Question 6 Chapter 5 – Unimax

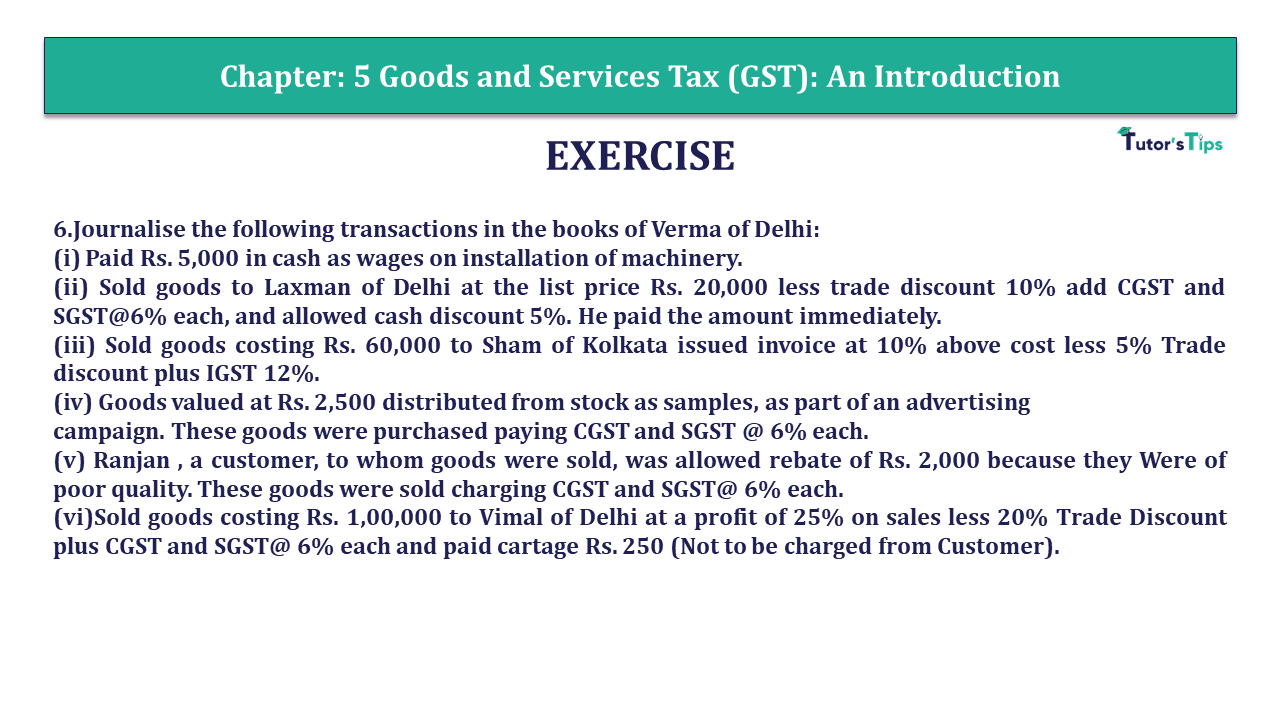

6.Journalise the following transactions in the books of Verma of Delhi:

(i) Paid Rs. 5,000 in cash as wages on installation of machinery.

(ii) Sold goods to Laxman of Delhi at the list price Rs. 20,000 less trade discount 10% add CGST and SGST@6% each, and allowed cash discount 5%. He paid the amount immediately.

(iii) Sold goods costing Rs. 60,000 to Sham of Kolkata issued invoice at 10% above cost less 5% Trade discount plus IGST 12%.

(iv) Goods valued at Rs. 2,500 distributed from stock as samples, as part of an advertising

campaign. These goods were purchased paying CGST and SGST @ 6% each.

(v) Ranjan , a customer, to whom goods were sold, was allowed rebate of Rs. 2,000 because they Were of poor quality. These goods were sold charging CGST and SGST@ 6% each.

(vi)Sold goods costing Rs. 1,00,000 to Vimal of Delhi at a profit of 25% on sales less 20% Trade Discount plus CGST and SGST@ 6% each and paid cartage Rs. 250 (Not to be charged from Customer).

The solution of Question 6 Chapter 5 – Unimax:

JOURNAL OF VERMA

| Date | Particulars | L.F. | Debit | Credit | |

| (i) | Machinery A/c * | Dr. | 5,000 | ||

| To Cash A/c | 5,000 | ||||

| (Being the wages paid on installation of a machinery) | |||||

| (ii) | Cash A/c (WN 1) | Dr. | 19,152 | ||

| Discount Allowed A/c | Dr. | 1,008 | |||

| To Sales A/c | 18,000 | ||||

| To Output CGST A/c | 1,080 | ||||

| To Output SGST A/c | 1,080 | ||||

| (Being the goods worth 20,000 sold, charged CGST and SGST 6% each, allowed 10% trade discount and 5% Cash discount) | |||||

| (iii) | Sham A/c | Dr. | 70,224 | ||

| To Sales A/c | 62,700 | ||||

| To Output IGST A/c | 7,524 | ||||

| (Being the goods supplied of 66,000 (i.e., 60,000+ 10% Of 60,000 plus IGST 12%) allowed 5% trade discount (i.e., 66,000- 3,300)) | |||||

| (iv) | Advertisement A/c | Dr. | 2,800 | ||

| To Purchases A/c | 2,500 | ||||

| To Input CGST A/c | 150 | ||||

| To Input SGST A/c | 150 | ||||

| (Being the goods distributed as free samples, Input CGST and Input SGST reversed) | |||||

| (v) | Rebate A/c | Dr. | 2,000 | ||

| Output CGST A/c | Dr. | 120 | |||

| Output SGST A/c | Dr. | 120 | |||

| To Ranjan A/c | 2,240 | ||||

| (Being the rebate allowed, Output CGST and SGST Reversed) | |||||

| (vi) | Vimal A/c | Dr. | 1,12,000 | ||

| To Sales A/c | 1,00,000 | ||||

| To Output CGST A/c | 6,000 | ||||

| To Output SGST A/c | 6,000 | ||||

| (Being the goods sold on credit, charging CGST and SGST 6% each) | |||||

| Cartage Outwards A/c | Dr. | 250 | |||

| To Cash A/c | 250 | ||||

| (Being the cartage paid) | |||||

Note: Installation charge is a capital expenditure, thus, is debited to the Machinery Account not paid, it being wages paid, which is not subject to levy of GST.

Working Notes :

1. Sale of Goods to Laxman, Delhi :

| Trade discount is not shown separately in the books of account. | ₹ |

| List Price | 20,000 |

| Less : Trade Discount @ 10% | 2,000 |

| 18,000 | |

| Add: CGST @ 6% | 1,080 |

| SGST @ 6% | 1,080 |

| 20,160 | |

| Less : Cash Discount @ 5% | 1,008 |

| Net Amount | 19,152 |

2. Calculation of Sales Price for Transaction (vi)

| ₹ | |

| Cost of Goods Sold | 1,00,000 |

| Add: Profit (25%) | 25,000 |

| 1,25,000 | |

| Less: Trade Discount (20%) | 25,000 |

| Sale Value | 1,00,000 |

This is all about the Question 6 Chapter 5 – Unimax. You can check out the following article to better understand:

Opening Journal Entry – its Rules and Examples

You Can also read all above articles in Hindi on our Hindi Website

Opening Journal Entry – its Rules and Examples – In Hindi

Thanks, Please Like and share with your friends

Comment if you have any doubt in the Question 6 Chapter 5 – Unimax.

You can also Check out the solved question of other Chapters: –

Advanced Accountancy – Unimax Class 11 – 2021 – Solution.

Part-I

- Chapter No. 1 – Introduction of Accounting

- Chapter No. 2 – Theory Base of Accounting

- Chapter No. 3 – Vouchers and Transactions

- Chapter No. 4 – Journal

- Chapter No. 5 – Goods and Services Tax (GST) : An Introduction

- Chapter No. 6 – Ledger

- Chapter No. 7 – Special Purpose Book – Cash Book

- Chapter No. 8 – Other Subsidiary Books

- Chapter No. 9 – Trial Balance

- Chapter No. 10 – Rectification of Errors

- Chapter No. 11 – Depreciation

- Chapter No. 12 – Provision and Reserves

- Chapter No. 13 – Bank Reconlciliation Statement

- Chapter No. 14 – Bills of Exchange

Students may Choose only one part from the Part II and Part III

Part-II

- Chapter No. 15 – Financial Statements (Without Adjustments)

- Chapter No. 16 – Financial Statements (With Adjustments)

- Chapter No. 17 – Accounts from Incomplete Records – Single Entry System

Part-III

- Chapter No. 18 – Introduction to Compurters and Accounting information System

- Chapter No. 19 – Computerised Accounting

- Chapter No. 20 – Accounting Software : Tally

- Chapter No. 21 – Data Base System

- Chapter No. 22 – Concept of Entity and Relationship

You can also Check out the other Books’ Solution: –

- Usha Publication – Elements of Book-Keeping PSEB (Class 11) – Solution

- T.S. Grewal’s Double Entry Book Keeping (Class +1) – Solution

- D K Goel – New ISC Accountancy -(Class 11 – ICSE)- Solution