Question 16 Chapter 7 – Unimax Class 12 Part 1 – 2021

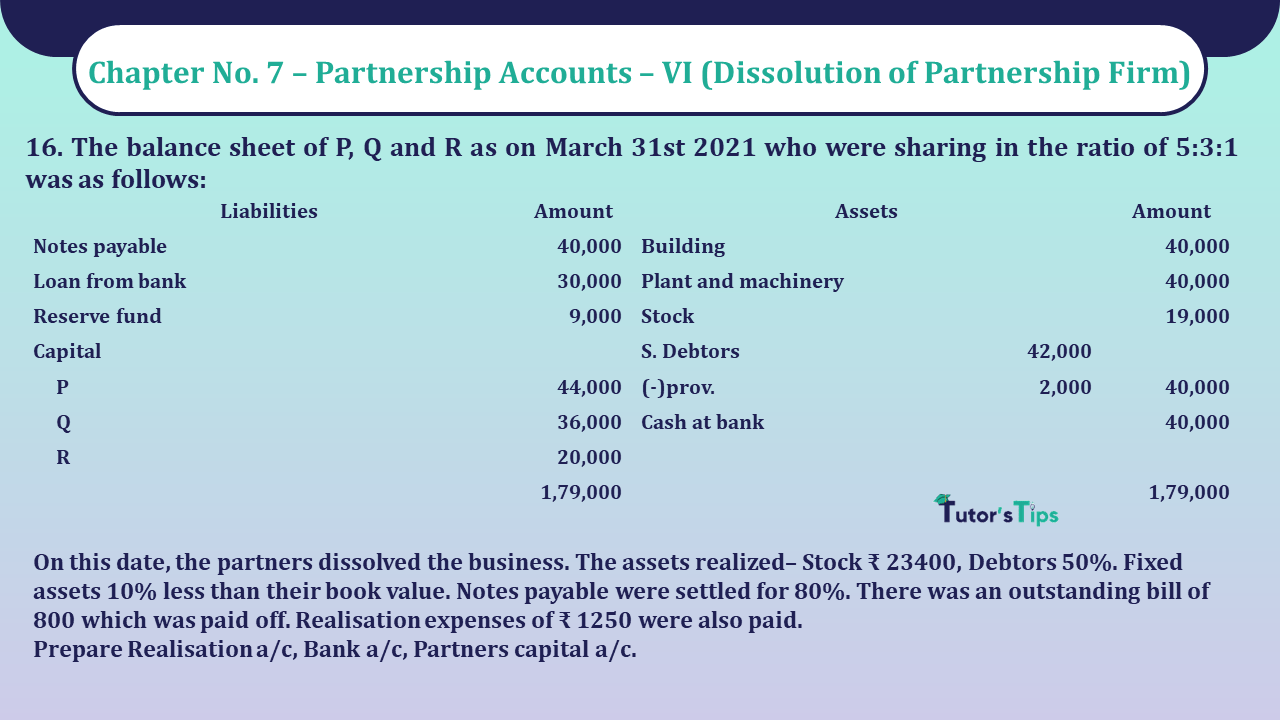

16. The balance sheet of P, Q and R as on March 31st 2021 who were sharing in the ratio of 5:3:1 was as follows:

| Liabilities | Amount | Assets |

Amount | ||

| Notes payable | 40,000 | Building | 40,000 | ||

| Loan from bank | 30,000 | Plant and machinery | 40,000 | ||

| Reserve fund | 9,000 | Stock | 19,000 | ||

| Capital | S. Debtors | 42,000 | |||

| P | 44,000 | (-)prov. | 2,000 | 40,000 | |

| Q | 36,000 | Cash at bank | 40,000 | ||

| R | 20,000 | ||||

| 1,79,000 | 1,79,000 | ||||

On this date, the partners dissolved the business. The assets realized– Stock ₹ 23400, Debtors 50%. Fixed assets 10% less than their book value. Notes payable were settled for 80%. There was an outstanding bill of 800 which was paid off. Realisation expenses of ₹ 1250 were also paid.

Prepare Realisation a/c, Bank a/c, Partners capital a/c.

The solution of Question 16 Chapter 7 – Unimax Class 12 Part 1: –

Realisation a/c

| Particulars | Amount | Particulars |

Amount | ||

| To building | 40,000 | By provision for d.d. | 2,000 | ||

| To plant and machinery | 40,000 | By notes payable | 40,000 | ||

| To stock | 19,000 | By loan from bank | 30,000 | ||

| To S. Debtors | 42,000 | By cash a/c— | |||

| To cash a/c | Stock | 23,400 | |||

| Notes payable | 32,000 | Debtors | 21,000 | ||

| Payment of outstanding bill | 800 | Building | 36,000 | ||

| Realisation expenses | 1,250 | Plant and machinery | 36,000 | ||

| Loan from bank | 30,000 | By loss on real. Trans. to capital a/cs | |||

| P | 9,250 | ||||

| Q | 5,550 | ||||

| R | 1,850 | 16,650 | |||

| 2,05,050 | 2,05,050 | ||||

Partner’s capital a/c

| Particulars | p | Q | R | Particulars | p | Q | R |

| To real. a/c (loss) | 9,250 | 5,550 | 1,850 | By balance b/d | 44,000 | 36,000 | 20,000 |

| To cash a/c (B.F.) | 39,750 | 33,450 | 19,150 | By res. Fund | 5,000 | 3,000 | 1,000 |

| 49,000 | 39,000 | 21,000 | 49,000 | 39,000 | 21,000 |

Cash a/c

| Particulars | Amount | Particulars | Amount |

| To balance b/d | 40,000 | By realisation a/c— | |

| To realisation a/c— | Notes payable | 32,000 | |

| Stock | 23,400 | Payment of outstandings | 800 |

| Debtors | 21,000 | Realisation expenses | 1,250 |

| Building | 36,000 | Loan from bank | 30,000 |

| Plant and machinery | 36,000 | Capital | |

| P | 39,750 | ||

| Q | 33,450 | ||

| R | 19,150 | ||

| 1,56,400 | 1,56,400 |

For more Explanation please check out the following link: –

Read out the full article

Dissolution of a Partnership Firm – its Methods

Also, Check out the same article in Hindi from the following link

Dissolution of a Partnership Firm – its Methods – in Hindi

Accountancy – Unimax Class 12 Part 1 – 2021 – Solution.

- Chapter No. 1 – Accounts of Non-Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Basic Concepts)

- Chapter No. 3 – Partnership Accounts – II (Goodwill)

- Chapter No. 4 – Partnership Accounts – III (Change in Profit Sharing Ratio among Existing Partners)

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

Accountancy – Unimax Class 12 Part 2 – 2021 – Solution.

- Chapter No. 1 – Share Capital

- Chapter No. 2 – Debentures

- Chapter No. 3 – Financial Statements of A Company (Balance Sheet Only)

- Chapter No. 4 – Analysis of Financial Statements

- Chapter No. 5 – Ratio Analysis

- Chapter No. 6 – Cash Flow Statement

Check out Other Publishers’ Book’s Solution:

Class +2 – Accounting Books solutions for free

Usha Publication Accountancy Class 12 – Part – 1 – PSEB- Solution

Usha Publication Accountancy Class 12 – Part – 2 – PSEB- Solution

T.S. Grewal’s Book Keeping +2 Part – A Vol. I – Solution

T.S. Grewal’s Book Keeping +2 Part – A Vol. II – Solution

T.S. Grewal’s Book Keeping +2 Part – B – Solution