In Cashbook, we will record the all-cash transaction of the business. This book keeps a record of all cash payments and cash receipts. In this article, we will discuss the Triple Column Cash Book, its format and example.

What is the Triple Column Cash Book?

In Triple Column Cash Book there are three columns in the cash book because every Businessman has a minimum of one current account in the bank. It is a very convenient way for him to get paid by cheque and make payments to others by cheque. So, he has to record these payments and receipts in the cash book for this an additional column will require a named bank column. So now a total three-column will be required to record the proper payment and receipts in the cash book these are shown below

- Cash Column

- Bank Column

- Discount Column

The format of the triple Column Cash Book:

The format of the triple Column Cash Book is explained as under:

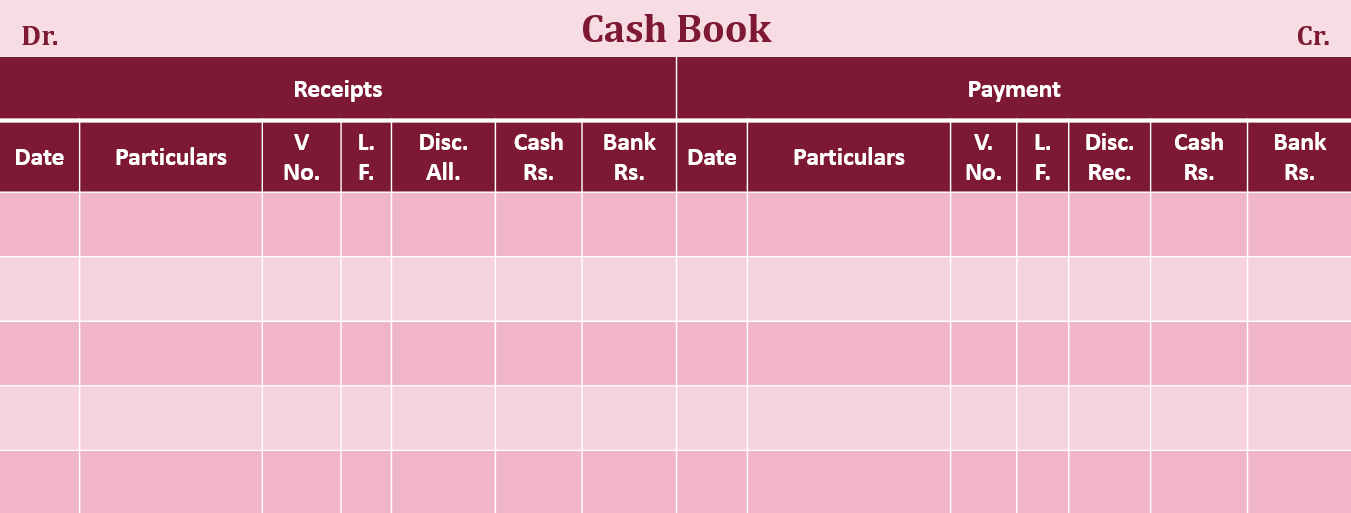

The Columns of the Triple Column Cash Book are explained Below:-

- Date:

- Particulars:

- V. NO (Voucher Number):

- L.F. (Ledger Folio):

- Amount ( It Included three columns i.e. 1. Discount, 2. Cash and 3. Bank.)

Explanation of all columns:

1. Date:

The date of the transaction is written in this column —in the first row, we will write the year till it will not change and in the subsequent rows, write the name of the month followed by the actual date.

2. Particulars:

In this column, the name of the opposite account is written (the second aspect of cash transaction). Below is written the narration of the transaction.

3. Voucher Number (V. NO.):

The voucher number for each item of receipt and payment is also written. A voucher is necessary for each item of receipt and payment. Generally, a voucher has a serial number and this number is written in this column (V. No).

4. L.F. (Ledger Folio):

The page number of the Ledger where the concerned (opposite ) account has been opened, is written in this column. This will help to locate the account from the Ledger. It may be noted that in a Ledger account, J.F. is written as the reference, while in a Cash Book L.F. is written.

5. Amount Columns:

All the Above columns are the same as the single & double-column cash book but instead of the amount column, three different columns are prepared i.e. 1. Discount, 2. Cash and 3. Bank.

1. Discount Column:

In the discount Column, we have to record the discount received on the credit side of the cash book and the discount allowed on the debit side of the cash book.

2. Cash Column:

All the payments and receipts made by cash are recorded in this column.

3. Bank Column:

All the payments and receipts made by the bank/ Cheque are recorded in this column.

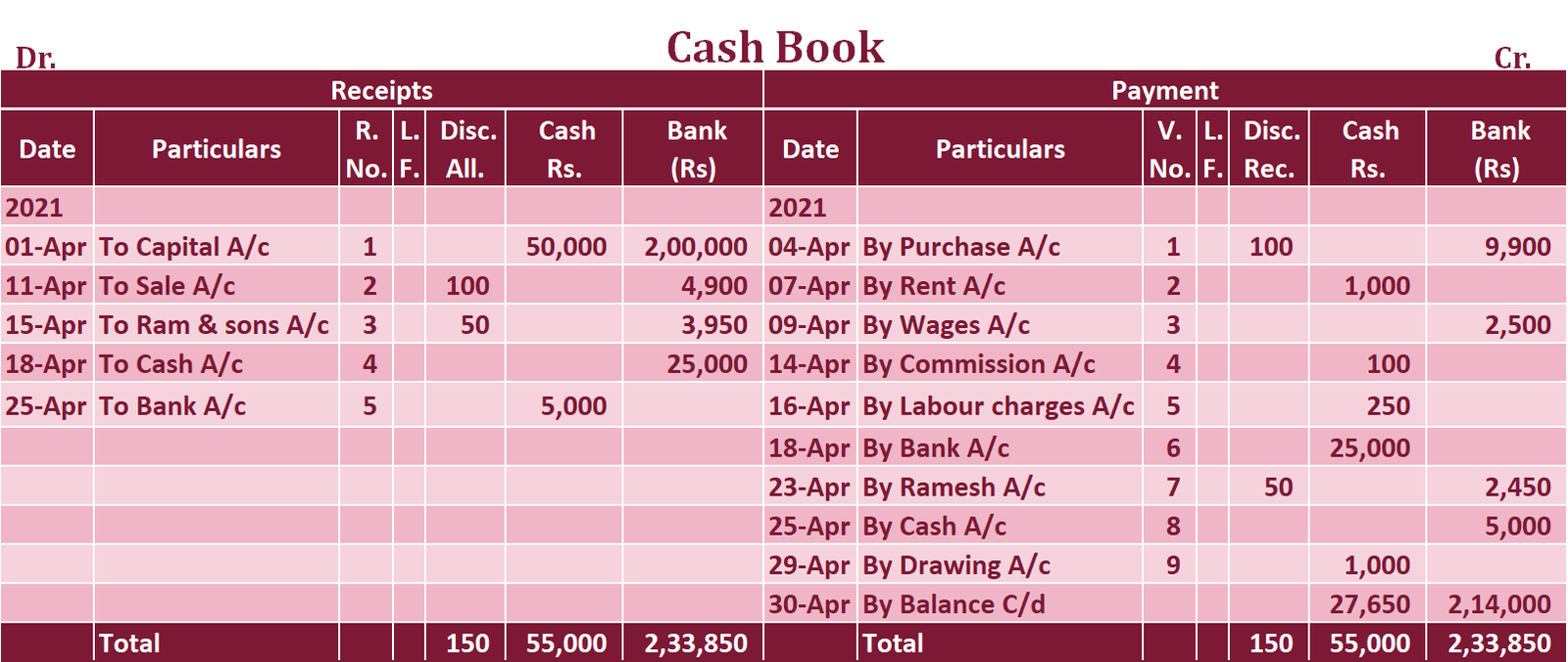

Example of Triple Column Cash Book :

Prepare the triple-column cash book from the following business transactions:

- 01/04/21 Started a business with cash Rs 50,000/- and bank balance of Rs 2,00,000/-

- 04/04/21 Goods purchase worth Rs 10,000/- and payment made immediately By cheque and get discount Rs 100/-

- 07/04/21 Rent paid for the building Rs 1,000/-

- 09/04/21 Wages paid for Rs 2,500/- by Cheque

- 11/04/21 Sold goods worth Rs 5,000/- and to receive payment immediately by cheque and allow discount Rs 100/-

- 12/04/21 Sold goods to Ram & sons Rs 4,000/-

- 14/04/21 Commission paid to Rohan Rs 100/-

- 15/04/21 Payment received from Ram & Sons Rs 3,950 by cheque. and allowed them a discount of Rs 50/-

- 16/04/21 Labour charges paid for Rs 250/-

- 18/04/21 Cash deposited into Bank Rs 25,000/-

- 21/04/21 Purchased goods worth Rs 2,500/- from Ramesh.

- 23/04/21 Payment made to Ramesh Rs 2,450 by Cheque and received the discount of Rs. 50/-

- 25/04/21 Cash withdrawal from Bank for office use Rs 5,000/-.

- 29/04/21 An owner withdraw cash from the business for personal use of Rs1,000.

Solution: –

Note: –

Transaction Dated 12/04/17 & 21/04/17 are not recorded in the cash book because these are credit business transactions.

If you have any questions about this topic of Triple Column Cash Book please ask it in the comment section below.

Thanks

Check out Financial Accounting Books @ Amazon. in