Today we are covering the technical and theoretical topic of the Reserve. So please read it very consciously and in this article, you will learn the meaning of the Reserve, types of Reserve, accounting treatment of Reserve and we will make it an understandable topic in much better ways with the help of examples.

What is Reserve:-

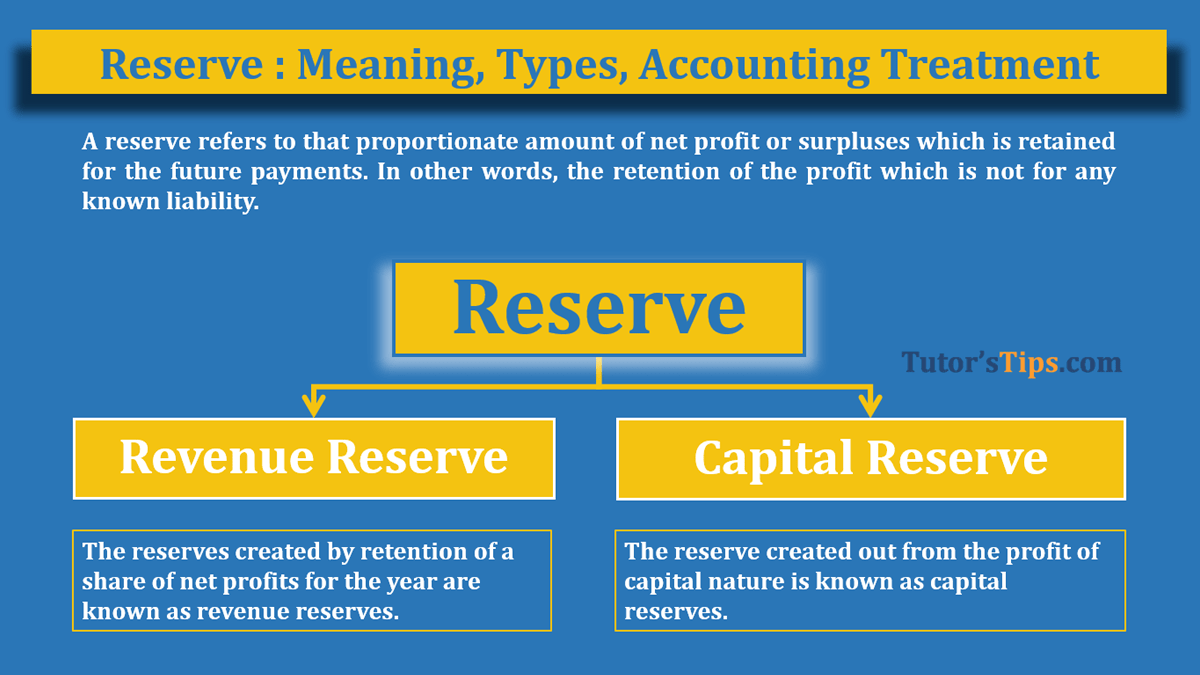

A reserve refers to the proportionate amount of net profit or surpluses which is retained for future payments. In other words, the retention of the profit is not for any known liability.

According to William Pickles. “Reserve means the amount set aside out of profit and other surpluses, which are not earmarked in any way to meet any particular liability known to exist on the date of Balance Sheet.”

“According To Part III, Schedule VI of the Companies Act, 1956,

The expression ‘reserves’ shall not include any amount written off or retained by way of providing for depreciation, renewals or diminution in value of assets or retained by way of providing for known liability. However, if the amount of provision is in excess of the amount which in the opinion of the directors is reasonably necessary for the purpose, the excess shall be treated as a reserve and not as a provision.”

Types of Reserves:-

1. Revenue(R/R): –

The reserves created by the retention of a share of net profits for the year are called revenue reserves. The creation of reserves by retention of profits is simply an appropriation of net profits. It does not affect the amount of net profit to pay the tax liability but it reduces the share of profit available for distribution among the shareholder, partners, or Owner. Revenue Reserve is also known as “Retained Earnings”, “Undistributed Profits” or “Retained Profits”.

To create “Revenue Reserves” we have to make an account named “Appropriation Profit/Loss account” after making of profit/loss account (income statement). The example of the Appropriation Profit/Loss account is shown below.

The feature of R/R:-

- These are created to strengthen the financial position of the business

- It does not affect the net profit for the year.

- it is the part of the owner’s capital.

- It can make for general purposes also if the purpose of retention of profit is not specified yet.

- it makes available additional working capital.

2. Capital (C/R): –

The reserve created out from the profit of capital nature is known as capital reserves. These reserves are not free for distribution among the Owner of the business by way of dividend. Generally, These profits are not available for distribution. The following are some names of Capital profit or gain.

- Profit on the sale of Fixed Assets.

- Premium charged on issued of debenture or equity share capital.

- Prior Period profit of the business or Profit before incorporation.

- Increase in value of fixed assets by the revaluation.

- Profit on the reissue of forfeited shares.

- Capital Redemption Reserve.

- Gain on the redemption of the debenture.

C/R can be utilized for writing off capital losses also.

Some journal entry related to C/R: –

Difference Between Revenue and Capital: –

Basis |

Revenue |

Capital |

| Meaning | The retention of a share of net profits for the year | The reserve created out from the profit of capital nature |

| Affect on Net Profit | It does not affect the Net profit. | It does affect the Net profit |

| Source | It is created out from net profit. | it is created out from capital gain/profit. |

| During loss year | It can not be created in the loss year. | It can be created in the loss year. |

| Object | To strengthen the financial position and to meet the unknown liability. | to meet the capital loss of compliance of legal requirements. |

| Payment of Dividend | The dividend can be paid out of it without any preconditions | The dividend can be paid out of it with any preconditions of the company act. |

Thanks for reading the topic of “Reserve”, please comment with your feedback whatever you want. If you have any questions please ask us by commenting.