Question 45 Chapter 5 of +2-Part-1

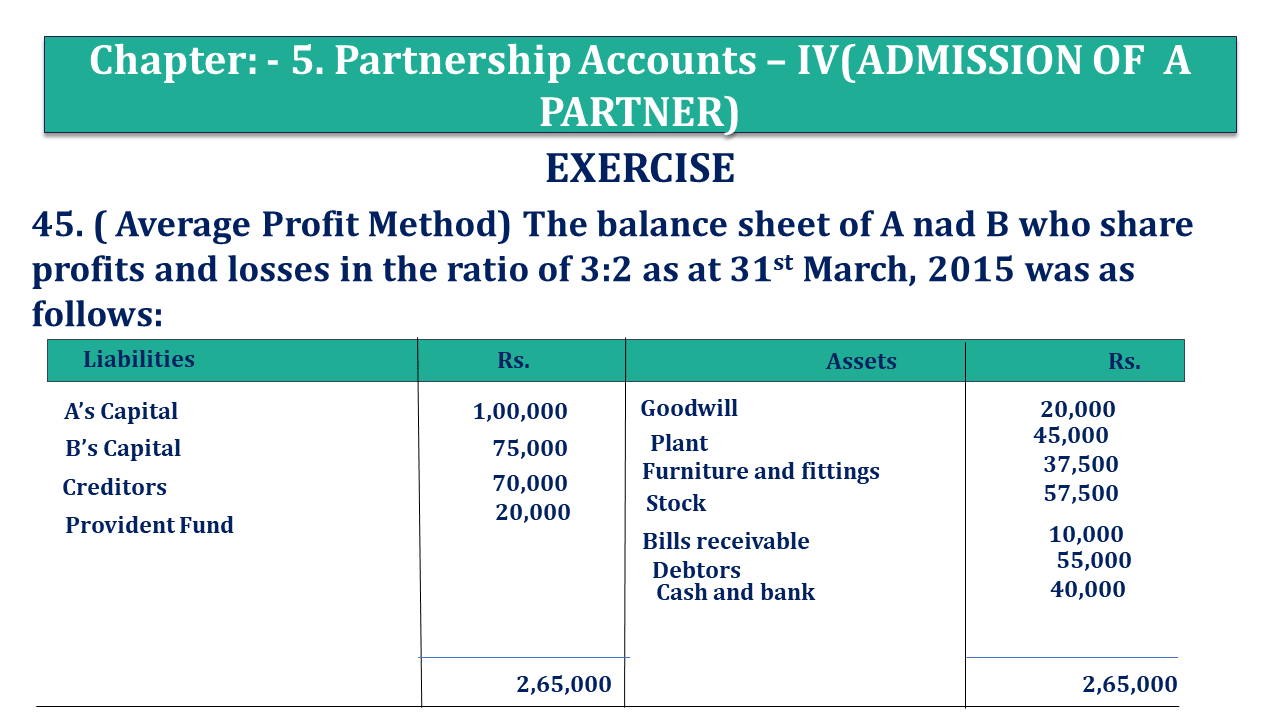

45. ( Average Profit Method) The balance sheet of A and B who share profits and losses in the ratio of 3:2 as at 31st March 2015 was as follows:

| Liabilities | Rs. | Assets | Rs |

| A’s Capital | 1,00,000 | Goodwill | 20,000 |

| B’s Capital | 75,000 | Plant | 45,000 |

| Creditors | 70,000 | Furniture and fittings | 37,500 |

| Provident Fund | 20,000 | Stock | 57,500 |

| Bills receivable | 10,000 | ||

| Debtors | 55,000 | ||

| Cash and bank | 40,000 | ||

| 2,65,000 | 2,65,000 |

C was admitted into the partnership on the following terms

(a) That the new profit sharing ratio shall be A 2/5th B 2/5th and C 1/5th

b) That C is to bring his capital of 50,000 in cash and to pay his share of Goodwill in the firm. Goodwill for this purpose is to be valued at 2 years purchase for an average of the previous 4 years profits. The profits for the previous 4 years are Rs. 25,000

Rs. 22,500 ;Rs. 25,000; Rs. 27,500.

(c) That the other assets are revalued as under-Plant Rs. 52,500 Furniture and fittings

Rs. 32.000: Stock Rs. 63,000 Debtors Rs. 50,000.

(d) That the value of assets except cash and bank shall remain unchanged

Give the necessary journal entries and the balance sheet of the reconstituted firm.

The solution of Question 45 Chapter 5 of +2 Part-1: –

| Journal | |||||

| Date | Particulars |

L.F. | Debit | Credit | |

| 1) | A’s Capital A/c | Dr. | 12,000 | ||

| B’s Capital A/c | Dr. | 8,000 | |||

| To Goodwill A/c | 20,000 | ||||

| (Being goodwill written off ) | |||||

| 2) | Bank A/c | Dr. | 60,000 | ||

| To C’s Capital A/c | 50,000 | ||||

| To Premium for Goodwill A/c | 10,000 | ||||

| (Being cash brought as capital and goodwill ) | |||||

| 3) | Premium for Goodwill A/c | Dr. | 10,000 | ||

| To A’s Capital A/c | 10,000 | ||||

| (Being goodwill transferred to A’s account ) | |||||

| 4) | Memorandum Revaluation A/c | Dr. | 10,500 | ||

| To Furniture and fittings | 5,500 | ||||

| To Debtors | 5,000 | ||||

| (Being assets revalued) | |||||

| 5) | Plant A/c | Dr. | 7,500 | ||

| Stock A/c | Dr. | 5,500 | |||

| To Memorandum Revaluation A/c | 13,000 | ||||

| (Being assets revalued) | |||||

| 6) | Memorandum Revaluation A/c | Dr. | 2,500 | ||

| To A’s Capital A/c | 1,500 | ||||

| To B’s Capital A/c | 1,000 | ||||

| (Being profit on revaluation distributed) | |||||

| 7) | Furniture and fittings | Dr. | 5,500 | ||

| Debtors | Dr. | 5,000 | |||

| To Memorandum Revaluation A/c | 10,500 | ||||

| (Being revaluation entry reversed) | |||||

| 8) | Memorandum Revaluation A/c | Dr. | 13,000 | ||

| To Plant A/c | . | 7,500 | |||

| To Stock A/c | 5,500 | ||||

| (Being revaluation entry reversed) | |||||

| 9) | A’s Capital A/c | Dr. | 1,000 | ||

| B’s Capital A/c | Dr. | 1,000 | |||

| C’s Capital A/c | Dr. | 500 | |||

| To Memorandum Revaluation A/c | 2,500 | ||||

| (Being memorandum loss distributed among all Partners in their new profit share ratio 2 : 2 : 1) | |||||

| Partners’ Capital Account |

|||||||

| Particulars | A | B | C | Particulars | A | B | C |

| To Goodwill A/c | 12,000 | 8,000 | By Balance b/d | 1,00,000 | 75,000 | ||

| To Memorandum Revaluation A/c |

1,000 | 1,000 | 500 | By Bank A/c | – | – | 50,000 |

| By Premium for Goodwill | 10,000 | – | – | ||||

| By Revaluation A/c | 1,500 | 1,000 | |||||

| To Balance c/d | 98,500 | 67,000 | 49,500 | ||||

| 1,11,500 | 76,000 | 60,000 | 1,11,500 | 76,000 | 60,000 | ||

| Balance Sheet |

|||||

| Liabilities |

Amount | Assets | Amount | ||

| A’s Capital | 98,500 | Plant | 45,000 | ||

| B’s Capital | 67,000 | Furniture and fittings | 37,500 | ||

| C’s Capital | 49,500 | 2,15,000 | Stock | 57,500 | |

| Creditors | 70,000 | Bills receivable | 10,000 | ||

| Provident Fund | 20,000 | Debtors | 55,000 | ||

| Cash and bank (Rs. 40,000+Rs. 60,000) |

1,00,000 | ||||

| 3,05,000 | 3,05,000 | ||||

Working Notes:

| Goodwill | = | Rs.(25,000+22,500+25,000+27,500) |

| 4 | ||

| = | Rs. 50,000 |

| C’s share of goodwill = | = | 1 | X | Rs 50,000 |

| 1 | ||||

| = | Rs 10,000 |

(ii) Sacrifice ratio:

| A’s sacrifice | = | 3 | – | 2 |

| 5 | 5 | |||

| = | 1 | |||

| 5 |

| B’s sacrifice | = | 2 | – | 2 |

| 5 | 5 | |||

| = | 0 | |||

| 5 |

Whole of sacrifice has been made by A

Thanks, Please Like and share with your friends

Comment if you have any questions.

Also, Check out the solved question of previous Chapters: –

Usha Publication – Accountancy PSEB (Class 12) – Volume I – Solution

- Chapter No. 1 – Accounting Not for Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Introduction)

- Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

- Chapter No. 4 – Partnership Accounts – III (Reconstitution of Partnership)

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

- Chapter No. 8 – Company Accounts (Share Capital)

- Chapter No. 9 – Company Accounts (Issue of Debentures)

- Chapter No. 10 – Company Accounts (Redemption of Debentures)

Usha Publication – Accountancy PSEB (Class 12) – Volume II – Solution

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis- Comparative and Common Size

- Chapter No. 4 – Ratio Analysis

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication