Question No 4 Chapter No 10

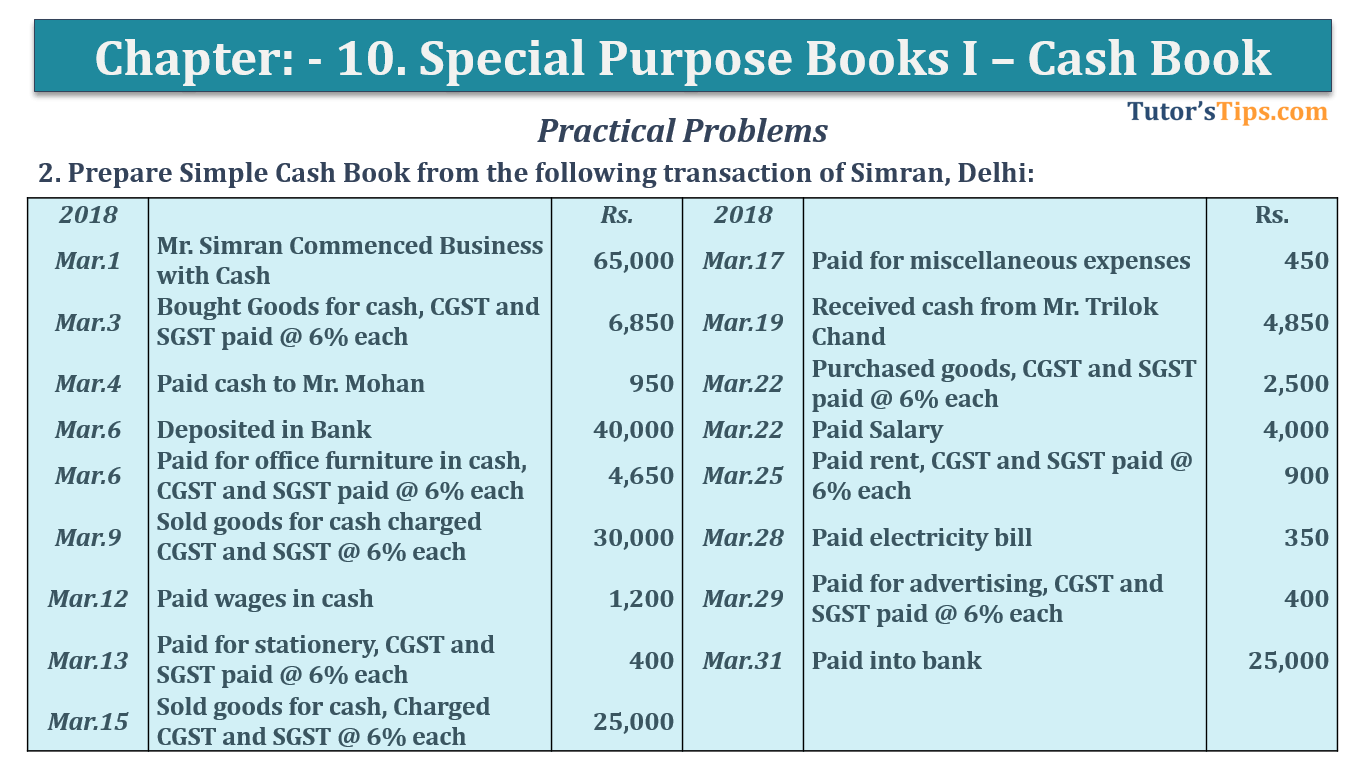

Prepare Simple Cash Book from the following transaction of Simran, Delhi:

| 2018 | Rs. | 2018 | Rs. | ||

| Mar.1 | Mr Simran Commenced Business with Cash | 65,000 | Mar.17 | Paid for miscellaneous expenses | 450 |

| Mar.3 | Bought goods for cash, CGST and SGST paid @ 6% each | 6,850 | Mar.19 | Received cash from Mr Trilok Chand | 4,850 |

| Mar.4 | Paid cash to Mr Mohan | 950 | Mar.22 | Purchased goods, CGST and SGST paid @ 6% each | 2,500 |

| Mar.6 | Deposited in Bank | 40,000 | Mar.22 | Paid Salary | 4,000 |

| Mar.6 | Paid for office furniture in cash, CGST and SGST paid @ 6% each | 4,650 | Mar.25 | Paid rent, CGST and SGST paid @ 6% each | 900 |

| Mar.9 | Sold goods for cash charged CGST and SGST @ 6% each | 30,000 | Mar.28 | Paid electricity bill | 350 |

| Mar.12 | Paid wages in cash | 1,200 | Mar.29 | Paid for advertising, CGST and SGST paid @ 6% each | 400 |

| Mar.13 | Paid for stationery, CGST and SGST paid @ 6% each | 400 | Mar.31 | Paid into bank | 25,000 |

| Mar.15 | Sold goods for cash, Charged CGST and SGST @ 6% each | 25,000 | |||

| Mar.24 | Payment to a carpenter for repairs to private property | 350 | |||

| Mar.26 | Paid for medical expenses of Smt. Gopal | 1,800 | |||

| Mar.30 | Paid for shop rent Rs 2,000 along with CGST and SGST @ 6% each |

The solution of Question No 4 Chapter No 10: –

In the Books of Simran, Delhi

| Dr. | Cash Book | Cr. | |||||

| Date | Particulars |

L.F. | Amount | Date | Particulars |

L.F. | Amount |

| 2018 | 2018 | ||||||

| Mar. 1 | To Capital A/c | 65,000 | Mar. 3 | By Purchase A/c* | 6,850 | ||

| Mar. 9 | To Sale A/c* | 30,000 | Mar. 3 | By Input CGST A/c | 411 | ||

| Mar. 9 | To Output CGST A/c | 1,800 | Mar. 3 | By Input SGST A/c | 411 | ||

| Mar. 9 | To Output SGST A/c | 1,800 | Mar. 4 | By Mr Mohan A/c | 950 | ||

| Mar. 15 | To Sale A/c* | 25,000 | Mar. 6 | By Bank A/c | 40,000 | ||

| Mar. 15 | To Output CGST A/c | 1,500 | Mar. 6 | By Office Furniture A/c* | 4,650 | ||

| Mar. 15 | To Output SGST A/c | 1,500 | Mar. 6 | By Input CGST A/c | 279 | ||

| Mar. 19 | To Mr. Trilok Chand A/c | 4,850 | Mar. 6 | By Input SGST A/c | 279 | ||

| Mar. 12 | By Wages A/c | 1,200 | |||||

| Mar. 13 | By Stationery A/c* | 400 | |||||

| Mar. 13 | By Input CGST A/c | 24 | |||||

| Mar. 13 | By Input SGST A/c | 24 | |||||

| Mar. 17 | By Misc. Expenses A/c | 450 | |||||

| Mar. 22 | By Purchase A/c* | 2,500 | |||||

| Mar. 22 | By Input CGST A/c | 150 | |||||

| Mar. 22 | By Input SGST A/c | 150 | |||||

| Mar. 22 | By Salary A/c | 4,000 | |||||

| Mar. 25 | By Rent A/c* | 900 | |||||

| Mar. 25 | By Input CGST A/c | 54 | |||||

| Mar. 25 | By Input SGST A/c | 54 | |||||

| Mar. 22 | By Electricity A/c | 350 | |||||

| Mar. 29 | By Advertising A/c* | 400 | |||||

| Mar. 29 | By Input CGST A/c | 24 | |||||

| Mar. 29 | By Input SGST A/c | 24 | |||||

| Mar. 31 | By Bank A/c* | 25,000 | |||||

| Mar. 30 | By Balance C/d | 41,916 | |||||

| 1,31,450 | 1,31,450 | ||||||

All transactions which are highlighted with (*) are explained as following as follows: –

*Mar.03 Bought goods for cash, CGST and SGST @ 6% each 6,850

The calculation of Amount of CGST and SGST @ 6% each.

6,850 * 6% = 411/- each

*Mar.06 Paid for office furniture in cash, CGST and SGST paid @ 6% each 4,650

The calculation of Amount of CGST and SGST @ 6% each

4,650 * 6% = 279/- each

*Mar.09 Sold goods for cash charged CGST and SGST @ 6% each 30,000

The calculation of Amount of CGST and SGST @ 6% each

30,000 * 6% = 1,800/- each

*Mar.13 Paid for stationery, CGST and SGST paid @ 6% each 400

The calculation of Amount of CGST and SGST @ 6% each

400 * 6% = 24/- each

*Mar.15 Sold goods for cash, Charged CGST and SGST @ 6% each 25,000

The calculation of Amount of CGST and SGST @ 6% each

25,000 * 6% = 1,500/- each

*Mar.22 Purchased goods, CGST and SGST paid @ 6% each 2,500

The calculation of Amount of CGST and SGST @ 6% each.

2,500 * 6% = 150/- each

*Mar.25 Paid rent, CGST and SGST paid @ 6% each 900

The calculation of Amount of CGST and SGST @ 6% each

900 * 6% = 54/- each

*Mar.29 Paid for advertising, CGST and SGST paid @ 6% each 400

The calculation of Amount of CGST and SGST @ 6% each

400 * 6% = 24/- each

To understand more about cash book please check out following links: –

Cash Book | Types of Cash Book | Subsidiary Books

Single Column Cash Book | Explained with Example

Double Column Cash Book | Explained with Example

Triple Column Cash Book | Explained with Example

Petty Cash Book | Example | Subsidiary Books

Thanks Please share with your friends

Comment if you have any question.

Also, Check out previous Chapters: –

- Chapter No. 5 – Accounting Equation

- Chapter No. 6 – Accounting Procedures – Rules of Debit and Credit

- Goods and Services Tax(GST)

- Chapter No. 8 – Journal

- Chapter No. 9 – Ledger

Check out T.S. Grewal +1 Book 2019 @ Official Website of Sultan Chand Publication

T.S. Grewal’s Double Entry Book Keeping