We have explained the whole topic of the ledger in the following parts to understand to proper meaning and utilization of it in financial accounting.

What is Ledger:

Ledger is a book in which we record all business transactions of each and every account in a separate ledger account. In other words, It is the summary of the single account. So we have to create a separate ledger for each and every account which are already created while recording journal entries.

These accounts are maintained in alphabetical order. With the help of the ledger accounts, we can get whole information about any particular account because all the related journal entries to the particular account are posted on the continuous pages of this book.

In the ledger accounts, we have to record date wise transactions related to a particular account, but in the journal, all the transactions are recorded only date wise and the name of the account has ignored. So if we want to know the balance of a particular account then it is very difficult to get it from Journal because we have to check and find out all transactions related to the particular accounts from all pages of the journal daybook.

Ledger accounts also have opening and closing balances but the journal doesn’t have.

Difference between Journal and Ledger

Examples of Ledger accounts:

The examples of ledger accounts are shown as follows:

- Cash A/c

- Bank

- Land and Building A/c

- Plant and Machine A/c

- Furniture and Fixture A/c

- Computer A/c

- Patent A/c

- Vehicle A/c

- Capital A/c

- Bank Loan A/c

- Purchases A/c

- Sales A/c

- Purchases Return A/c

- Sales Return A/c

- Wages A/c

- Freight and transportation A/c

- Electricity expenses A/c

- Water and Fuel A/c

- Salaries A/c

- Commission A/c

- Rent A/c

- Interest on loan A/c

- Telephone and Mobile Expenses A/c

- Printing and Stationery A/c

- Rent Received A/c

- Commission received A/c

- Etc.

The Types of Ledger:

It has three types shown as following:

- Debtor/Sale Ledger: All customers to whom goods are sold on credit are recorded in this type of ledger account.

- Creditors/Purchase Ledger: All vendors/ suppliers from whom goods are purchased on credit are recorded in this type of ledger account.

- General Ledger: All other accounts except Debtors and creditors are recorded in this ledger. like Current assets and fixed assets, Liabilities, Incomes & Expenses, Gains & losses.

The format of Ledger:

It has two sides, the left side is the debit side and the right side is the credit side. the format is shown as under :

1. The standard Format:

| Dr. |

Name of Account | Cr. |

|||||

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

2. An alternative format:

This format is now used more than the old one. In this format, Date, particulars and journal folio make common for both transactions debit or credit. Almost in all the accounting software, this format is used. it is shown below:

| Name of Account | |||||

| Date | Particulars | J.F. | Debit | Credit |

Balance |

How to Post transactions into the ledger from the journal:

Posting means recording the transaction in the ledger from the journal or other subsidiary books. First of all, every transaction recorded in the journal or cash book or purchase book or sale book or returns books and then it will post in the ledger. In the posting, we use the prefix on both the side “To” on the debit side and “By” on The credit side.

1. Posting process of a simple journal entry:

We will explain it to you in steps as shown below:

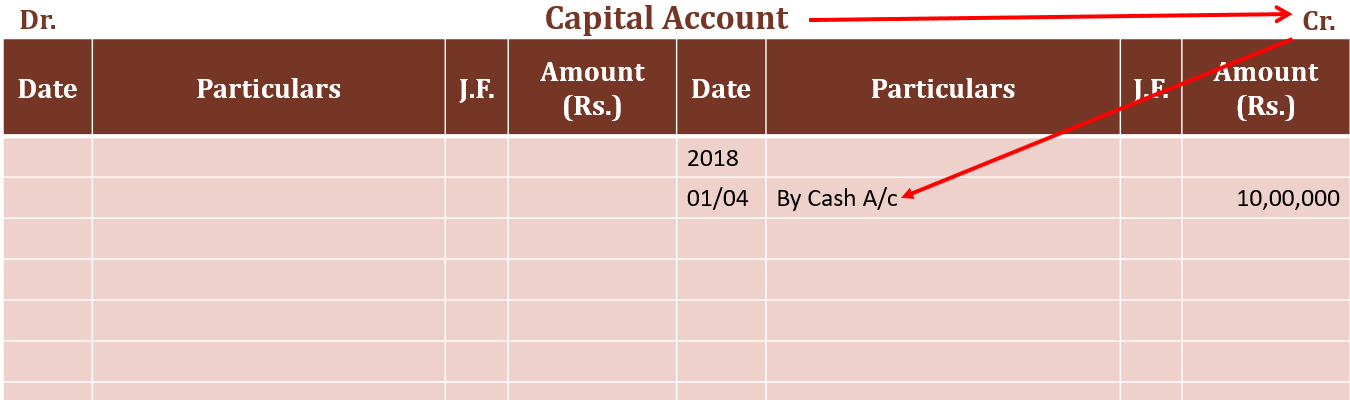

| 01/04/2018 | Cash a/c | Dr. | 10,00,000 | ||

| To capital a/c |

10,00,000 |

||||

| (Being capital introduced by owner) | |||||

Here we had operated two accounts

- Cash a/c

- Capital a/c

So, in cash a/c, we have to post the capital a/c

and in the capital a/c, we have to post the cash a/c as shown below:

This image shows the exact journal entry. Please read according to the direction of the arrows.

it shows cash a/c —->Dr —>To capital a/c.

In this image, it shows also the journal entry. Please read according to the direction of the arrows.

it shows capital a/c —->Cr. —>By Cash a/c.

This is the reason to use the prefix “To” on the Debit side ” & “By” on the Credit side” because it makes sense.

2. Posting of a compound journal entry into ledger:

we had already explained the meaning of compound journal entry if you did not remember then please click here. I will take the same example of the previous topic of the compound journal entry for easy understanding.

1. By debiting two or more accounts and credited only a single account:

Example 1:

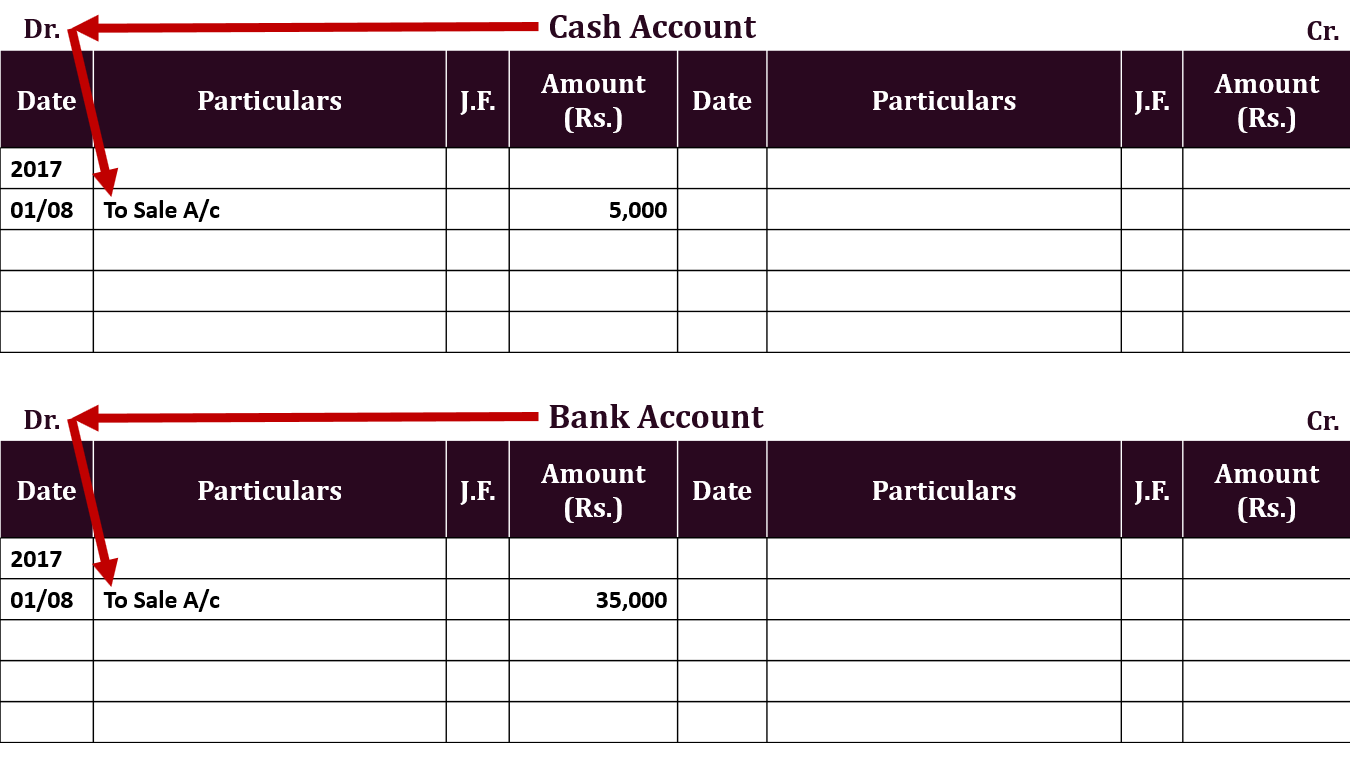

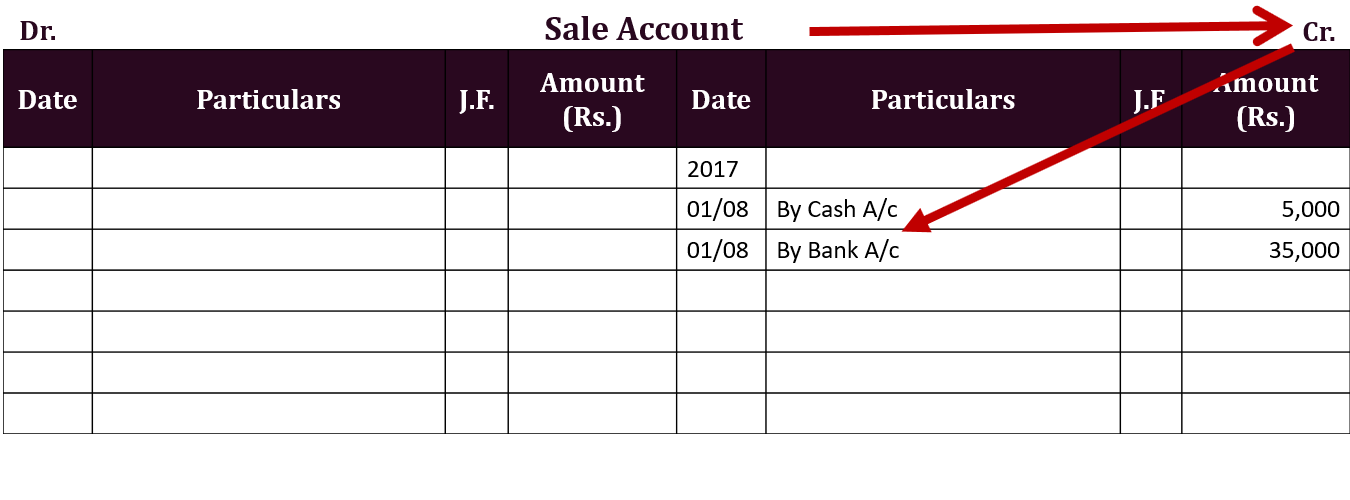

On Date 01/08/2017 Sold goods to Mr Rajan worth Rs. 40,000/- and He paid Rs. 5,000/- in cash and 35,000/- By cheque.

In this above transaction three accounts are involved shown as below:

- Cash A/c – Rs 5,000/- Cash received for it.

- Bank A/c – Balance payment made with the cheque.

- Sale A/c – Goods sold.

| Date | Particulars | L.F. | Debit | Credit | ||

| 01/08/2017 | Cash a/c | Dr. | 5,000 | |||

| Bank a/c | Dr. | 35,000 | ||||

| To Sales a/c | 40,000 | |||||

| (Being Sold goods to Mr Rajan worth Rs. 40,000/- and He paid Rs. 5,000/- in cash and 35,000/- By cheque) | ||||||

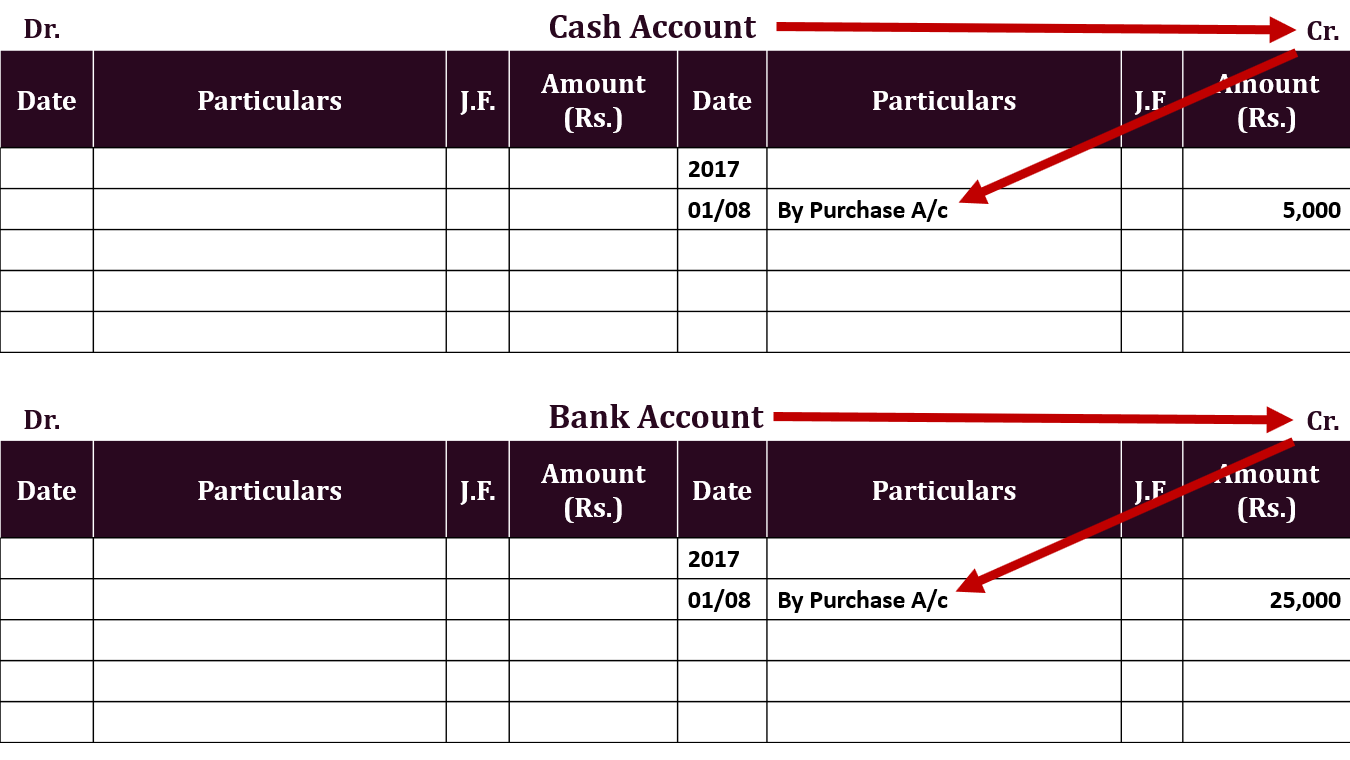

Post this transaction to the Ledger account as below:

Compound Journal Entry posted to Ledger Example

2. By debiting a single account and credited two or more accounts.

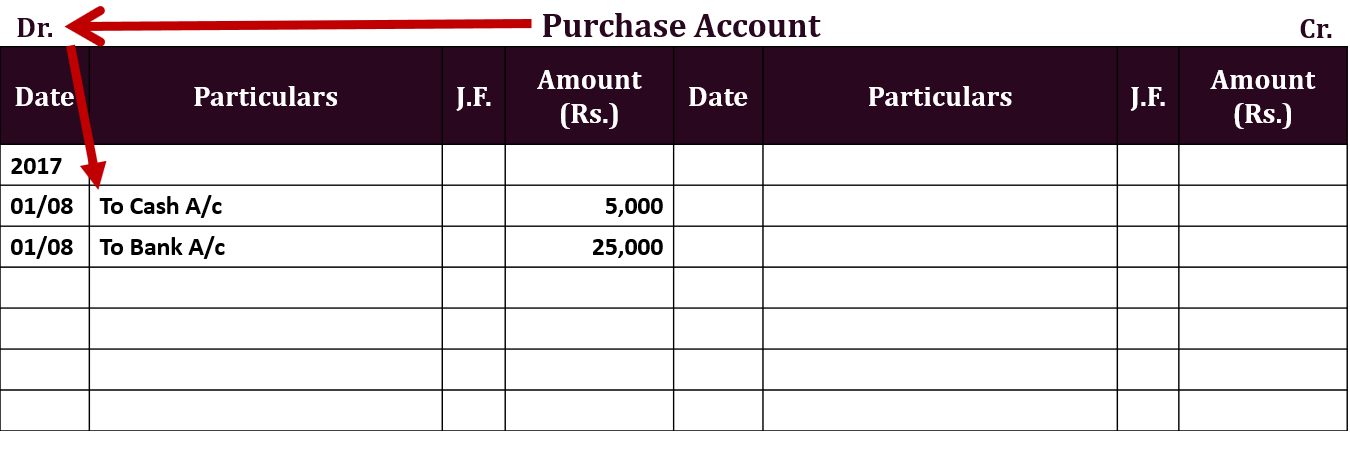

Example 2:

On Date 01/08/2017 Purchase goods from Mr Rohan worth Rs. 30,000/- and paid him Rs. 5,000/- in cash and 25,000/- By cheque.

In this above transaction three accounts are involved shown as below:

- Purchase A/c – Goods purchased.

- Cash A/c – Rs 5,000/- Cash paid for it.

- Bank A/c – Balance payment made with the cheque.

| Date | Particulars | L.F. | Debit | Credit | ||

| 01/08/2017 | Purchase a/c | Dr. | 30,000 | |||

| To Cash a/c | 5,000 | |||||

| To Bank a/c | 25,000 | |||||

| (Being Purchase goods from Mr Rohan worth Rs. 30,000/- and paid him Rs. 5,000/- in cash and 25,000/- By cheque) | ||||||

Post this transaction to the Ledger account as below:

Compound Journal Entry

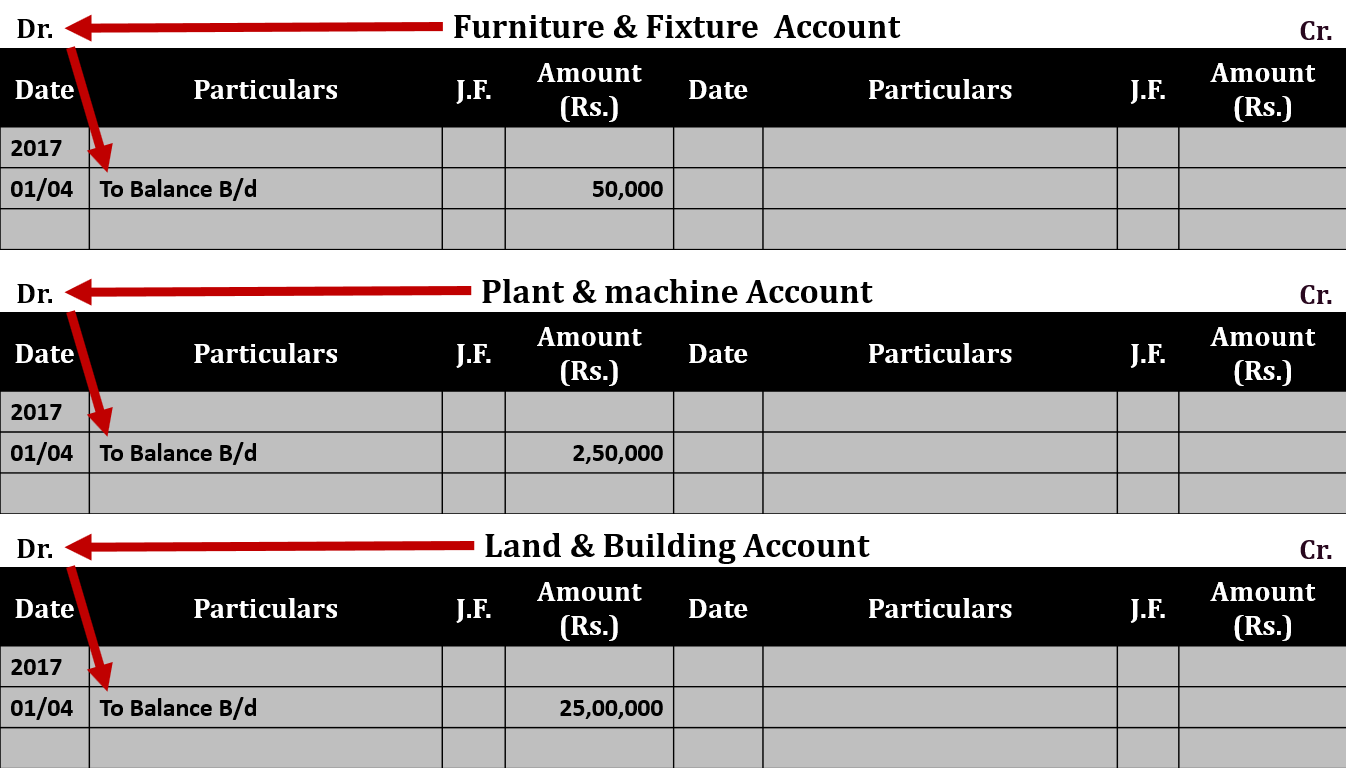

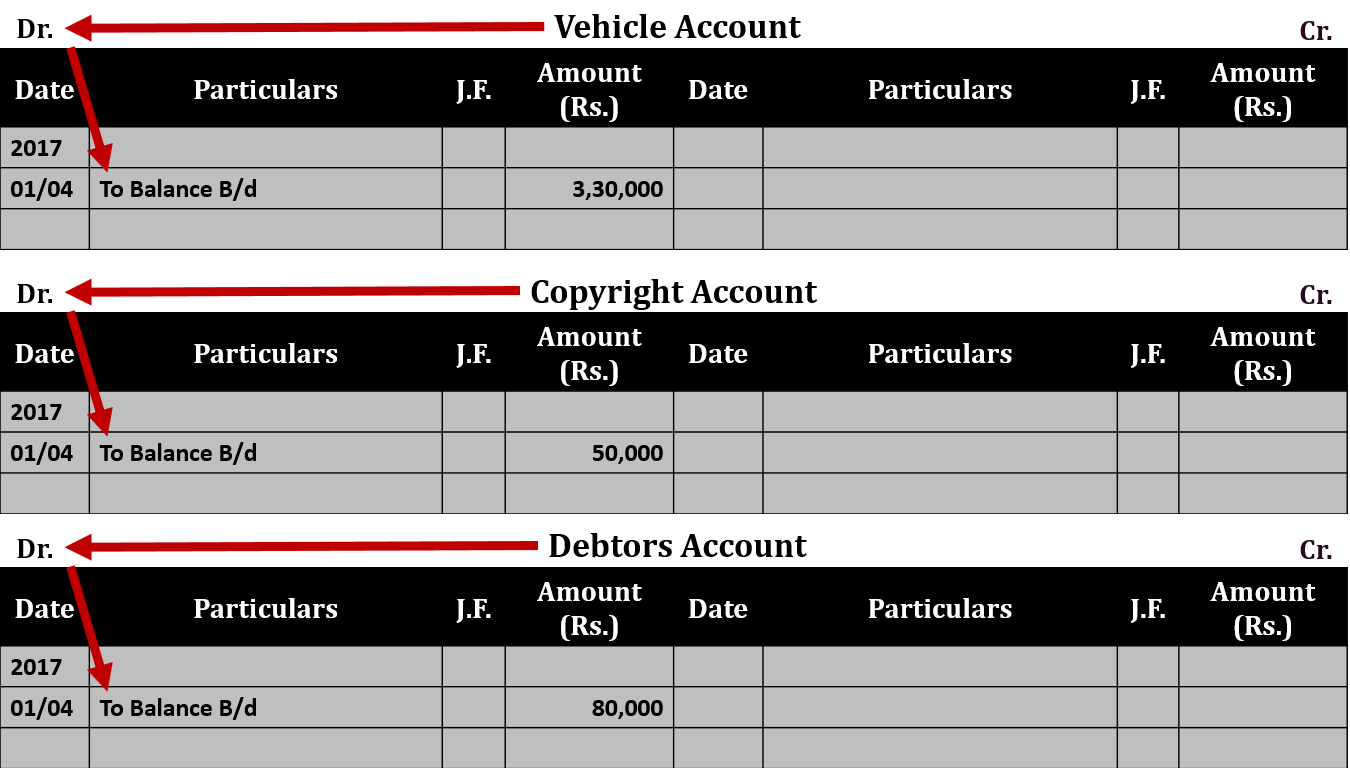

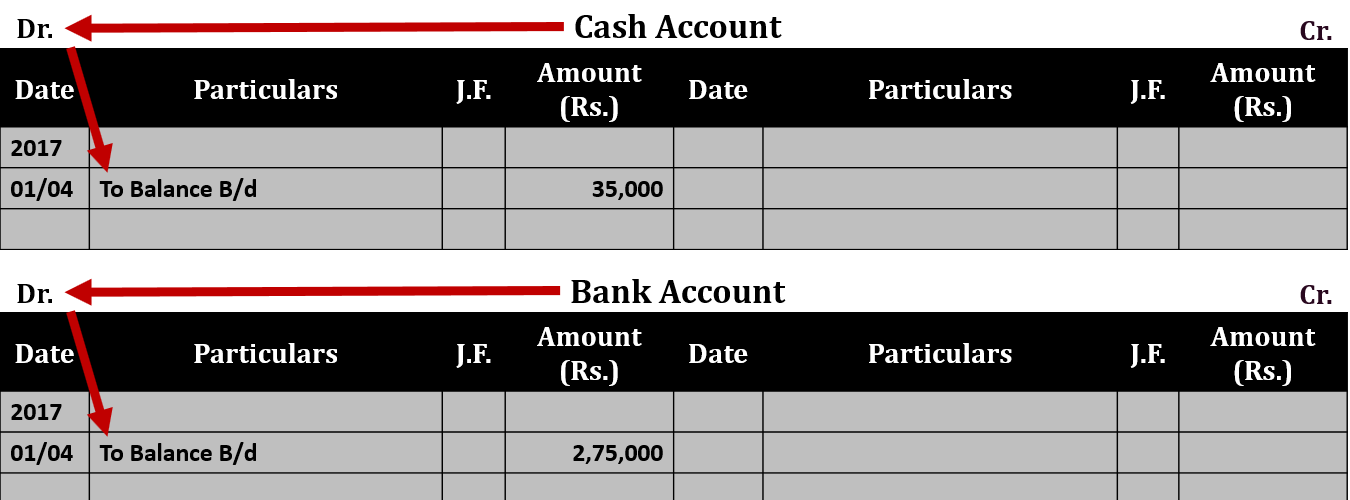

3. How to post an Opening journal entry.

we had already explained the meaning of opening a journal entry if you did not remember then please click here.

We will take the same example of the previous topic on the compound journal entry for easy understanding.

Example no. 1

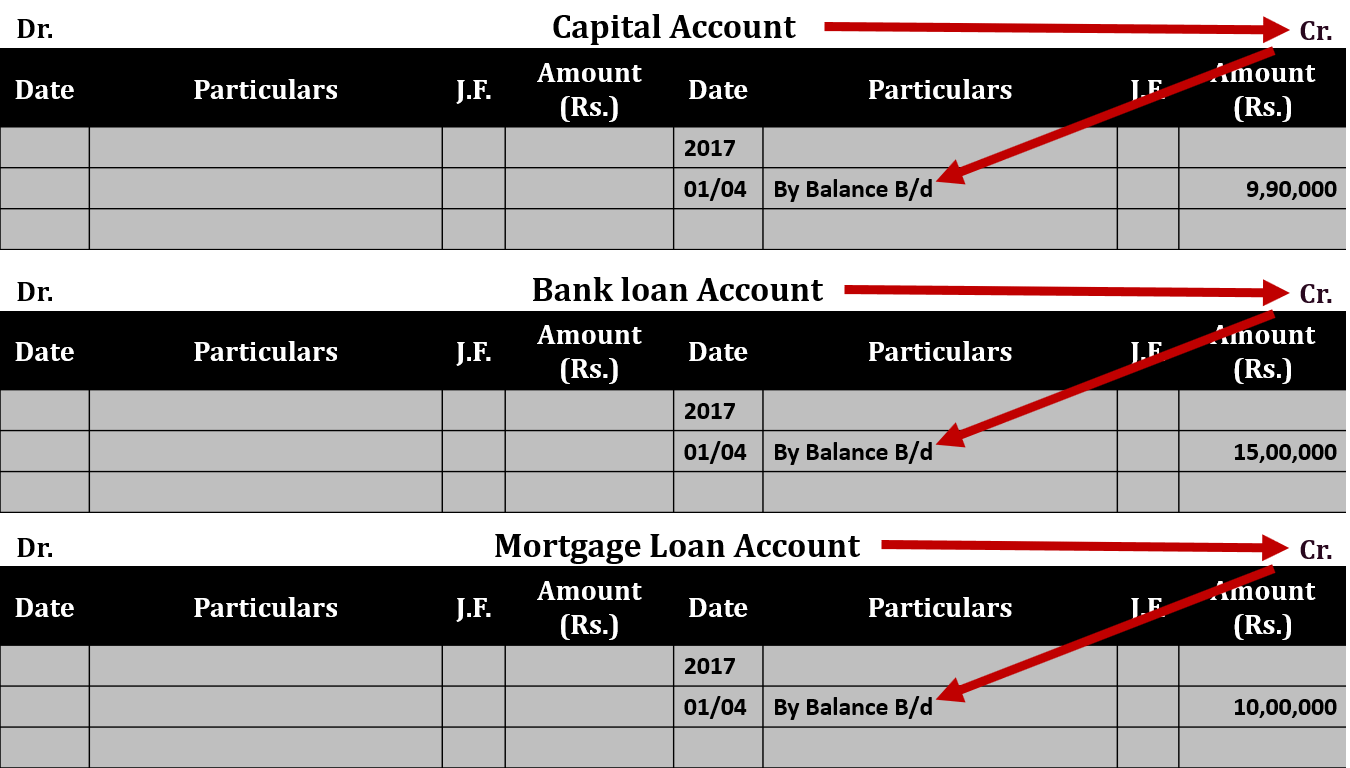

Balance sheet year ending 31/03/2017 shown the following balances post it to next financial year:

Closing Balances of Assets are

- Furniture & Fixture = 50,000/-

- Plant & machine = 2,50,000/-

- Land & Building = 25,00,000/-

- Vehicle = 3,30,000/-

- Copyright = 50,000

- Debtors = 80,000/-

- Cash = 35,000/-

- Bank = 2,75,000/-

Closing Balances of Capital and liabilities are

- Capital = 9,90,000/-

- Bank loan A/c = 15,00,000/-

- Mortgage Loan = 10,00,000/-

- Creditors = 80,000/-

Journal entry will be posted as shown below:

We have to open a total of 12 ledger accounts and Post this transaction to the Ledger account as below:

Thanks, Please share with your friends

Comment if you have any question

Check out Financial Accounting Books @ Amazon