Question 57 Chapter 5 of +2-B

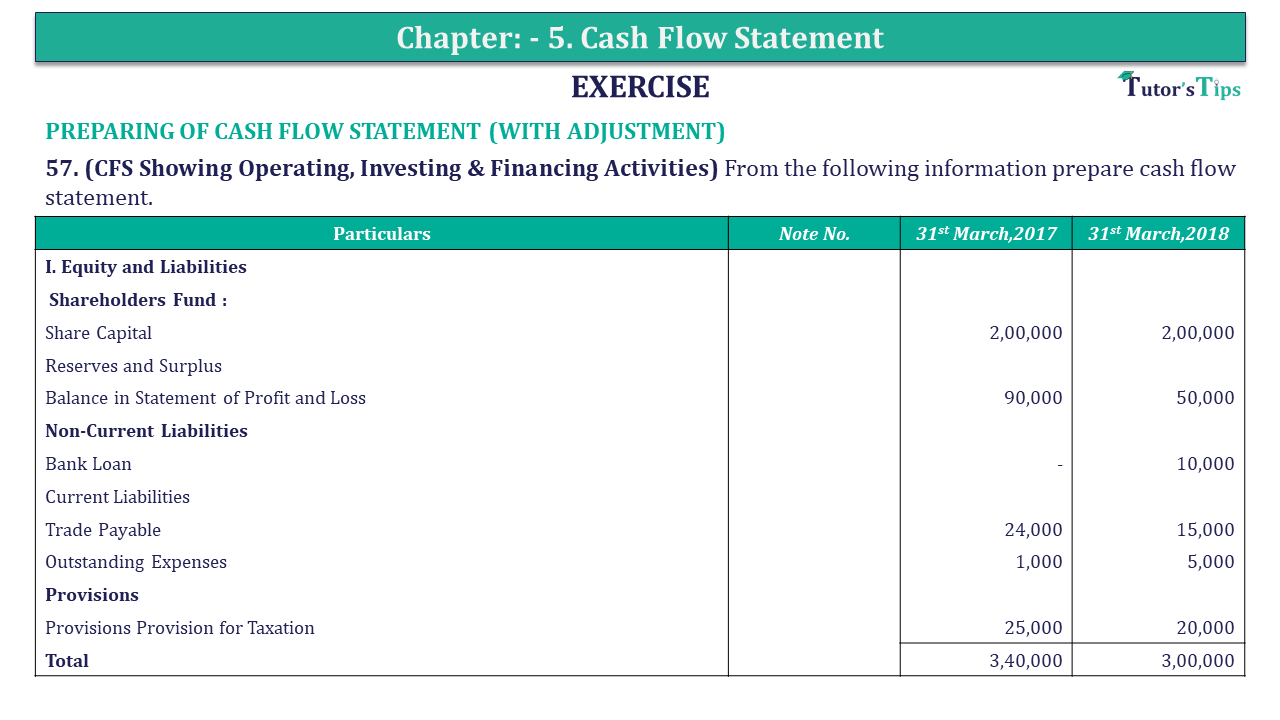

57. (CFS Showing Operating, Investing & Financing Activities) From the following information prepare cash flow statement.

| Particulars | Note No. | 31st March,2018 | 31st March,2017 |

| I. Equity and Liabilities | |||

| Shareholders Fund : | |||

| Share Capital | 2,00,000 | 2,00,000 | |

| Reserves and Surplus | |||

| Balance in Statement of Profit and Loss | 90,000 | 50,000 | |

| Non-Current Liabilities | |||

| Bank Loan | – | 10,000 | |

| Current Liabilities | |||

| Trade Payable | 24,000 | 15,000 | |

| Outstanding Expenses | 1,000 | 5,000 | |

| Provisions | |||

| Provisions Provision for Taxation | 25,000 | 20,000 | |

| Total | 3,40,000 | 3,00,000 | |

| II. Assets | |||

| Non-Current Assets : | |||

| Current Assets : | 2,00,000 | 2,00,000 | |

| Inventories | |||

| Trade Receivable | 90,000 | 50,000 | |

| Cash and Cash Equivalents – Cash | |||

| Bank | – | 10,000 | |

| Total | 3,40,000 | 3,00,000 |

Net profit for the year 2017-18 after providing ₹ 20,000 as depreciation was ₹ 60,000. During 2017-18, Company declared an equity dividend of @10% and paid ₹ 15,000 as income tax.

The solution of Question 57 Chapter 5 of +2-B: –

| Cash Flow Statement for the year ended 31st March 2018 |

||

| Particulars |

Rs |

|

| (A) Cash Flow from Operating Activities | ||

| Net Profit before Tax and Extraordinary Items* | 40,000 | |

| Adjustment of non-Cash & Non-Operating Items | ||

| Add: Depreciation Charged | 20,000 | |

| Provision for Taxation | 20,000 | 40,000 |

| Cash operating Profit before Working Capital adj. | 80,000 | |

| Add: Increase in Current Liabilities: | ||

| Trade Payable | 9,000 | |

| Add: Decrease in current Assets: | ||

| Inventories | 10,000 | 19,000 |

| Less: Decrease in current Liabilities: | 99,000 | |

| Outstanding Expenses | 4,000 | |

| Less: Increase in current Assets: | ||

| Trade Receivables | 10,000 | 14,000 |

| 85,000 | ||

| Less: Tax Paid | 15,000 | |

| Cash flow from Operating Activities | 70,00 |

|

| (B) Cash flows from Investing Activities | ||

| Inflow of Cash | ||

| Purchase of Non-current Assets* | 60,000 | |

| Net cash used in investing Activities | 60,000 |

|

| (C) Cash flows from Financing Activities | ||

| Outflow of Cash | ||

| Repayment of Bank Loan | 10,000 | |

| Net cash flow from financing activities | 10,000 |

|

| Net Increase in Cash & Cash Equivalents (A + B + C) | Nil | |

| Add: Cash & Cash equivalents in the beginning | 30,000 | |

| Cash & Cash equivalents at the end | 30,000 | |

End of Solution

Check Out the Solution of all questions of this chapter:

The solution to all questions of Chapter No. 15 – Cash Flow Statement Class 12 Usha Publication – 2024 is shown as follows, click on the image of the question to get the solution.

Thanks for completing the chapter. If you understand the question or we have helped you with your homework, please share our website on your social media. We are delighted to help you out.

Thanks again.

End of Post

Download a PDF of Chapter No. 15 – Cash Flow Statement:

If you want to download a PDF of this chapter then you can do it. Check out our PDF file on our Store page.

Chapter-Wise Solution of Usha Publication Accountancy – Part 2 Class 12 – Session 2024-25 as per the PSEB curriculum

Check out Solutions to all questions of the every chapter shown as under. The Solution of Accountancy – Part 2 Class 12 – Session 2024-25 is provided as per the new book published by Usha Publication.

Chapter No. 8 – Company Accounts (Share Capital)

Chapter No. 9 – Company Accounts (Issue of Debentures)

Chapter No. 10 – Company Accounts (Redemption of Debentures)

Chapter No. 11 – Financial Statements of a Company

Chapter No. 12 – Financial Statement Analysis

Chapter No. 13 – Tools of Financial Statement Analysis- Comparative and Common Size

Chapter No. 14 – Accounting Ratios

Chapter No. 15 – Cash Flow Statement

Also, Check out our Comprehensive Chapter-wise solution of Advanced Accountancy Part 2 Class 12 by Unimax Publication

- Chapter No. 1 – Company Accounts (Share Capital)

- Chapter No. 2 – Issue of Debentures

- Chapter No. 3 – Redemption of Debentures

- Chapter No. 4 – Financial Statements of a Company (Balance Sheet Only)

- Chapter No. 5 -Financial Statement Analysis

- Chapter No. 6 – Tools/Methods of Financial Analysis

- Chapter No. 7 – Ratio Analysis

- Chapter No. 8 – Cash Flow Statement

Check out Part 1 of both books.

In Class 12th the accountancy has 2 books i.e. Part 1 and Part 2. The Books related to the Part 1 are shown above. but If you want to know more about Part 1, you can check it out from the following links. We have provided the links to both books i.e. Accountancy Part 1 by Usha Publication and Advanced Accountancy Part 2 by Unimax Publication.

1. Accountancy – Part 1 Class 12 – Session 2024-25 By Usha Publication

2. Advanced Accountancy Part 1 Class 12 by Unimax Publication