Question 43 Chapter 1 of Class 12 Part – 1

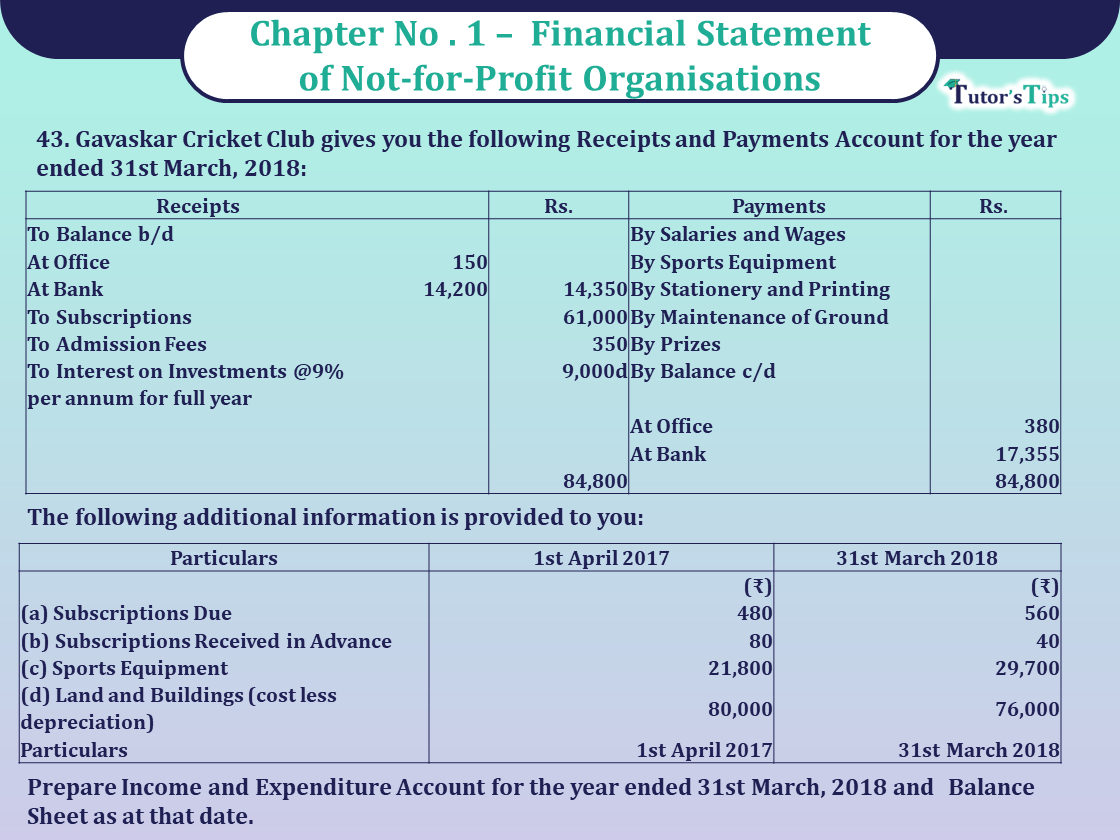

- Gavaskar Cricket Club gives you the following Receipts and Payments Account for the year ended 31st March, 2018:

| Receipts | Rs. | Payments | Rs. | ||

| To Balance b/d | By Salaries and Wages | 12,000 | |||

| At Office | 150 | By Sports Equipment | 46,785 | ||

| At Bank | 14,200 | 14,350 | By Stationery and Printing | 1,220 | |

| To Subscriptions | 61,000 | By Maintenance of Ground | 6,000 | ||

| To Admission Fees | 350 | By Prizes | 1,060 | ||

| To Interest on Investments @9% per annum for full year | 9,000d | By Balance c/d | |||

| At Office | 380 | ||||

| At Bank | 17,355 | 17,735 | |||

| 84,800 | 84,800 |

The following additional information is provided to you:

| Particulars | 1st April 2017 | 31st March 2018 |

| (a) Subscriptions Due | 480 | 560 |

| (b) Subscriptions Received in Advance | 80 | 40 |

| (c) Sports Equipment | 21,800 | 29,700 |

| (d) Land and Buildings (cost less depreciation) | 80,000 | 76,000 |

Prepare Income and Expenditure Account for the year ended 31st March, 2018 and

Balance Sheet as at that date.

The solution of Question 43 Chapter 1 of Class 12 Part – 1: –

Gavaskar Cricket Club

Income and Expenditure Account

For the year ended on 31st March, 2018

| Expenditure |

Amount | Income |

Amount | ||

| To Salaries and Wages | 12,000 | By Subscriptions | 61,000 | ||

| To Stationery and Printing | 1,220 | Less: Outstanding in the beginning | (480) | ||

| To Maintenance of ground | 6,000 | Add: Outstanding at the end | 560 | ||

| To Depreciation on Land and Building | 4,000 | Add: Received in Advance in the beginning | 80 | ||

| To Prizes | 1,060 | Less: Received in Advance at the end | (40) | 61,220 | |

| To Sports Equipments used | By Admission fees | 350 | |||

| Sports equipments purchased | 46,785 | By Interest on Investment | 9,000 | ||

| Add: Opening stock of sports equipments | 21,800 | ||||

| Less: Closing stock of sports equipments | (29,700) | ||||

| To Surplus. i.e., Excess of Income over Expenditure | 7,405 | ||||

| 70,570 | 70,570 | ||||

Balance Sheet (as at 1st April 2017)

| Liabilities |

Amount | Assets |

Amount | |

| Subscription Received in Advance | 80 | Sports Equipments 2180 | 21,800 | |

| Land and Building | 80,000 | |||

| Cash in Hand | 150 | |||

| Cash at Bank | 14,200 | |||

| Capital Fund (Balancing Figure) |

2,16,550 | Outstanding Subscriptions | 480 | |

| Investment =100×9,000/9 | 50,000 | |||

| 2,16,630 | 2,16,630 | |||

Balance Sheet (as at 31st March 2018)

| Liabilities |

Amount | Assets |

Amount | |

| Subscription Received in Advance | 40 | Investment | 1,00,000 | |

| Capital Fund | 2,16,550 | Outstanding Subscriptions | 560 | |

| Add: Surplus | 7,405 | 2,23,995 | Land and Building | 76,000 |

| Sports Equipments | 29,700 | |||

| Cash in Hand | 380 | |||

| Cash at Bank | 17,355 | |||

| 2,23,995 | 2,23,995 | |||

Thanks, Please Like and share with your friends

Comment if you have any questions.

Also, Check out the solved question of all Chapters: –

Usha Publication – Accountancy PSEB (Class 12) – Volume I – Solution

Chapter No. 1 – Accounting Not for Profit Organisations

Chapter No. 2 – Partnership Accounts – I (Introduction)

Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

Chapter No. 4 – Partnership Accounts – III (Reconstitution of Partnership)

Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

Chapter No. 8 – Company Accounts (Share Capital)

Chapter No. 9 – Company Accounts (Issue of Debentures)

Chapter No. 10 – Company Accounts (Redemption of Debentures)

Usha Publication – Accountancy PSEB (Class 12) – Volume II – Solution

Chapter No. 1 – Financial Statements of a Company

Chapter No. 2 – Financial Statement Analysis

Chapter No. 3 – Tools of Financial Statement Analysis- Comparative and Common Size

Chapter No. 4 – Ratio Analysis

Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication