Annuity Method:

In Annuity method, we will calculate a fixed amount of depreciation on the original cost of an asset but also calculate interest on the invested amount of capital on the purchase of this asset with help of annuity table.

We will debit an asset account with the amount of interest earn at a fixed rate on the balance of an asset at the reduced value and charged fixed amount or rate of depreciation every year for the estimated life of an asset.

This method is suitable for those assets on which lager amount was invested and have a definite period of life.

Depreciation can be calculated under the Annuity method shown below:

Example:

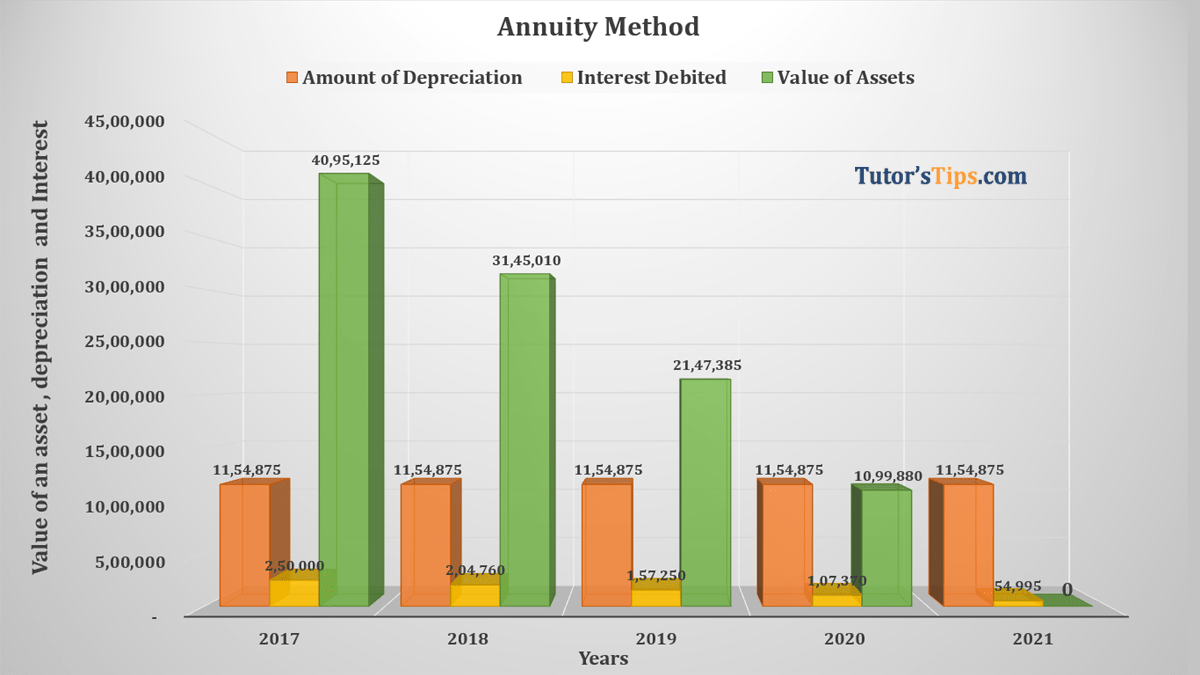

We purchased an asset on lease on 01/04/2016 for five years at a cost of Rs. 50,00,000/-. It is proposed to depreciate the lease by annuity method by charging loss of normal rate of interest @5%. With the help of annuity table, we get know the amount of depreciation to be charged by the following:

Re. 1 must write off a sum of Re. 0.230975 every year.

| Year ended | Opening balance of an asset | Interest Debited | Amount of depreciation | The closing balance of an asset |

| 31-03-2017 | 50,00,000 | 2,50,000 | 11,54,875 | 40,95,125 |

| 31-03-2018 | 40,95,125 | 2,04,760 | 11,54,875 | 31,45,010 |

| 31-03-2019 | 31,45,010 | 1,57,250 | 11,54,875 | 21,47,385 |

| 31-03-2020 | 21,47,385 | 1,07,370 | 11,54,875 | 10,99,880 |

| 31-03-2021 | 10,99,880 | 54,995 | 11,54,875 | 0 |

*Closing Balance = Opening Balance of an Asset + Interest Debited – Amount of Depreciation.

The journal entries under the Annuity Method: –

Now, we will post all the journal entries year by year according to the Annuity Method of Depreciation as follows: –

| Date | Particulars | L.F. | Debit | Credit | ||

| 1st Year | ||||||

| 2016-17 | ||||||

| 01-Apr | Lease A/c | Dr. | 50,00,000 | |||

| To Bank A/c | 50,00,000 | |||||

| (Being land purchased on lease ) | ||||||

| 31-Mar | Lease A/c | Dr. | 2,50,000 | |||

| To Interest A/c | 2,50,000 | |||||

| (Being Interest @ 5% charged on the closing balance of an asset) | ||||||

| 31-Mar | Depreciation A/c | Dr. | 11,54,875 | |||

| To Lease A/c | 11,54,875 | |||||

| (Being Depreciation on asset charged) | ||||||

| 31-Mar | Profit or loss A/c | Dr. | 11,54,875 | |||

| To Depreciation A/c | 11,54,875 | |||||

| (Being Depreciation transfer to P&L A/c) | ||||||

| 2nd Year | ||||||

| 2017-18 | ||||||

| 31-Mar | Lease A/c | Dr. | 2,04,760 | |||

| To Interest A/c | 2,04,760 | |||||

| (Being Interest @ 5% charged on the closing balance of an asset) | ||||||

| 31-Mar | Depreciation A/c | Dr. | 11,54,875 | |||

| To Lease A/c | 11,54,875 | |||||

| (Being Depreciation on asset charged) | ||||||

| 31-Mar | Profit or loss A/c | Dr. | 11,54,875 | |||

| To Depreciation A/c | 11,54,875 | |||||

| (Being Depreciation transfer to P&L A/c) | ||||||

| 3rd Year | ||||||

| 2017-18 | ||||||

| 31-Mar | Lease A/c | Dr. | 1,57,250 | |||

| To Interest A/c | 1,57,250 | |||||

| (Being Interest @ 5% charged on the closing balance of an asset) | ||||||

| 31-Mar | Depreciation A/c | Dr. | 11,54,875 | |||

| To Lease A/c | 11,54,875 | |||||

| (Being Depreciation on asset charged) | ||||||

| 31-Mar | Profit or loss A/c | Dr. | 11,54,875 | |||

| To Depreciation A/c | 11,54,875 | |||||

| (Being Depreciation transfer to P&L A/c) | ||||||

| 4th Year | ||||||

| 2017-18 | ||||||

| 31-Mar | Lease A/c | Dr. | 1,07,370 | |||

| To Interest A/c | 1,07,370 | |||||

| (Being Interest @ 5% charged on the closing balance of an asset) | ||||||

| 31-Mar | Depreciation A/c | Dr. | 11,54,875 | |||

| To Lease A/c | 11,54,875 | |||||

| (Being Depreciation on asset charged) | ||||||

| 31-Mar | Profit or loss A/c | Dr. | 11,54,875 | |||

| To Depreciation A/c | 11,54,875 | |||||

| (Being Depreciation transfer to P&L A/c) | ||||||

| 5th Year | ||||||

| 2017-18 | ||||||

| 31-Mar | Lease A/c | Dr. | 54,995 | |||

| To Interest A/c | 54,995 | |||||

| (Being Interest @ 5% charged on the closing balance of an asset) | ||||||

| 31-Mar | Depreciation A/c | Dr. | 11,54,875 | |||

| To Lease A/c | 11,54,875 | |||||

| (Being Depreciation on asset charged) | ||||||

| 31-Mar | Profit or loss A/c | Dr. | 11,54,875 | |||

| To Depreciation A/c | 11,54,875 | |||||

| (Being Depreciation transfer to P&L A/c) | ||||||

The Assets account under the Annuity Method: –

Now, we will prepare an asset account under the Annuity Method of Depreciation shown below:

| Lease Account | |||||

| Date | Particulars | Amount | Date | Particulars | Amount |

| 01-04-2017 | To Bank A/c | 50,00,000 | 31-03-2018 | By Depreciation A/c | 11,54,875 |

| 31-03-2018 | To Interest A/c | 2,50,000 | 31-03-2018 | By Balance C/d | 40,95,125 |

| 52,50,000 | 52,50,000 | ||||

| 01-04-2018 | To Balance B/d | 40,95,125 | 31-03-2019 | By Depreciation A/c | 11,54,875 |

| 31-03-2019 | To Interest A/c | 2,04,760 | 31-03-2019 | By Balance C/d | 31,45,010 |

| 42,99,885 | 42,99,885 | ||||

| 01-04-2019 | To Balance B/d | 31,45,010 | 31-03-2020 | By Depreciation A/c | 11,54,875 |

| 31-03-2020 | To Interest A/c | 1,57,250 | 31-03-2020 | By Balance C/d | 21,47,385 |

| 33,02,260 | 33,02,260 | ||||

| 01-04-2020 | To Balance B/d | 21,47,385 | 31-03-2021 | By Depreciation A/c | 11,54,875 |

| 31-03-2021 | To Interest A/c | 1,07,370 | 31-03-2021 | By Balance C/d | 10,99,880 |

| 22,54,755 | 22,54,755 | ||||

| 01-04-2021 | To Balance B/d | 10,99,880 | 31-03-2022 | By Depreciation A/c | 11,54,875 |

| 31-03-2022 | To Interest A/c | 54,995 | 31-03-2022 | By Balance C/d | 0 |

| 11,54,875 | 11,54,875 | ||||