Question 15 Chapter 7 – Unimax Class 12 Part 1 – 2021

Table of Contents

15. J, S and R were in partnership sharing profits and losses in the ratio of 3:2:1. Their balance sheet as on 31st December 2021 was as follows:

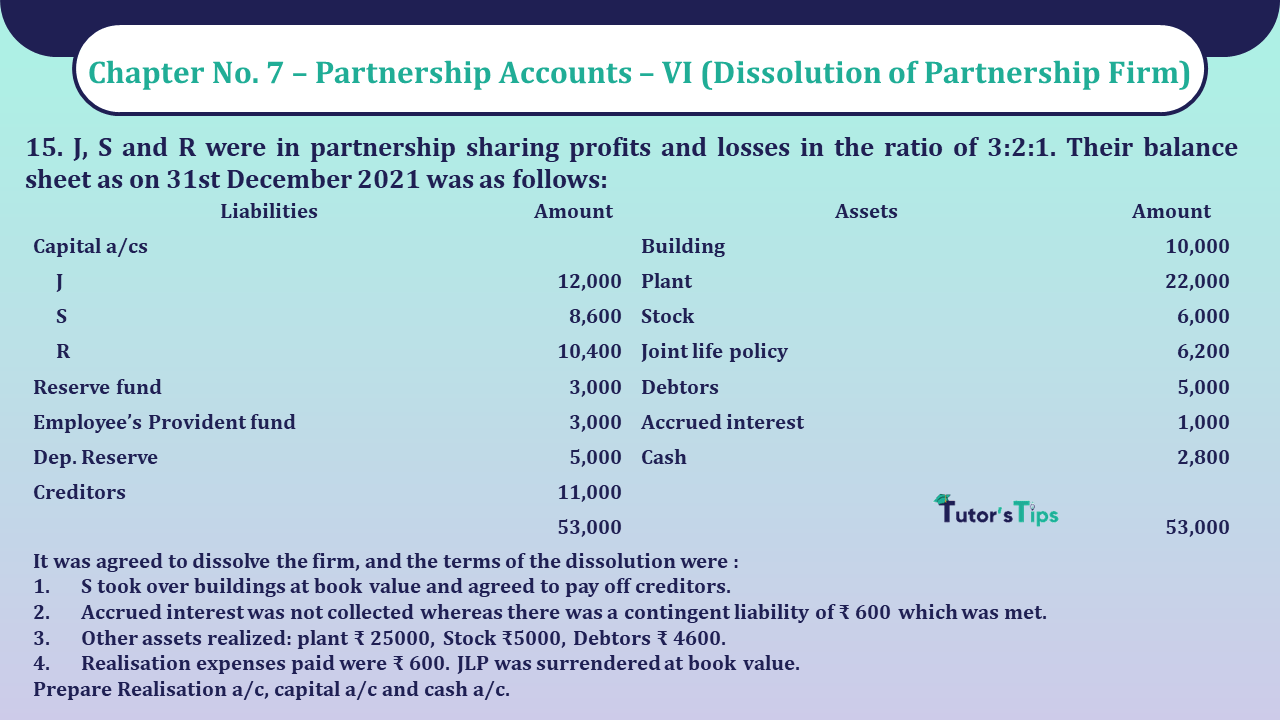

| Liabilities | Amount | Assets |

Amount | ||

| Capital a/cs | Building | 10,000 | |||

| J | 12,000 | Plant | 22,000 | ||

| S | 8,600 | Stock | 6,000 | ||

| R | 10,400 | Joint life policy | 6,200 | ||

| Reserve fund | 3,000 | Debtors | 5,000 | ||

| Employee’s Provident fund | 3,000 | Accrued interest | 1,000 | ||

| Depp. Reserve | 5,000 | Cash | 2,800 | ||

| Creditors | 11,000 | ||||

| 53,000 | 53,000 | ||||

It was agreed to dissolve the firm, and the terms of the dissolution were :

- S took over buildings at book value and agreed to pay off creditors.

- Accrued interest was not collected whereas there was a contingent liability of ₹ 600 which was met.

- Other assets realized: plant ₹ 25000, Stock ₹5000, Debtors ₹ 4600.

- Realisation expenses paid were ₹ 600. JLP was surrendered at book value.

Prepare Realisation a/c, capital a/c and cash a/c.

The solution of Question 15 Chapter 7 – Unimax Class 12 Part 1: –

Realisation a/c

| Particulars | Amount | Particulars |

Amount | ||

| To building | 10,000 | By employees Provident fund | 3,000 | ||

| To plant | 22,000 | By Depp. Reserve | 5,000 | ||

| To stock | 6,000 | By creditors | 11,000 | ||

| To JLP | 6,200 | By S’s capital a/c (building taken over) | 10,000 | ||

| To Debtors | 5,000 | By cash— | |||

| To accrued interest | 1,000 | Plant | 25,000 | ||

| To S’s capital a/c (cr. Paid) | 11,000 | Stock | 5,000 | ||

| To cash a/c— | JLP | 6,200 | |||

| Employee’s Provident fund | 3,000 | Debtors | 4,600 | ||

| Realisation exp. | 600 | ||||

| Pay. of contingent liab. | 600 | ||||

| To profit Trans. To cap. a/c | |||||

| J | 2,200 | ||||

| S | 1,467 | ||||

| R | 733 | 4,400 | |||

| 69,800 | 69,800 | ||||

Partner’s capital a/c

| Particulars | J | S | R | Particulars | J | S | R |

| To real. a/c (building taken over) | 10,000 | By balance b/d | 12000 | 8600 | 10400 | ||

| To cash a/c (B.F.) | 12,500 | 12,067 | 11,633 | By realisation a/c (cr. Paid) | 11000 | ||

| By realisation a/c (profit) | 2200 | 1467 | 733 | ||||

| By res. Fund | 1500 | 1000 | 500 | ||||

| 15,700 | 22,067 | 11,633 | 15,700 | 22,067 | 11,633 |

Cash a/c

| Particulars | Amount | Particulars | Amount |

| To balance b/d | 2,800 | By realisation a/c | |

| To realisation a/c | Employee’s Provident fund | 3,000 | |

| Plant | 25,000 | Realisation expenses | 600 |

| Stock | 5,000 | Payment of contingent liability | 600 |

| Debtors | 4,600 | Capitals | |

| JLP | 6,200 | J | 15,700 |

| S | 12,067 | ||

| R | 11,633 | ||

| 43,600 | 43,600 |

For more Explanation please check out the following link: –

Read out the full article

Dissolution of a Partnership Firm – its Methods

Also, Check out the same article in Hindi from the following link

Dissolution of a Partnership Firm – its Methods – in Hindi

Accountancy – Unimax Class 12 Part 1 – 2021 – Solution.

- Chapter No. 1 – Accounts of Non-Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Basic Concepts)

- Chapter No. 3 – Partnership Accounts – II (Goodwill)

- Chapter No. 4 – Partnership Accounts – III (Change in Profit Sharing Ratio among Existing Partners)

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

Accountancy – Unimax Class 12 Part 2 – 2021 – Solution.

- Chapter No. 1 – Share Capital

- Chapter No. 2 – Debentures

- Chapter No. 3 – Financial Statements of A Company (Balance Sheet Only)

- Chapter No. 4 – Analysis of Financial Statements

- Chapter No. 5 – Ratio Analysis

- Chapter No. 6 – Cash Flow Statement

Check out Other Publishers’ Book’s Solution:

Class +2 – Accounting Books solutions for free

Usha Publication Accountancy Class 12 – Part – 1 – PSEB- Solution

Usha Publication Accountancy Class 12 – Part – 2 – PSEB- Solution

T.S. Grewal’s Book Keeping +2 Part – A Vol. I – Solution

T.S. Grewal’s Book Keeping +2 Part – A Vol. II – Solution

T.S. Grewal’s Book Keeping +2 Part – B – Solution