Question No 29 Chapter No 16 – Unimax Class 11

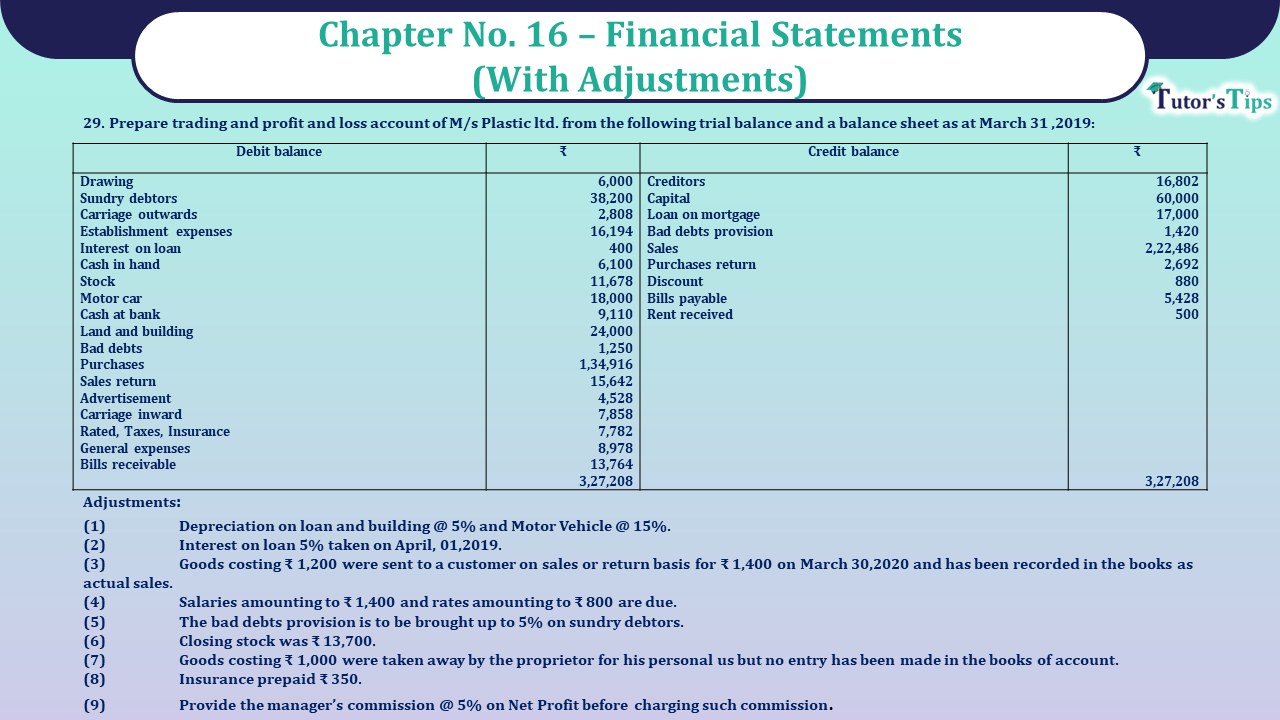

Prepare trading and profit and loss account of M/s Plastic ltd. from the following trial balance and a balance sheet as at March 31 ,2019:

| Debit balance | Amount | Credit balance | Amount |

| Drawing | 6,000 | Creditors | 16,802 |

| Sundry debtors | 38,200 | Capital | 60,000 |

| Carriage outwards | 2,808 | Loan on mortgage | 17,000 |

| Establishment expenses | 16,194 | Bad debts provision | 1,420 |

| Interest on loan | 400 | Sales | 2,22,486 |

| Cash in hand | 6,100 | Purchases return | 2,692 |

| Stock | 11,678 | Discount | 880 |

| Motor car | 18,000 | Bills payable | 5,428 |

| Cash at bank | 9,110 | Rent received | 500 |

| Land and building | 24,000 | ||

| Bad debts | 1,250 | ||

| Purchases | 1,34,916 | ||

| Sales return | 15,642 | ||

| Advertisement | 4,528 | ||

| Carriage inward | 7,858 | ||

| Rated, Taxes, Insurance | 7,782 | ||

| General expenses | 8,978 | ||

| Bills receivable | 13,764 | ||

| 3,27,208 | 3,27,208 |

Adjustments:

(1) Depreciation on loan and building @ 5% and Motor Vehicle @ 15%.

(2) Interest on loan 5% taken on April, 01,2019.

(3) Goods costing ₹ 1,200 were sent to a customer on sales or return basis for ₹ 1,400 on March 30,2020 and has been recorded in the books as actual sales.

(4) Salaries amounting to ₹ 1,400 and rates amounting to ₹ 800 are due.

(5) The bad debts provision is to be brought up to 5% on sundry debtors.

(6) Closing stock was ₹ 13,700.

(7) Goods costing ₹ 1,000 were taken away by the proprietor for his personal us but no entry has been made in the books of account.

(8) Insurance prepaid ₹ 350.

(9) Provide the manager’s commission @ 5% on Net Profit before charging such commission.

The solution of Question No 29 Chapter No 16 – UNIMAX Class 11

| Trading and Profit & Loss A/c of M/S Roni Plastic LTD. For the year ended 31st March, 2020 |

||||||

| Particulars |

Amount | Particulars |

Amount | |||

| To Opening stock | 11,678 | By sales | 2,22,486 | |||

| To purchases | 1,32,916 | Less: Returns | 15,642 | |||

| Less: Returns | 2,692 | Less: Sales return basis | 1,400 | 2,05,444 | ||

| Less: Drawings | 1,000 | 1,31,224 | By Closing stock | 13,700 | ||

| To Carriage inward | 7,858 | |||||

| To Gross Profit | 16,220 | |||||

| (transferred to P & L A/c) | 69,584 | Basis | 1,200 | 14,900 | ||

| 2,20,344 | 2,20,344 | |||||

| To Dep. On land and building | 1,200 | By Gross Profit b/d | 69,584 | |||

| To Dep. On Motor vehicle | 2,700 | By Discount | 880 | |||

| To interest on loan | 400 | By Rent | 500 | |||

| Add: Outstanding interest | 450 | 850 | ||||

| To Rates, Taxes, Insurance | 7,782 | |||||

| Add: Outstanding rates | 800 | |||||

| Less: Prepaid insurance | 350 | 8,232 | ||||

| To Bad debts | 1,250 | |||||

| Add: New Provision | 1,840 | |||||

| Less: Old Provision | 1,420 | 1,670 | ||||

| To Carriage outward | 2,808 | |||||

| To Establishments expenses | 16,194 | |||||

| To Advertisement | 4,528 | |||||

| To General expenses | 8,978 | |||||

| To Commission to Manager (22404*5/100) | 1,120 | |||||

| To Net Profit | ||||||

| (Transferred to capital) | 21,284 | |||||

| 70,964 | 70,964 | |||||

| Balance Sheet of Modern Traders As on 31st Dec., 2019 |

|||||

| Liabilities |

Amount | Assets |

Amount | ||

| Capital | 60,000 | Sundry debtors | 38,200 | ||

| Add: Net Profit | 21,284 | Less: Sales on Return basis | 1,400 | ||

| Less: Drawings | 7,000 | 74,284 | Less: Provision | 1,840 | 34,960 |

| Creditors | 16,802 | Cash | 6,100 | ||

| Loan on Mortgage | 17,000 | Motor car | 18,000 | ||

| Bills payable | 5,428 | Less: Depreciation | 2,700 | 15,300 | |

| Outstanding interest | 450 | Bank | 9,110 | ||

| Outstanding commission | 800 | Land & Building | 24,000 | ||

| To Manager | 1,120 | Less: Deprecation | 1,200 | 22,800 | |

| Outstanding salary | 1,400 | Bills receivable | 13,764 | ||

| Closing stock | 13,700 | ||||

| Add: stock on Returns basis | 1,200 | 14,900 | |||

| prep air insurance | 350 | ||||

| 1,17,284 | 1,17,284 | ||||

Thanks, Please Like and share with your friends

Comment if you have any Doubts.

Final Accounts: Meaning, Definition and Explanation

Profit and Loss Account: Meaning, Format & Examples

Balance Sheet: Meaning, Format & Examples

Also, Check out the solved question of all Chapters: –

Advanced Accountancy – Unimax Class 11 – 2021 – Solution.

Part-I

- Chapter No. 1 – Introduction of Accounting

- Chapter No. 2 – Theory Base of Accounting

- Chapter No. 3 – Vouchers and Transactions

- Chapter No. 4 – Journal

- Chapter No. 5 – Goods and Services Tax (GST): An Introduction

- Chapter No. 6 – Ledger

- Chapter No. 7 – Special Purpose Book – Cash Book

- Chapter No. 8 – Other Subsidiary Books

- Chapter No. 9 – Trial Balance

- Chapter No. 10 – Rectification of Errors

- Chapter No. 11 – Depreciation

- Chapter No. 12 – Provision and Reserves

- Chapter No. 13 – Bank Reconciliation Statement

- Chapter No. 14 – Bills of Exchange

Students may choose only one part from the Part II and Part III

Part-II

- Chapter No. 15 – Financial Statements (Without Adjustments)

- Chapter No. 16 – Financial Statements (With Adjustments)

- Chapter No. 17 – Accounts from Incomplete Records – Single Entry System

Part-III

- Chapter No. 18 – Introduction to Computers and Accounting information System

- Chapter No. 19 – Computerised Accounting

- Chapter No. 20 – Accounting Software: Tally

- Chapter No. 21 – Data Base System

- Chapter No. 22 – Concept of Entity and Relationship

Usha Publication – Elements of Book-Keeping PSEB (Class 11) – Solution

Chapter No. 2 – Theory Base of Accounting

Chapter No. 3 – Origin of Transactions

Chapter No. 4 – Vouchers and transactions

Chapter No. 6 – Accounting for Goods and Services Tax(GST)

Chapter No. 9 – Other Subsidiary Books

Chapter No. 10 – Journal Proper

Chapter No. 11 – Trial Balance

Chapter No. 12 – Bank Reconciliation Statement

Chapter No. 14 – Provisions and Reserves

Chapter No. 15 – Bills of Exchange

Chapter No. 16 – Rectification of Errors

Chapter No. 17 – Financial Statements – (Without Adjustments)

Chapter No. 18 – Financial Statements – (With Adjustments)

Check out T.S. Grewal +1 Book 2019 @ Oficial Website of Sultan Chand Publication