Focus Topic:6 Types of Adjusting Entries Explanation with Example

Estimated Reading Time:6 mins

Today we will cover the all entries which are not recorded in the books of accounts known as Adjusting Entries. Introduction to Adjusting Entries According to…

Syllabus-aligned study material with detailed definitions, formats, and practical examples.

Interactive check: Includes a custom practice quiz at the bottom of the article to self-evaluate knowledge.

Today we will cover the all entries which are not recorded in the books of accounts known as Adjusting Entries.

Introduction to Adjusting Entries

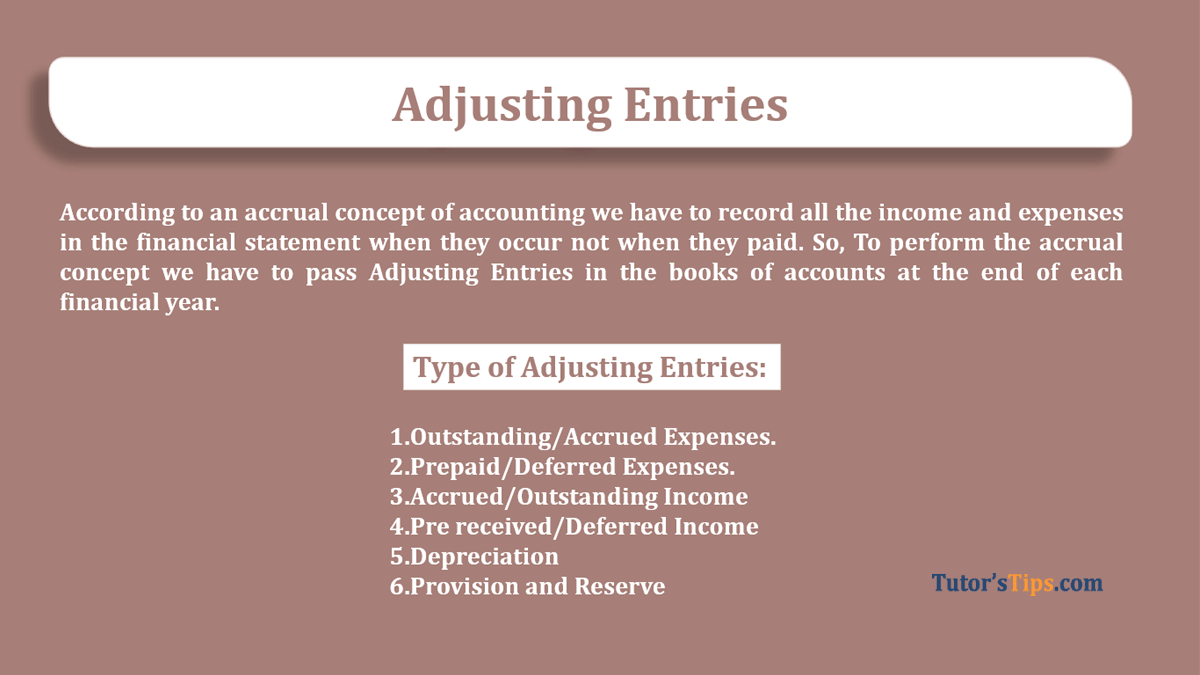

According to an accrual concept of accounting we have to record all the income and expenses in the financial statement when they occur not when they paid. So, To perform the accrual concept we have to pass Adjusting Entries in the books of accounts at the end of each financial year.

So with the help of Adjusting Entries, we can get an actual financial position of the company/firm/organization. It confirms the actual balance of all accounts eg. expenses, income, assets, and liabilities.

Type of Adjusting Entries:

The following are the type of Adjusting Entries: -

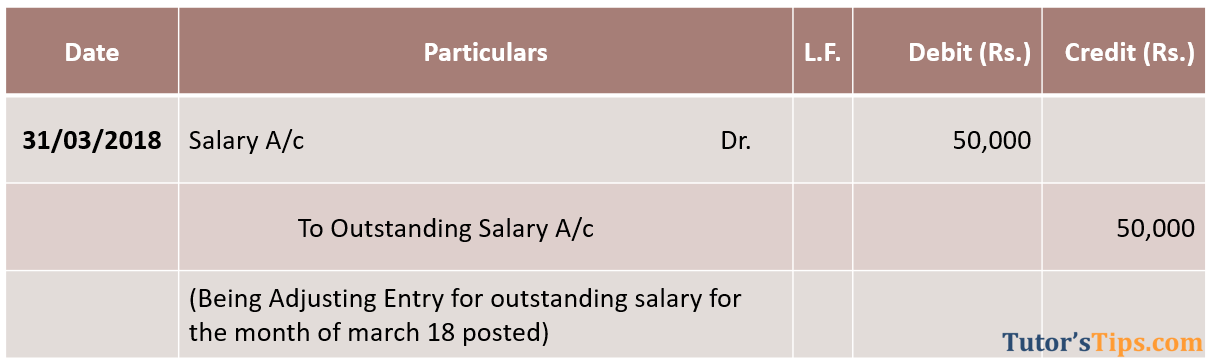

It means those expenses which were incurred but not yet paid.

For Example:

The salary Rs 50,000/- for the month of March-18 paid in April-18. Pass the journal entry for the year ended 31st March 2018.

Solution:

We have to pass journal entry at the end of the financial year means 31st March 2018 to record the correct amount of expenses.

Note: If you did notknowhow to apply this rules of accounting please check this link

https://tutorstips.com/golden-rules-of-accounting

In the Transaction, two accounts are involved salary and outstanding salary.

Salary -> Expense a/c -> Nominal rule ->Expense met by Business -> Debit Outstanding Salary -> Representative person -> Personal rule -> giver - > CreditAdjusting Entries - Outstanding Expenses

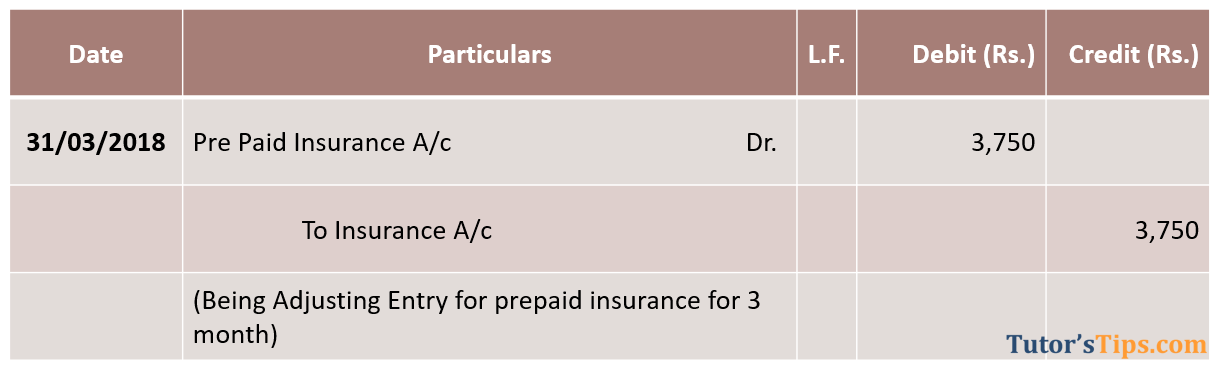

It means those expenses which were paid for but not yet incurred.

For Example:

Paid 15,000/-for the insurance of inventories taken up June-18. Pass the journal entry for the year ended 31st March 2018.

Solution:

So in this transaction, we have paid 3 months extra premium for insurance which is actually related to next year that why cannot claim this expense in this financial year. So, the treatment of this transaction are as following:

In the Transaction, two accounts are involved Insurance and Prepaid Insurance.

Insurance -> Expense a/c -> we had given extra Debit to this account so, now -> Credit it. Prepaid Insurance -> Representative person -> Personal rule -> Receiver - > Debit

Now Calculate the amount of prepaid insurance

15000* 3/12 = 3,750/-

Adjusting Entries - Prepaid Expenses

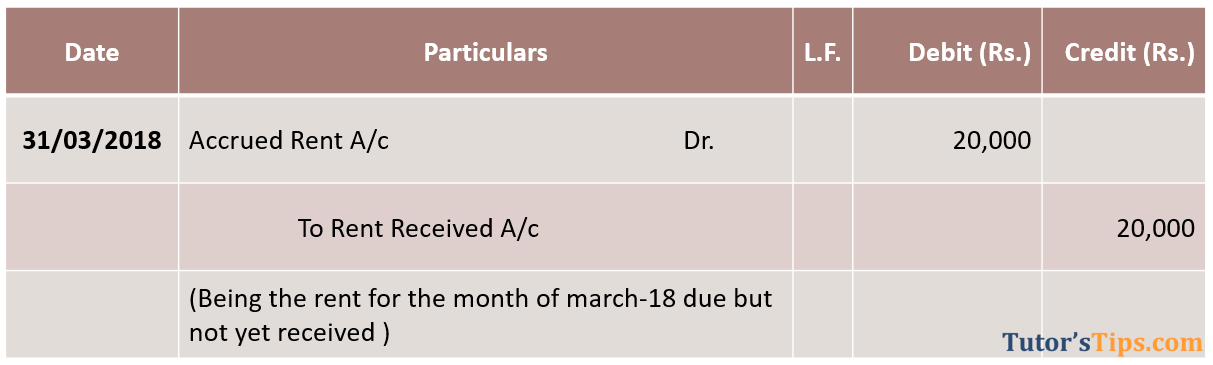

It means those incomes which were Incurred but not yet received.

Example:

The rent for the month of March-18 due but not received yet from the tenant for Rs 20,000/-.Pass the journal entry for the year ended 31st March 2018.

So in this transaction, we will treat two accounts with the golden rules of accounting shown as following.

Accrued Rent A/c -> Representative personal A/c -> Personal Rule -> Tenant using our cash for other propose. So, he is the receiver -> DebitRent received A/c -> Income A/c -> Nominal Rule -> Rent Earned -> CreditAdjusting Entries - Accrued Income

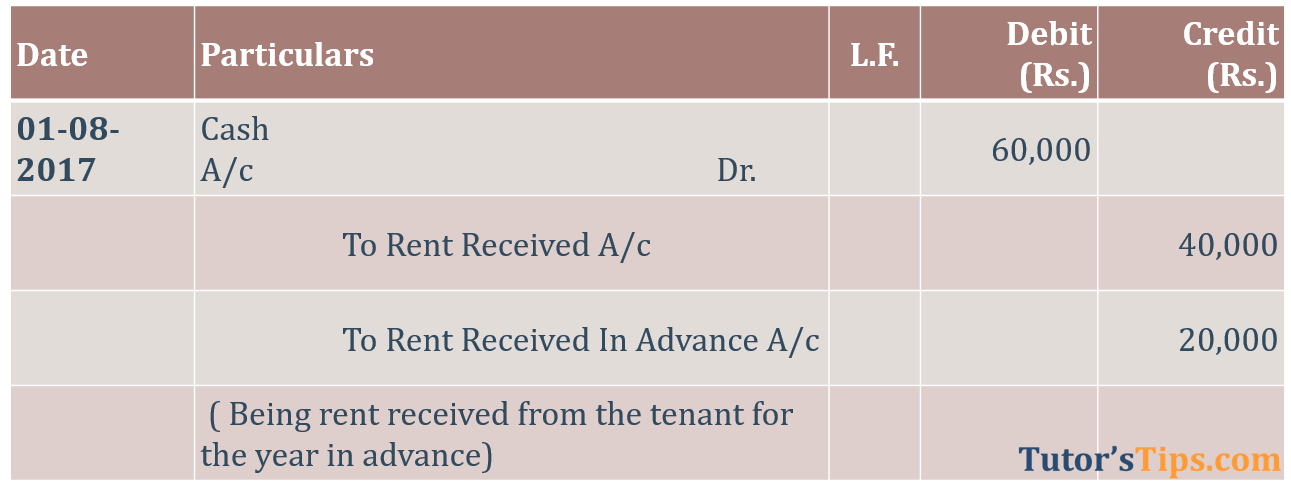

It means that income is received but not yet earned.

Example:

On 01/08/2017, rent received for the let-out building for the period of one year in advance. Pass the journal entry for the year ended 31st March 2018.

So in this transaction, we will treat three accounts with the golden rules of accounting shown as following.

Cash a/c -> Asset A/c -> Real Rule -> Cash Comes in -> DebitRent received A/c -> Income A/c -> Nominal Rule -> Rent Earned -> CreditAdvance Rent received A/c -> Representative personal A/c -> Personal Rule -> Tenant paying cash, giver -> CreditAdjusting Entries - Pre received Income

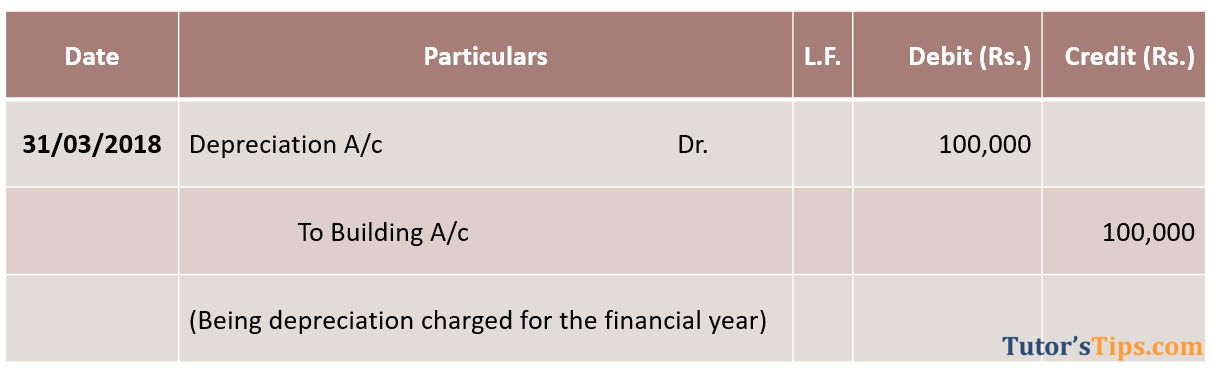

It means a decrease in the value of Fixed assets by passing time. It is charged only on fixed assets (except Land) because every fixed asset has a life more than one year but will not last indefinitely and the land has an indefinitely life so it will be appreciated.

Example:

Depreciation charged on building @ 10% on Rs 10,00,000/-. Pass the journal entry for the year ended 31st March 2018.

We will treat two account

Depreciation Account -> is Expenses -> Nominal Rule -> All Expenses -> DebitedBuilding Account -> is an Assets ->Real Rule -> Goes out -> CreditedAdjusting Entries - Depreciation

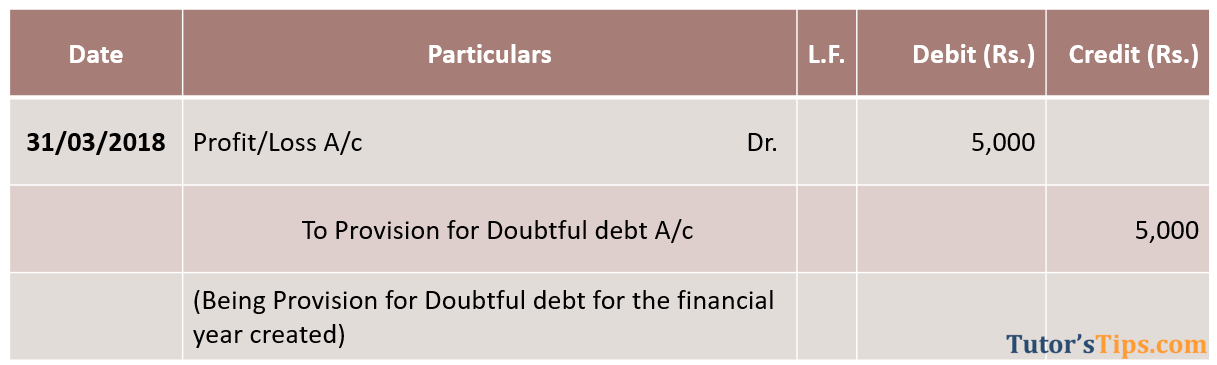

Provision and reserve mean to retain a part of the profit of the financial year to meet the liabilities in the future. the amount of which is not accurately finalized at the time of finalizing the financial statement.

Example:

Provision made for the Doubtful debt 5% on total debtors of 100,000/-. Pass the journal entry for the year ended 31st March 2018.

Solution:-

Amount of Provision is 100,000 * 5% = 5,000/-

There are two treatment of provision account shown as follows:-

We can show provision a/c in the liability side of the balance sheet

Deduct the amount of provision from the amount of an asset for which it was created.

1. We can show provision a/c in the liability side of the balance sheet:

In this treatment, we have to pass only single journal entry shown as follows:-

1. Provision for doubtful debt Account -> this account is representing the group of defaulter -> So it will be treated as Representative Person -> So Personal Rule applied -> we assume that we can not recover the due amount from them -> so now they giving us loss -> it means they are giver -> Credit2. Profit/loss Account ->is Income & expenses a/c -> Provision is made for future loss/expenses-> so Nominal Rule applied -> all losses and Expenses are debit -> Debit Adjusting Entries - Provision for doubtful debt

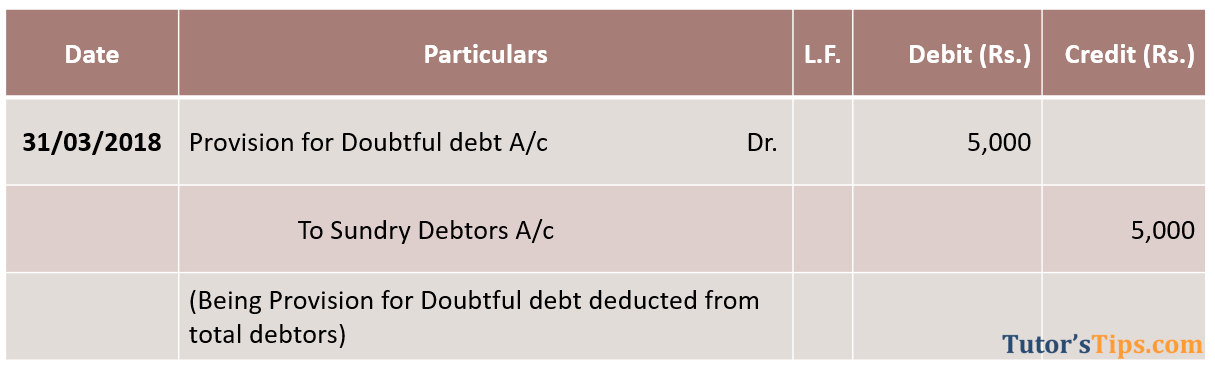

2. Deduct the amount of provision:-

Deduct the amount of provision from the amount of an asset for which it was created, We have to pass two journal entries shown as follows:-

The first journal entry is the same as explained in the above treatment.

In the Second Journal entry, We will transfer the amount of provision to an asset account for which it was created: -1. Provision for doubtful debt Account -> Closing the account of the provision by Debiting it -> Debit 2. Sundry Debtors Account -> Asset -> Real Rule -> Goes out -> CreditAdjusting Entries - Provision for doubtful debt transferred to Debtors

👤

Author & Educator

Sarbjit SinghB.Com and M.Com

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

❓ Frequently Asked Questions

What does "6 Types of Adjusting Entries Explanation with Example" cover?

Today we will cover the all entries which are not recorded in the books of accounts known as Adjusting Entries. Introduction to Adjusting Entries According to…

Who is this guide meant for?

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Financial Accounting.

Can I test myself on "6 Types of Adjusting Entries Explanation with Example"?

Yes — this page includes a short interactive quiz so you can check your understanding straight away.