| Jan 24 | 11 | Stationary expenses | 60 |

| Jan 26 | 12 | Paid traveling expenses | 40 |

| Jan 29 | 13 | Freight paid on the purchase of goods | 40 |

| Jan 31 | 14 | Stationary expenses | 30 |

Solutions:-

2. Columnar or Analytical Petty Cash Book:

For small-scale businesses, a simple petty cash book is sufficient but on a medium or large scale business number of petty expenses increases hence it is desirable to have a separate record for each type of petty expense. But this one will be able to know which items of petty expenses need to be controlled. The format of it is shown below:

Details of Column in Columnar Petty Cash Book: –

The following all column are the same with simple Petty Cash Book

- Debit / Receipts: –

- C. B. Folio:

- Date: –

- Particulars: –

- V. No.:-

- L. F.: –

- Credit / Payments.

8. Name of Expenses: –

In these columns, we have to make a separate column for each separate expense.

Example Columnar or Analytical Petty CashBook: –

We have taken the same example as above and solved it in columnar format.

Solutions:-