Question No 10 Chapter No 9

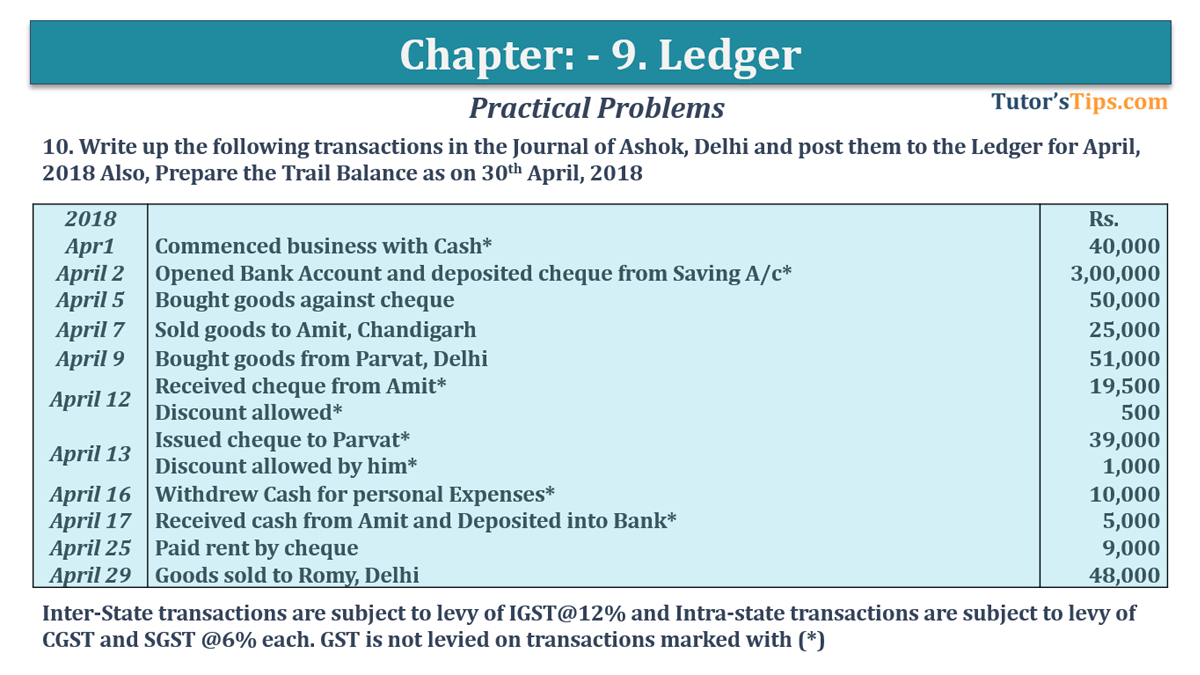

Write up the following transactions in the Journal of Ashok, Delhi and post them to the Ledger for April, 2018 Also, Prepare the Trail Balance as on 30th April, 2018: –

| 2018 | Rs. | |

| Apr-01 | Commenced business with Cash* | 40,000 |

| Apr-02 | Opened Bank Account and deposited cheque from Saving A/c* | 3,00,000 |

| Apr-05 | Bought goods against cheque | 50,000 |

| Apr-07 | Sold goods to Amit, Chandigarh | 25,000 |

| Apr-09 | Bought goods from Parvat, Delhi | 51,000 |

| Apr-12 | Received cheque from Amit* | 19,500 |

| Discount allowed* | 500 | |

| Apr-13 | Issued cheque to Parvat* | 39,000 |

| Discount allowed by him* | 1,000 | |

| Apr-16 | Withdrew Cash for personal Expenses* | 10,000 |

| Apr-17 | Received cash from Amit and Deposited into Bank* | 5,000 |

| Apr-25 | Paid rent by cheque | 9,000 |

| Apr-29 | Goods sold to Romy, Delhi | 48,000 |

Inter-State transactions are subject to levy of IGST@12% and Intra-state transactions are subject to levy of CGST and SGST @6% each. GST is not levied on transactions marked with (*).

Solution of Question No 10 Chapter No 9: –

In the Books of Ashok, Delhi

| Date | Particulars |

L.F. | Debit | Credit | |

| 2018 | |||||

| Apr. 1 | Cash A/c | Dr. | 40,000 | ||

| To Capital A/c | 40,000 | ||||

| (Being business commenced with Cash) | |||||

| Apr. 2 | Bank A/c | Dr. | 3,00,000 | ||

| To Capital A/c | 3,00,000 | ||||

| (Being opened Bank Account and deposited cheque from saving A/c) | |||||

| Apr. 5 | Purchase A/c | Dr. | 50,000 | ||

| Input CGST A/c | Dr. | 3,000 | |||

| Input SGST A/c | Dr. | 3,000 | |||

| To Bank A/c | 56,000 | ||||

| (Being goods bought against cheque) | |||||

| Apr. 7 | Amit, Chandigarh A/c | Dr. | 28,000 | ||

| To Sale A/c | 25,000 | ||||

| To Output IGST A/c | 3,000 | ||||

| (Being Goods Sold to Amit, Chandigarh) | |||||

| Apr. 9 | Purchase A/c | Dr. | 51,000 | ||

| Input CGST A/c | Dr. | 3,060 | |||

| Input SGST A/c | Dr. | 3,060 | |||

| To Parvat, Delhi A/c | 57,120 | ||||

| (Being Goods Purchase from Parvat, Delhi) | |||||

| Apr. 12 | Bank A/c | Dr. | 19,500 | ||

| Discount Allowed A/c | Dr. | 500 | |||

| To Amit, Chandigarh A/c | 20,000 | ||||

| (Being payment received by cheque from Amit, Chandigarh) | |||||

| Apr. 13 | Parvat, Delhi A/c | Dr. | 40,000 | ||

| To Bank A/c | 39,000 | ||||

| To Discount Received A/c | 1,000 | ||||

| (Being Payment made by cheque to Parvat, Delhi ) | |||||

| Apr. 16 | Drawing A/c | Dr. | 10,000 | ||

| To Cash A/c | 10,000 | ||||

| (Being Cash withdrew for personal use ) | |||||

| Apr. 17 | Cash A/c | Dr. | 5,000 | ||

| To Amit, Chandigarh A/c | 5,000 | ||||

| (Being Cash received from Amit, Chandigarh) | |||||

| Apr. 15 | Bank A/c | Dr. | 5,000 | ||

| To Cash A/c | 5,000 | ||||

| (Being Cash deposited into Bank ) | |||||

| Apr. 25 | RentA/c | Dr. | 9,000 | ||

| Input CGST A/c | Dr. | 540 | |||

| Input SGST A/c | Dr. | 540 | |||

| To Bank A/c | 10,080 | ||||

| (Being rent paid by cheque) | |||||

| Apr. 15 | Romy, Delhi A/c | Dr. | 53,760 | ||

| To Sale A/c | 48,000 | ||||

| To Output CGST A/c | 2,880 | ||||

| To Output SGST A/c | 2,880 | ||||

| (Being Goods Sold to Romy, Delhi) | |||||

To clear the meaning of Ledger and Ledger balancing Click below:

What is Ledger in accounting – explain its Types

Ledger balancing or Closing of ledger account | Ledger

| Dr. | Cash A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 1 | To Capital A/c | 40,000 | Apr. 16 | By DrawingA/c | 10,000 | ||

| Apr. 17 | To Amit A/c | 5,000 | Apr. 17 | By Bank A/c | 5,000 | ||

| Apr. 30 | By Balance C/d | 30,000 | |||||

| 20,000 | 20,000 | ||||||

| Dr. | Capital A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 1 | By Cash A/c | 40,000 | |||||

| Apr. | By Bank A/c | 3,00,000 | |||||

| Apr. 30 | To Balance C/d | 3,40,000 | |||||

| 3,40,000 | 3,40,000 | ||||||

| Dr. | Bank A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 2 | To Capital A/c | 3,00,000 | Apr. 5 | By Purchase A/c | 50,000 | ||

| Apr. 12 | To Amit Chandigarh A/c | 19,500 | Apr. 5 | By Input CGST A/c | 3,000 | ||

| Apr. 12 | To Cash A/c | 5,000 | Apr. 5 | By Input SGST A/c | 3,000 | ||

| Apr. 27 | By Parvat, Delhi A/c | 39,000 | |||||

| Apr. 27 | By Rent A/c | 9,000 | |||||

| Apr. 5 | By Input CGST A/c | 540 | |||||

| Apr. 5 | By Input SGST A/c | 540 | |||||

| Apr. 30 | By Balance C/d | 2,19,420 | |||||

| 3,24,500 | 3,24,500 | ||||||

| Dr. | Purchase A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 5 | To Bank A/c | 50,000 | |||||

| Apr. 9 | To Parvat, Delhi A/c | 51,000 | |||||

| Apr. 30 | By Balance C/d | 1,01,000 | |||||

| 1,01,000 | 1,01,000 | ||||||

| Dr. | Sales A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 7 | By Amit, Chandigarh A/c | 28,000 | |||||

| Apr. 29 | By Romy, Delhi A/c | 48,000 | |||||

| Apr. 30 | To Balance C/d | 76,000 | |||||

| 76,000 | 76,000 | ||||||

| Dr. | Amit, Chandigarh A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 7 | To Sales A/c | 25,000 | Apr. 12 | By Bank A/c | 19,500 | ||

| Apr. 7 | To Output IGST A/c | 3,000 | Apr. 12 | By Discount Allowed A/c | 500 | ||

| Apr. 18 | By Cash A/c | 5,000 | |||||

| Apr. 30 | By Balance C/d | 3,000 | |||||

| 28,000 | 28,000 | ||||||

| Dr. | Parvat, Delhi A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 7 | To Bank A/c | 39,000 | Apr. 12 | By Purchase A/c | 51,000 | ||

| Apr. 7 | To Discount Received A/c | 1,000 | Apr. 12 | By Input CGST A/c | 3,060 | ||

| Apr. 12 | By Input SGST A/c | 3,060 | |||||

| Apr. 30 | To Balance C/d | 17,120 | |||||

| 57,120 | 57,120 | ||||||

| Dr. | Romy, Delhi A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 7 | To Sales A/c | 48,000 | |||||

| Apr. 7 | To Output CGST A/c | 2,880 | |||||

| Apr. 7 | To Output SGST A/c | 2,880 | |||||

| Apr. 30 | By Balance C/d | 53,760 | |||||

| 53,760 | 53,760 | ||||||

| Dr. | Drawing A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 16 | To Cash A/c | 10,000 | Apr. 30 | By Balance C/d | 10,000 | ||

| 1,500 | 1,500 | ||||||

| Dr. | Discount Allowed A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 10 | To Amit, Chandigarh A/c | 500 | Apr. 30 | By Balance C/d | 500 | ||

| 500 | 500 | ||||||

| Dr. | Discount Received A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 13 | By Parvat, Delhi A/c | 1,000 | |||||

| Apr. 30 | To Balance C/d | 1,000 | |||||

| 1,000 | 1,000 | ||||||

| Dr. | Input CGST A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 5 | To Bank A/c | 3,000 | |||||

| Apr. 8 | To Parvat, Delhi A/c | 3,060 | |||||

| Apr. 25 | To Rent A/c | 540 | |||||

| Apr. 30 | By Balance C/d | 6,600 | |||||

| 6,600 | 6,600 | ||||||

| Dr. | Input SGST A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 5 | To Bank A/c | 3,000 | |||||

| Apr. 8 | To Parvat, Delhi A/c | 3,060 | |||||

| Apr. 25 | To Rent A/c | 540 | |||||

| Apr. 30 | By Balance C/d | 6,600 | |||||

| 6,600 | 6,600 | ||||||

| Dr. | Output CGST A/c |

Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 29 | By Romy, Delhi A/c | 2,880 | |||||

| Apr. 30 | To Balance C/d | 2,880 | |||||

| 2,880 | 2,880 | ||||||

| Dr. | Output SGST A/c |

Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 29 | By Romy, Delhi A/c | 2,880 | |||||

| Apr. 30 | To Balance C/d | 2,880 | |||||

| 2,880 | 2,880 | ||||||

| Dr. | Output IGST A/c |

Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 10 | By Amit Chandigarh A/c | 3,000 | |||||

| Apr. 30 | To Balance C/d | 3,000 | |||||

| 3,000 | 3,000 | ||||||

| Trial Balance | |||

| Particulars |

L.F. | Debit | Credit |

| Cash A/c | 30,000 | ||

| Capital A/c | 3,40,000 | ||

| Bank A/c | 2,19,420 | ||

| Purchases A/c | 1,01,000 | ||

| Sale A/c | 73,000 | ||

| Amit, Chandigarh A/c | 3,000 | ||

| Parvat, Delhi A/c | 17,120 | ||

| Romy, Delhi A/c | 53,760 | ||

| Discount Allowed A/c | 500 | ||

| Discount Received A/c | 1,000 | ||

| Rent A/c | 9,000 | ||

| Input CGST A/c | 6,600 | ||

| Input SGST A/c | 6,600 | ||

| Output CGST A/c | 2,880 | ||

| Output SGST A/c | 2,880 | ||

| Output IGST A/c | 3,000 | ||

| 4,39,880 | 4,39,880 | ||

Thanks Please share with your friends

Comment if you have any question.

Check out previous questions: –

- Question No 34 Chapter No 8 – T.S. Grewal 11 Class

- Question No 33 Chapter No 8 – T.S. Grewal 11 Class

- Question No 32 Chapter No 8 – T.S. Grewal 11 Class

- Question No 31 Chapter No 8 – T.S. Grewal 11 Class

- Question No 30 Chapter No 8 – T.S. Grewal 11 Class

Check out T.S. Grewal +1 Book 2019 @ Oficial Website of Sultan Chand Publication

T.S. Grewal’s Double Entry Book Keeping