Question No 72 Chapter 1 – UNIMAX Class 12 Part 2 – 2021

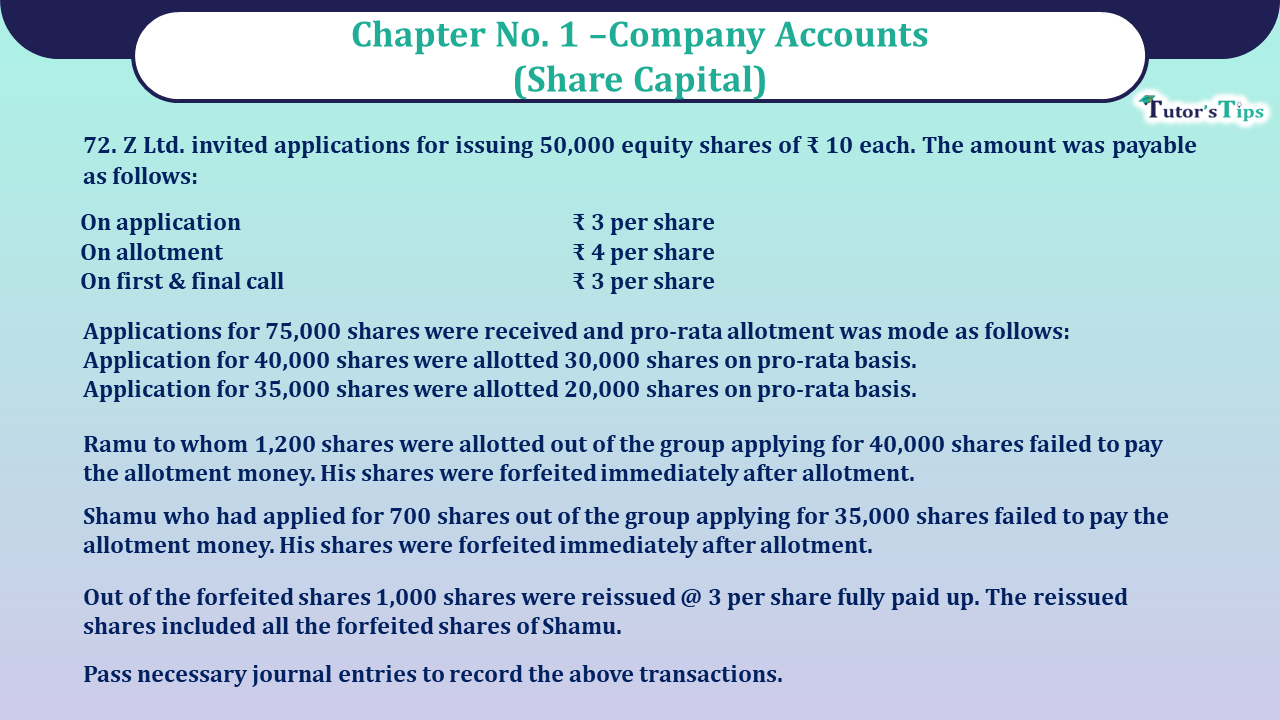

Z Ltd. invited applications for issuing 50,000 equity shares of ₹ 10 each. The amount was payable as follows:

| On application | ₹ 3 per share |

| On allotment | ₹ 4 per share |

| On first & final call | ₹ 3 per share |

Applications for 75,000 shares were received and pro-rata allotment was mode as follows:

Application for 40,000 shares were allotted 30,000 shares on pro-rata basis.

Application for 35,000 shares were allotted 20,000 shares on pro-rata basis.

Ramu to whom 1,200 shares were allotted out of the group applying for 40,000 shares failed to pay the allotment money. His shares were forfeited immediately after allotment.

Shamu who had applied for 700 shares out of the group applying for 35,000 shares failed to pay the allotment money. His shares were forfeited immediately after allotment.

Out of the forfeited shares 1,000 shares were reissued @ 3 per share fully paid up. The reissued shares included all the forfeited shares of Shamu.

Pass necessary journal entries to record the above transactions.

The solution of Question 72 Chapter 1 of +2 Part-2: –

Journal

| Date | Particulars |

L.F. | Debit | Credit | |

| Bank A/c | Dr. | 2,25,000 | |||

| To Equity share application A/c | 2,25,000 | ||||

| (Being application money received on 75,000 shares @ ₹ 3 each) | |||||

| Equity share application A/c | Dr. | 2,25,000 | |||

| To Equity share capital A/c | 1,50,000 | ||||

| To Equity share allotment A/c | 75,000 | ||||

| (Being application money transferred to share capital A/c & share allotment) | |||||

| Equity shares allotment A/c | Dr. | 2,00,000 | |||

| To Equity shares capital A/c | 2,00,000 | ||||

| (Being allotment money due on 50,000 shares @ 4 per share) | |||||

| Bank A/c | Dr. | 1,20,700 | |||

| To Equity shares allotment A/c | 1,20,700 | ||||

| (Being allotment money received except on 1600 shares) | |||||

| Ramu | Equity share capital A/c | Dr. | 8400 | ||

| To Equity share allotment A/c | 3600 | ||||

| To Share forfeited A/c | 4800 | ||||

| (Being 1200 shares forfeited due to non-payment of allotment) | |||||

| Shamu | Equity share capital A/c | Dr. | 2800 | ||

| To Equity shares allotment A/c | 700 | ||||

| To Share forfeited A/c | 2100 | ||||

| (Being 400 shares forfeited due to non-payment of allotment money) | |||||

| Bank A/c | Dr. | 9,000 | |||

| Share forfeited A/c | Dr. | 1,000 | |||

| To Equity share capital A/c | 10,000 | ||||

| (Being 1000 share forfeited reissued @ ₹ 9 per share fully paid up) | |||||

| Share forfeited A/c | Dr. | 3500 | |||

| To capital reserve A/c | 3500 | ||||

| (Being the profit on 1000 forfeited shares transferred to capital reserve A/c) | |||||

Working Note:

| Shares applied | Shares allotted | |

| Lot 1 | 40,000 | 30,000 |

| 35,000 | 20,000 | |

| 75,000 | 50,000 |

1 Table showing adjustment of excess amount received on application.

| Lot 1 | Lot 2 | total | |

| No. of shares applied | 40,000 | 35,000 | 75,000 |

| Less: no. of shares allotted | 30,000 | 20,000 | 50,000 |

| Over subscription | 10,000 | 15,000 | 25,000 |

| ₹ | ₹ | ₹ | |

| Excess amount received on application @ ₹ 3 | 30,000 | 45,000 | 75,000 |

| Less: amount adjusted on allotment @ ₹ 4 | 30,000 | 45,000 | 75,000 |

| Refunded to be made | Nil | Nil | Nil |

2 Net Amount received on allotment

| No. of share allotted to Ramu = 1200 share | |

| No. of shares applied by Ramu = 1200 x 40,000/30,000 | 1600 share |

| ₹ | |

| Application money received on (1600 shares of Mr. Ramu 1600*3) | 4800 |

| Less: actual application amount on 1200 shares (1200*3) | 3600 |

| Excess application money adjusted towards allotment | 1200 |

| ₹ | |

| Allotment amount due Mr. Ramu on 1200 shares = 1200 x 4 | 4800 |

| Less: Excess application money adjusted | 1200 |

| 3600 | |

| No. of shares applied by Mr. Shamu | 700share |

| No of shares allotted to Mr. Shamu = 700 x 20,000/35,000 | 400share |

| ₹ | |

| Application money received on 700 shares of Mr. Shamu (700 x 3) | 2100 |

| Less: actual application amount on 400 shares (400 x 3) | 1200 |

| Amount not paid by Mr. Ramu | 3600 |

| No. of shares applied by Mr. Shamu | 700share |

| No. of shares allotted to Mr. Shamu = 700 x 20,000/35,000 | 400share |

| ₹ | |

| Application money received on700 shares of Mr. Shamu (700 x 3) | 2100 |

| Less: Actual application amount on 400 shares (400 x 3) | 1200 |

| Excess application money adjusted towards allotment | 900 |

| ₹ | |

| Allotment amount due from Mr. Shamu on 400 shares = (44 x 4) | 1600 |

| Less: Excess application money adjusted | 900 |

| Amount not paid by Mr. Shamu | 700 |

| ₹ | |

| Total amount due on allotment = (50000 x 4) | 2,00,000 |

| Less: application money already adjusted | 75000 |

| 1,25,000 | |

| Less: amount not paid by Mr. Shamu | 3600 |

| 1,21,400 | |

| Less: amount not paid by Mr. Shamu | 700 |

| Net amount received on allotment | 1,20,700 |

4 Calculation of amount to be transferred to Capital Reserve

| Amount forfeited on 1200 shares of Mr. Ramu = ₹ 4800 | |

| Amount forfeited on 600 shares of Mr. Ramu =4800 x 600/1200 = 2400 | |

| Amount forfeited on 400 shares of Mr. Shamu = ₹ 2100 | |

| Amount forfeited on 600 shares of Mr. Shamu = ₹ 2400 | |

| Total amount of forfeited on 1000 shares = 4500 | |

| Less discount allowed on reissued shares = 4500 | |

| Balance credited to capital reserve a/c = 3500 |

Thanks, Please Like and share with your friends

Comment if you have any Doubts.

Share Capital: Meaning, Types, and Classes

Usha Publication – Accountancy PSEB (Class 12) – Volume I – Solution

- Chapter No. 1 – Accounting Not for Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Introduction)

- Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

- Chapter No. 4 – Partnership Accounts – III (Reconstitution of Partnership)

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

- Chapter No. 8 – Company Accounts (Share Capital)

- Chapter No. 9 – Company Accounts (Issue of Debentures)

- Chapter No. 10 – Company Accounts (Redemption of Debentures)

Usha Publication – Accountancy PSEB (Class 12) – Volume II – Solution

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis- Comparative and Common Size

- Chapter No. 4 – Ratio Analysis

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication