Question No 41 Chapter No 18

Goods withdrawn for business and personal use

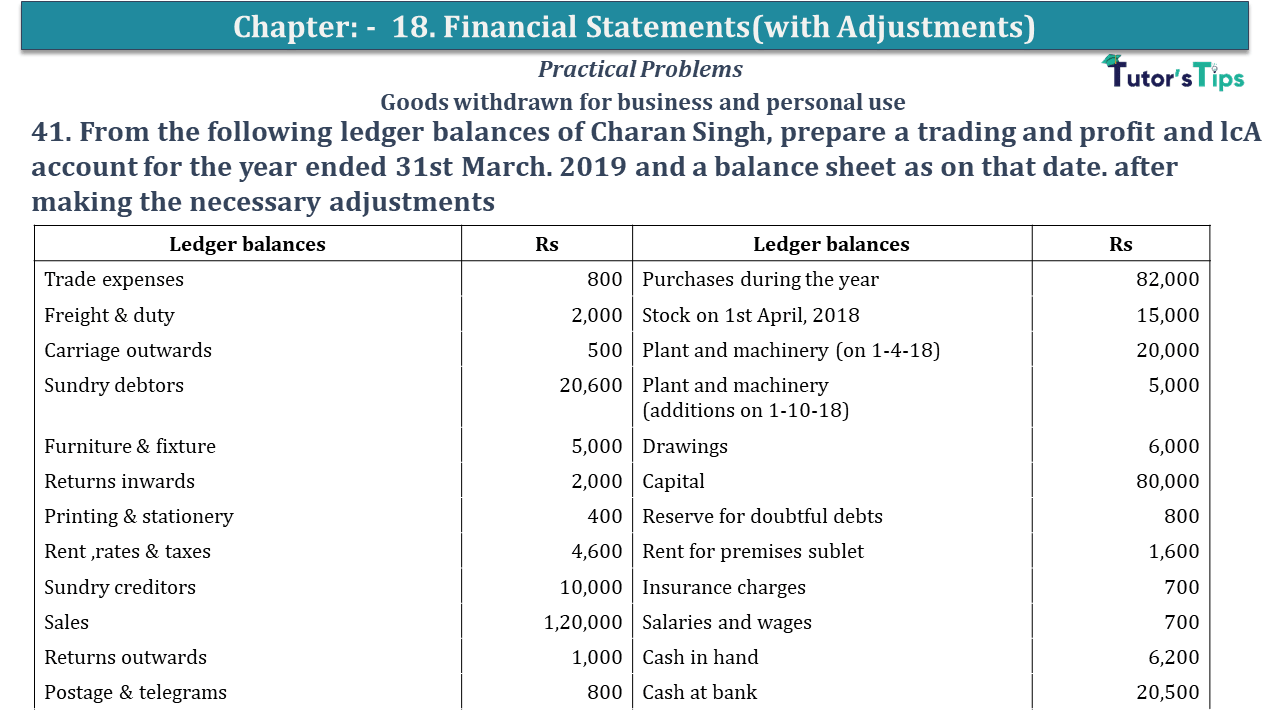

41. From the following ledger balances of Charan Singh, prepare a trading and profit and lcA account for the year ended 31st March. 2019 and a balance sheet as on that date. after making the necessary adjustments

| Ledger balances | Rs | Ledger balances | Rs |

| Trade expenses | 800 | Purchases during the year | 82,000 |

| Freight & duty | 2,000 | Stock on 1st April 2018 | 15,000 |

| Carriage outwards | 500 | Plant and machinery (on 1-4-18) | 20,000 |

| Sundry debtors | 20,600 | Plant and machinery | 5,000 |

| (additions on 1-10-18) | |||

| Furniture & fixture | 5,000 | Drawings | 6,000 |

| Returns inwards | 2,000 | Capital | 80,000 |

| Printing & stationery | 400 | Reserve for doubtful debts | 800 |

| Rent ,rates & taxes | 4,600 | Rent for premises sublet | 1,600 |

| Sundry creditors | 10,000 | Insurance charges | 700 |

| Sales | 1,20,000 | Salaries and wages | 700 |

| Returns outwards | 1,000 | Cash in hand | 6,200 |

| Postage & telegrams | 800 | Cash at bank | 20,500 |

The items for adjustments are :

(i)Stock on 31st March 2019 was 14,000.

(ii) Write off 600 as bad debts.

(iii) The provision for doubtful debts is to, be maintained at 5% of sundry debtors.

(iv) Provide for depreciation-furniture and fixtures at 5% p.a. and on plant & machinery at 20% p.a.

(v) Insurance prepaid was 100.

(vi) A fire occurred on 5th March 2019 in the godown and stock of the value of 5,000 was destroyed. It was insured and the insurance company admitted full claim.

(vii) Manager is given a 10% commission on net profit finally remaining.

The solution of Question No 41 Chapter No 18:-

| Trading A/c |

|||||

| Particular |

Amount | Particular |

Amount | ||

| To Opening Stock A/c | 15,000 | By Sale A/c | 1,20,000 | ||

| To Purchases A/c | 82,000 | Less: return | 2,000 | 1,18,000 | |

| Less: return | 1,000 | 81,000 | |||

| To fright & duty A/c | 2,000 | By Closing Stock A/c | 14,000 | ||

| To Gross Profit A/c | 39,000 | ||||

| 1,37,000 | 1,37,000 | ||||

| Profit/Loss A/c |

|||||

| Particular |

Amount | Particular |

Amount | ||

| To Trade expenses | 800 | By Gross Profit A/c | 39,000 | ||

| To carriage outwards | 500 | By Rent A/c | 1,600 | ||

| To printing & stationery | 400 | ||||

| To Rent ,rates & taxes | 4,600 | ||||

| To Bad debts w/off during the year | 600 | ||||

| Add: new provision | 1,000 | ||||

| Less: old provision | 800 | 800 | |||

| To postage & telegrams | 800 | ||||

| To salesmen wages | 21,300 | ||||

| To dep. On furniture & fitting | 250 | ||||

| To dep. On plant & machinery | 4,500 | ||||

| To insurance paid. | 700 | ||||

| Less: unexpired | 100 | 600 | |||

| To manager’s commission | 550 | ||||

| To Net profit A/c | 5,500 | ||||

| 40,600 | 40,600 | ||||

| Balance Sheet | |||||

| Labilities |

Amount | Assets |

Amount | ||

| Capital A/c | 80,000 | Debtors | 20,600 | ||

| Add: Net Profit | 5,500 | Less: bad debts | 600 | ||

| Less: Drawing | 6,000 | 79,500 | Less: provision | 1,000 | 19,000 |

| Creditor | 10,000 | Cash in hand | 6,200 | ||

| Manager commission due | 550 | Cash at bank | 20,500 | ||

| Closing stock | 14,000 | ||||

| Furniture & fitting | 5,000 | ||||

| Less: depreciation | 250 | 4,750 | |||

| Machinery | 25,000 | ||||

| Less: depreciation | 4,500 | 20,500 | |||

| Insurance claim | 5,000 | ||||

| Unexpired insurance | 100 | ||||

| 90,050 | 90,050 | ||||

Final Accounts: Meaning, Definition and Explanation

Profit and Loss Account: Meaning, Format & Examples

Balance Sheet: Meaning, Format & Examples

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of all Chapters: –

Usha Publication – Elements of Book-Keeping PSEB (Class 11) – Solution

Chapter No. 2 – Theory Base of Accounting

Chapter No. 3 – Origin of Transactions

Chapter No. 4 – Vouchers and transactions

Chapter No. 6 – Accounting for Goods and Services Tax(GST)

Chapter No. 9 – Other Subsidiary Books

Chapter No. 10 – Journal Proper

Chapter No. 11 – Trial Balance

Chapter No. 12 – Bank Reconciliation Statement

Chapter No. 14 – Provisions and Reserves

Chapter No. 15 – Bills of Exchange

Chapter No. 16 – Rectification of Errors

Chapter No. 17 – Financial Statements – (Without Adjustments)