Question No 32 Chapter No 16 – Unimax Class 11

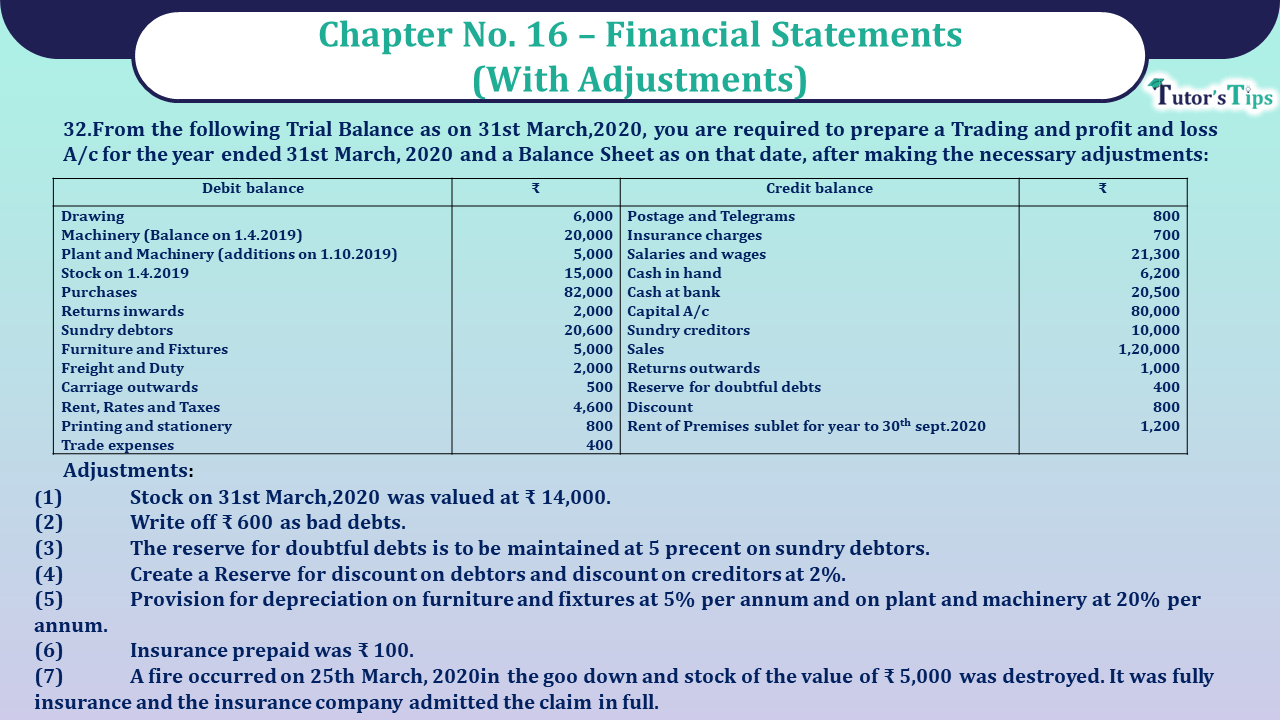

From the following Trial Balance as on 31st March,2020, you are required to prepare a Trading and profit and loss A/c for the year ended 31st March, 2020 and a Balance Sheet as on that date, after making the necessary adjustments:

| Debit balance | Amount | Credit balance | Amount |

| Drawing | 6,000 | Postage and Telegrams | 800 |

| Machinery (Balance on 1.4.2019) | 20,000 | Insurance charges | 700 |

| Plant and Machinery (additions on 1.10.2019) | 5,000 | Salaries and wages | 21,300 |

| Stock on 1.4.2019 | 15,000 | Cash in hand | 6,200 |

| Purchases | 82,000 | Cash at bank | 20,500 |

| Returns inwards | 2,000 | Capital A/c | 80,000 |

| Sundry debtors | 20,600 | Sundry creditors | 10,000 |

| Furniture and Fixtures | 5,000 | Sales | 1,20,000 |

| Freight and Duty | 2,000 | Returns outwards | 1,000 |

| Carriage outwards | 500 | Reserve for doubtful debts | 400 |

| Rent, Rates and Taxes | 4,600 | Discount | 800 |

| Printing and stationery | 800 | Rent of Premises sublet for year to 30th sept.2020 | 1,200 |

| Trade expenses | 400 |

Adjustments:

(1) Stock on 31st March,2020 was valued at ₹ 14,000.

(2) Write off ₹ 600 as bad debts.

(3) The reserve for doubtful debts is to be maintained at 5 precent on sundry debtors.

(4) Create a Reserve for discount on debtors and discount on creditors at 2%.

(5) Provision for depreciation on furniture and fixtures at 5% per annum and on plant and machinery at 20% per annum.

(6) Insurance prepaid was ₹ 100.

(7) A fire occurred on 25th March, 2020in the goo down and stock of the value of ₹ 5,000 was destroyed. It was fully insurance and the insurance company admitted the claim in full.

The solution of Question No 32 Chapter No 16 – UNIMAX Class 11

| Trading and Profit & Loss A/c Rakesh Roshan For the year ended 31st Dec., 2019 |

|||||

| Particulars |

Amount | Particulars |

Amount | ||

| To Opening stock | 15,000 | By sales | 1,20,000 | ||

| To purchases | 82,000 | Less: Returns inwards | 2,000 | 1,18000 | |

| Less: Returns outwards | 1,000 | 81,000 | By Closing stock | 14,000 | |

| To Freight & Duty | 2,000 | By Goods lost in fire | 5,000 | ||

| To Gross Profit | 39,000 | ||||

| (transferred to P & L A/c) | |||||

| 1,37,000 | 1,37,000 | ||||

| To Salaries & Wages | 21,300 | By Gross Profit b/d | 39,000 | ||

| To Insurance charges | 700 | By discount | 800 | ||

| Less: Prepaid | 100 | 600 | By Rent | 1,200 | 600 |

| To Postage & Telegrams | 800 | Less: Pre received | 600 | 200 | |

| To Trade expenses | 400 | By Discount on creditors | |||

| To Printing & Stationery | 800 | ||||

| To Rent, Rate and Taxes | 4,600 | ||||

| To Carriage outward | 500 | ||||

| To Bad debts | 600 | ||||

| Add: New Provision | 1,000 | ||||

| Less: Old Provision | 400 | 1,200 | |||

| To Depreciation debtors | 380 | ||||

| To Depreciation on furniture & Fixture | 250 | ||||

| To Dep. On Plant & Machinery | 4,000 | ||||

| To Dep. On Additional Plant& Machinery | 500 | ||||

| To Net Profit | |||||

| (Transferred to capital) | 5,270 | ||||

| 40,600 | 40,600 | ||||

| Balance Sheet of Mr. Rakesh As on 31st Dec., 2020 |

|||||

| Liabilities | Amount | Assets | Amount | ||

| Capital | 80,000 | Prepaid insurance | 100 | ||

| Add: Net Profit | 5,270 | Cash in hand | 6,200 | ||

| Less: Drawings | 6,000 | 79,270 | Cash at bank | 20,500 | |

| Sundry creditors | 10,000 | Furniture & Fixtures | 5,000 | ||

| Less: Discount | 200 | 9,800 | Less: Deprecation | 250 | 4,750 |

| Pre received Rent | 600 | Plant & Machinery | 20,000 | ||

| Less: Dep. (4,000+5,000) | 20,500 | ||||

| Closing stock | 14,000 | ||||

| Insurance claim | 5,000 | ||||

| Sundry debtors | 20,600 | ||||

| Less: bad debts | 600 | ||||

| Less: Provision | 1,000 | ||||

| Less: Discount | 380 | 18,620 | |||

| 89,670 | 89,670 | ||||

Thanks, Please Like and share with your friends

Comment if you have any Doubts.

Final Accounts: Meaning, Definition and Explanation

Profit and Loss Account: Meaning, Format & Examples

Balance Sheet: Meaning, Format & Examples

Also, Check out the solved question of all Chapters: –

Advanced Accountancy – Unimax Class 11 – 2021 – Solution.

Part-I

- Chapter No. 1 – Introduction of Accounting

- Chapter No. 2 – Theory Base of Accounting

- Chapter No. 3 – Vouchers and Transactions

- Chapter No. 4 – Journal

- Chapter No. 5 – Goods and Services Tax (GST): An Introduction

- Chapter No. 6 – Ledger

- Chapter No. 7 – Special Purpose Book – Cash Book

- Chapter No. 8 – Other Subsidiary Books

- Chapter No. 9 – Trial Balance

- Chapter No. 10 – Rectification of Errors

- Chapter No. 11 – Depreciation

- Chapter No. 12 – Provision and Reserves

- Chapter No. 13 – Bank Reconciliation Statement

- Chapter No. 14 – Bills of Exchange

Students may choose only one part from the Part II and Part III

Part-II

- Chapter No. 15 – Financial Statements (Without Adjustments)

- Chapter No. 16 – Financial Statements (With Adjustments)

- Chapter No. 17 – Accounts from Incomplete Records – Single Entry System

Part-III

- Chapter No. 18 – Introduction to Computers and Accounting information System

- Chapter No. 19 – Computerised Accounting

- Chapter No. 20 – Accounting Software: Tally

- Chapter No. 21 – Data Base System

- Chapter No. 22 – Concept of Entity and Relationship

Usha Publication – Elements of Book-Keeping PSEB (Class 11) – Solution

Chapter No. 2 – Theory Base of Accounting

Chapter No. 3 – Origin of Transactions

Chapter No. 4 – Vouchers and transactions

Chapter No. 6 – Accounting for Goods and Services Tax(GST)

Chapter No. 9 – Other Subsidiary Books

Chapter No. 10 – Journal Proper

Chapter No. 11 – Trial Balance

Chapter No. 12 – Bank Reconciliation Statement

Chapter No. 14 – Provisions and Reserves

Chapter No. 15 – Bills of Exchange

Chapter No. 16 – Rectification of Errors

Chapter No. 17 – Financial Statements – (Without Adjustments)

Chapter No. 18 – Financial Statements – (With Adjustments)

Check out T.S. Grewal +1 Book 2019 @ Oficial Website of Sultan Chand Publicatio