Question No 48 Chapter No 17

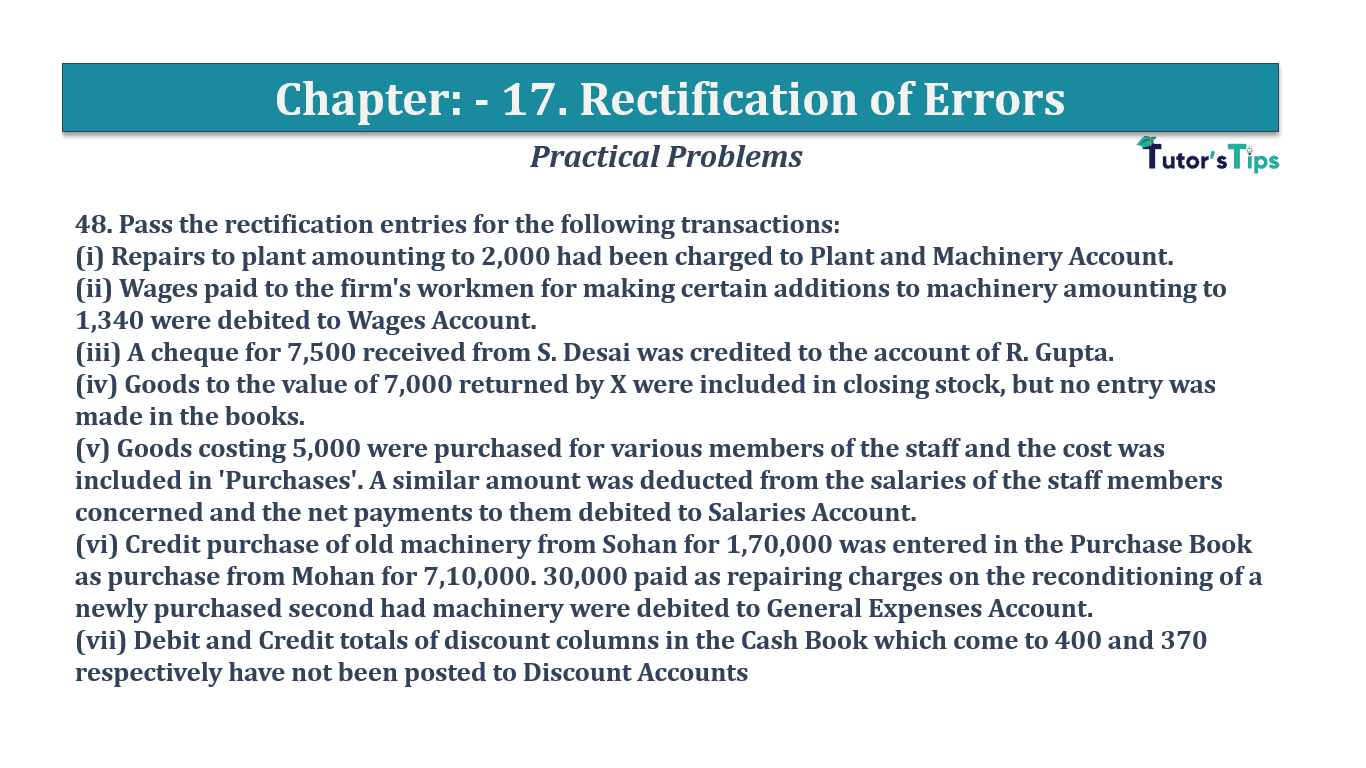

48. Pass the rectification entries for the following transactions:

(i) Repairs to plant amounting to 2,000 had been charged to Plant and Machinery Account.

(ii) Wages paid to the firm’s workmen for making certain additions to machinery amounting to 1,340 were debited to Wages Account.

(iii) A cheque for 7,500 received from S. Desai was credited to the account of R. Gupta.

(iv) Goods to the value of 7,000 returned by X were included in closing stock, but no entry was made in the books.

(v) Goods costing 5,000 were purchased for various members of the staff and the cost was included in ‘Purchases’. A similar amount was deducted from the salaries of the staff members concerned and the net payments to them debited to Salaries Account.

(vi) Credit purchase of old machinery from Sohan for 1,70,000 was entered in the Purchase Book as purchase from Mohan for 7,10,000. 30,000 paid as repairing charges on the reconditioning of a newly purchased second had machinery were debited to General Expenses Account.

(vii) Debit and Credit totals of discount columns in the Cash Book which come to 400 and 370 respectively have not been posted to Discount Accounts

The solution of Question No 48 Chapter No 16:-

| Date | Particulars |

L.F. | Debit | Credit | |

| i | Repairs A/c | Dr. | 2,000 | ||

| To Plant and Machinery A/c | 2,000 | ||||

| (Being Repairs wrongly capitalised, now rectified) | |||||

| ii | Machinery A/c | Dr. | 1,340 | ||

| To Wages A/c | 1,340 | ||||

| (Being Wages paid to Workmen for certain addition to Machinery wrongly debited to Wages Account, now rectified) | |||||

| iii | R. Gupta | Dr. | 7,500 | ||

| To S. Desa | 7,500 | ||||

| (Being Cheque of Rs 7,500 received from S. Desai was wrongly Credited to R. Gupta’s Account, now rectified) | |||||

| iv | Sales Return A/c | Dr. | 7,000 | ||

| To X A/c | 7,000 | ||||

| (Being Goods returned by X had not recorded in the book, now rectified) | |||||

| v | Salaries A/c | Dr. | 5,000 | ||

| To Purchases A/c | 5,000 | ||||

| (Being Goods purchased for Staff was wrongly debited to Purchases Account, now rectified) | |||||

| vi | Mohan A/c | Dr. | 7,10,000 | ||

| Machinery A/c | Dr. | 2,00,000 | |||

| To Sohan A/c | 1,70,000 | ||||

| To Purchases A/c | 7,10,000 | ||||

| To General Expenses A/c | 30,000 | ||||

| (Being Credit purchase of an old machinery from Sohan and repairs charges were wrongly recoreded as purchase from Mohan and General Expenses, now rectified) | |||||

| vii(a) | Discount Allowed A/c | Dr. | 400 | ||

| To Suspense A/c | 400 | ||||

| (Being Discount allowed omitted to be recorded, now recorded) | |||||

| vii(b) | Suspense A/c | Dr. | 370 | ||

| To Discount Received A/c | 370 | ||||

| (Being Discount received omitted to be recorded, now recorded) | |||||

Error Rectification in accounting – Explanation with examples

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of previous Chapters: –

-

- Chapter No. 1 – Introduction to Accounting

- Chapter No. 2 – Basic Accounting Terms

- Chapter No. 3 – Theory Base of Accounting, Accounting Standards and International Financial Reporting Standards(IFRS)

- Chapter No. 4 – Bases of Accounting

- Chapter No. 5 – Accounting Equation

- Chapter No. 6 – Accounting Procedures – Rules of Debit and Credit

- Goods and Services Tax(GST)

- Chapter No. 7 – Origin of Transactions – Source Documents and Preparation of Vouchers

- Chapter No. 8 – Journal

- Chapter No. 9 – Ledger

- Chapter No. 10 – Special Purpose Books I – Cash Book

- Chapter No. 11 – Special Purpose Books II – Other Books

- Chapter No. 12 – Bank Reconciliation Statement

- Chapter No. 13 – Trial Balance

- Chapter No. 14 – Depreciation

- Chapter No. 15 – Provisions and Reserves

- Chapter No. 16 – Accounting for Bills of Exchange

- Chapter No. 17 – Rectification of Errors

- Chapter No. 18 – Financial Statements of Sole Proprietorship

- Chapter No. 19 – Adjustments in preparation of Financial Statements

- Chapter No. 20 – Accounts from incomplete Records – Single Entry System

- Chapter No. 21 – Computers in Accounting

- Chapter No. 22 – Accounting Software – Tally

- Chapter No. 5 – Accounting Equation

- Chapter No. 6 – Accounting Procedures – Rules of Debit and Credit

- Goods and Services Tax(GST)

- Chapter No. 8 – Journal

- Chapter No. 9 – Ledger

- Chapter No. 10 – Special Purpose Books I – Cash Book

Check out T.S. Grewal +1 Book 2019 @ Official Website of Sultan Chand Publication

T.S. Grewal’s Double Entry Book Keeping