Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Journal entry for Accrued income is very simple to remember. We will explain the meaning and journal entry for accrued income with the help of both rule of accounting i.e. golden rules and modern rules of accounting in this article as below:

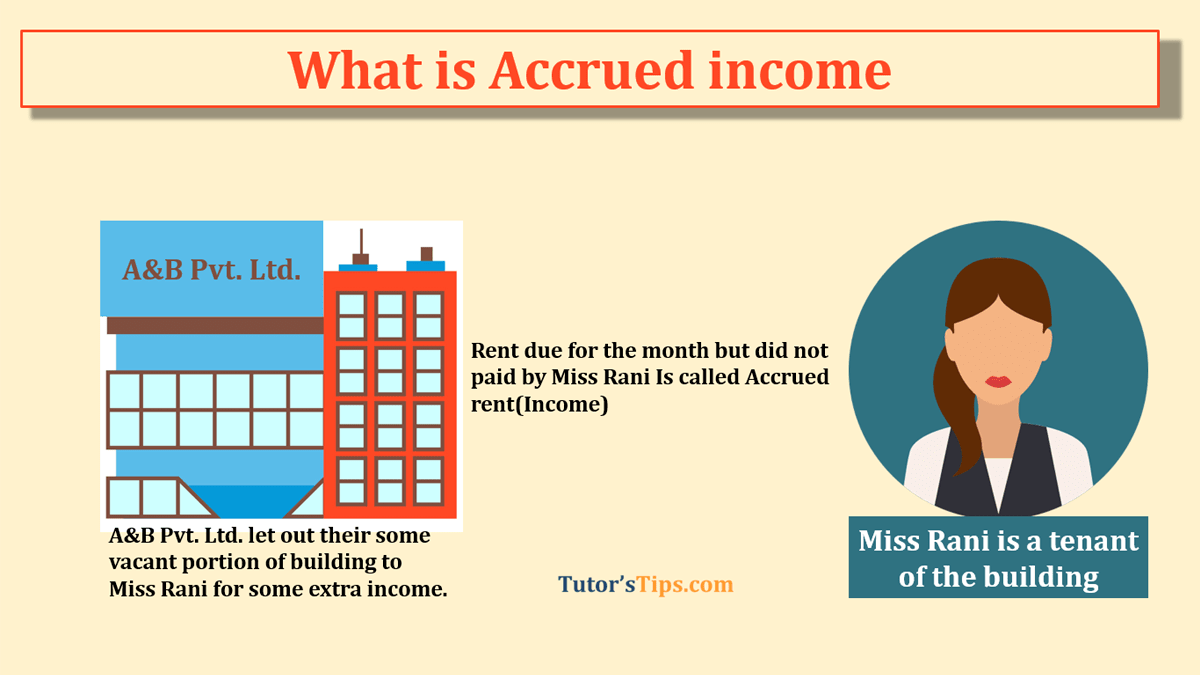

Accrued income means that income which is earned but yet not received by the Business enterprises. In other words, the income earned by the company by providing service to the other company or individual but payment for that service is still pending from the receiver of the services.

According to the accrual principle of the accounting, The Incomes and expenses are recorded in the books of that financial year in which year they have actually earned or due.

To find out the actual profit and loss of the business in a particular financial year we need to enter total expenses and incomes concerned with the same financial year. To calculate the total expenses and incomes we have to add the income which is due but not yet received during the year and expenses which are due but not yet paid during the year. So That's why accrual principle is accepted by almost all businesses and legal authorities of the country.

The journal entry for accrued income can be two types one is for creating the accused income account in the books of accounts and second is for settling the accrued income account in the books of accounts when payment received. These both are explained with the help of example shown as following:

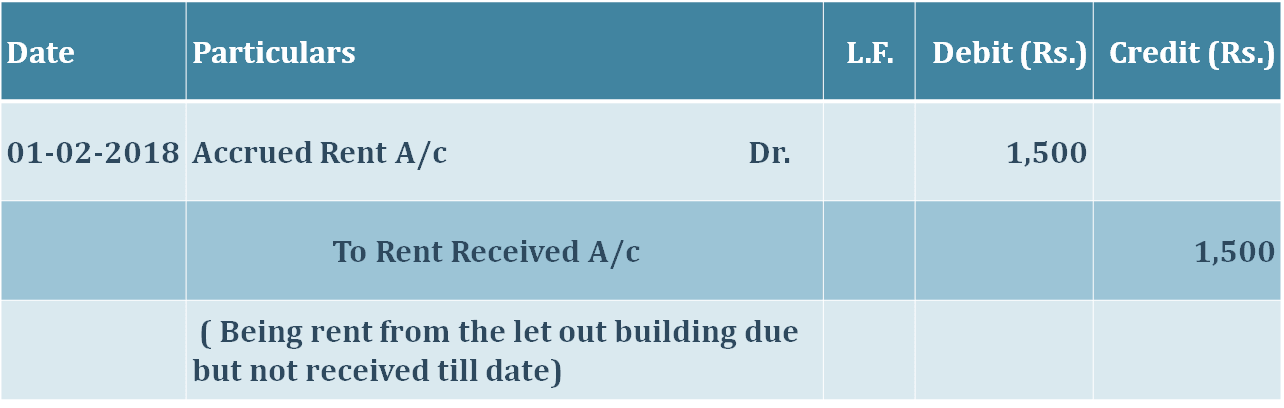

Example: 01/02/2018 Rent earn but not received yet from the tenant for Rs 1,500/-.

So in this transaction, According to the first step of our treatment of business transaction with the golden rules of accounting, we find two accounts which are involved in the transaction. These are shown as follows.

Accrued Rent A/c -> Representative personal A/c* -> Personal Rule -> Tenant using our cash for other propose. So, he is the receiver -> Debit

Rent received A/c -> Income A/c -> Nominal Rule -> Rent Earned -> Credit

The journal entry for the transaction is the following:

| Date | Particulars | L.F. | Debit | Credit |

|---|---|---|---|---|

| 01/02/18 | Accrued Rent a/c Dr. | 1,500 | ||

| To Rent Received a/c | 1,500 | |||

| (Being rent from the let out building due but not yet received) |

The journal entry is explained with the help of the following example:

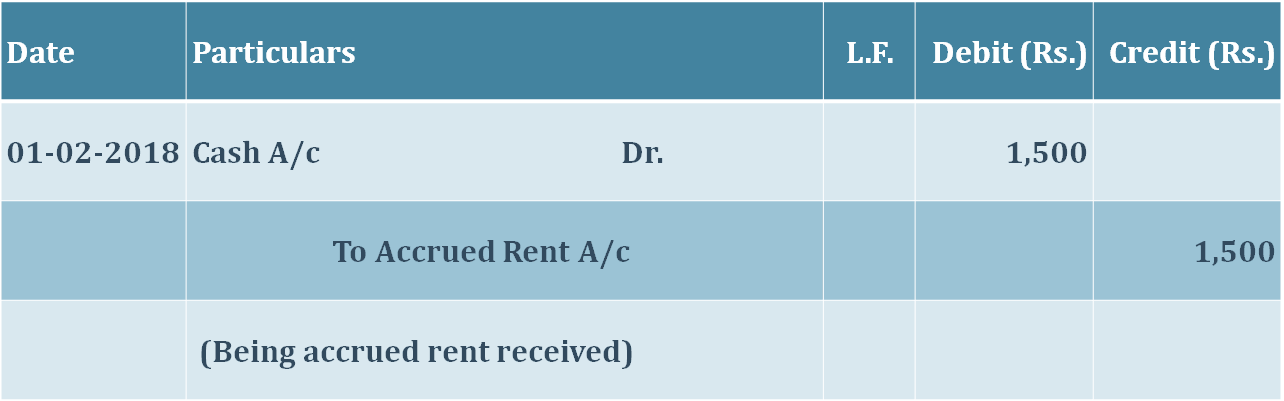

15/04/2018 Accrued Rent received from the tenant for Rs 1,500/-.

Accrued Rent A/c -> Representative personal A/c* -> Personal Rule -> Tenant is paying cash -> he is the giver -> Credit

Cash A/c -> Assets A/c -> Real Rule -> Cash received -> comes in -> Debit

The journal entry for the transaction is the following:

| Date | Particulars | L.F. | Debit | Credit |

|---|---|---|---|---|

| 15/04/18 | Cash a/c Dr. | 1,500 | ||

| To Accrued Rent a/c | 1,500 | |||

| (Being accrued rent received) |

Both the above journal entries are now explained with the help of modern rules of accounting as below:

The journal entry is explained with the help of the following example:

01/02/2018 Rent earn but not received yet from the tenant for Rs 1,500/-.

So Now we will treat this same transaction with the Modern rules of accounting shown as following.

Accrued Rent A/c -> Asset A/c -> Asset Rule -> Increase in asset -> Debit

Rent received A/c -> Income A/c -> Income Rule -> Increase in income -> Credit

The journal entry remains the same as above:

| Date | Particulars | L.F. | Debit | Credit |

|---|---|---|---|---|

| 01/02/18 | Accrued Rent a/c Dr. | 1,500 | ||

| To Rent Received a/c | 1,500 | |||

| (Being rent from the let out building due but not yet received) |

Example: 15/04/2018 Accrued Rent received from the tenant for Rs 1,500/-.

Accrued Rent A/c -> Asset A/c -> Asset Rule -> Accrued Rent received -> Decreased in asset -> Credit

Cash A/c ->Asset A/c -> Asset Rule -> Increase in asset -> Debit

The journal entry for the transaction is the following:

| Date | Particulars | L.F. | Debit | Credit |

|---|---|---|---|---|

| 01/02/18 | Cash a/c Dr. | 1,500 | ||

| To Accrued Rent a/c | 1,500 | |||

| (Being accrued rent received) |

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "What is Accrued income - Journal Entry and Examples", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to Financial Accounting.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "What is Accrued income - Journal Entry and Examples" instantly.