Bills of Exchange / Bills Receivable (B/R) : –

Bills of Exchange is an instrument in writing form which is signed by the accepter (known as Drawee), directing a certain person (known as Drawer) to pay a certain amount against the purchase of goods and services. In other words, it is an instrument of debt written by the seller of goods and services and accepted by the buyer of goods and services.

Bills of Exchange are Bills Receivable for the seller(drawer) and bills payable for the buyer (drawee).

Bills Receivable is as assets and Bills Payable is the Liabilities.

It is used as security where both the parties (Seller & buyer) don’t know each other, also discountable from the bank if drawer/seller ready to pay some amount of interest to the bank, also transferable to the creditor.

Parties involved in the B/R shown below: –

- Drawer

- Drawee

- Payee

1. Drawer : –

A Drawer is a person who sells goods and services or who draws a bill.

2. Drawee: –

A Drawee is a person who purchases goods and services or who accepts a bill.

3. Payee: –

A payee is a person to whom the payment is to be made.

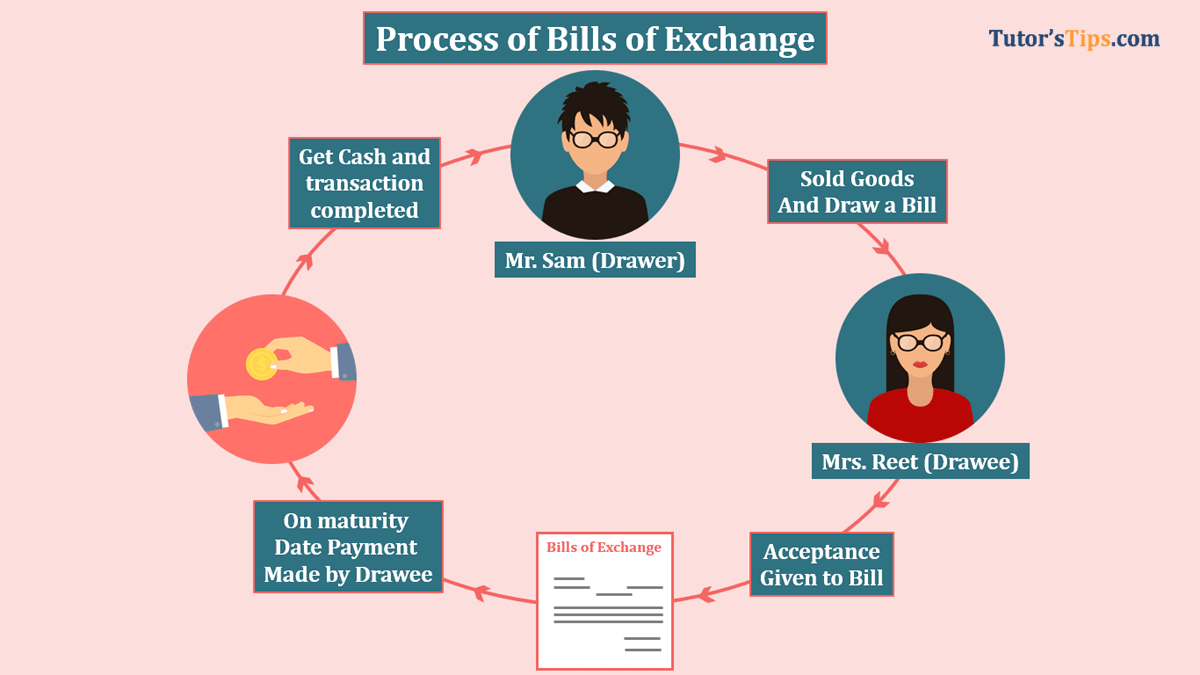

The process of creating Bills Receivable : –

I will explain to you the whole process of creating it in steps as shown below: –

In the above image, firstly seller sold goods to the buyer/customer and then draw a bill on him.

Buyer received a bill and accepts it with any condition.

On maturity of bill buyer will pay a sum of amount to the payee. (Payee may be a bank or Drawer himself)

we will explain about payee in Bills of Exchange chapter because it is a vast topic here we are trying to explain a simple meaning of B/R.

The format of Bills Receivable Book: –

The format of the B/R book shown below : –

Example : –

Suresh wants to purchase goods but he did not have liquid cash to pay for goods and he did not know any seller of this type of goods. He went to the market and met with Mr. Ramesh. He is asking him for a security proof of payment then Mr. Suresh told him that draw a bill Receivable on me, I will accept it.

So, Suresh feels secure with B/R, he accepts the deal.

01/04/2018 Ramesh Sold goods to Suresh for Rs. 10,000/- on credit and he draw a bill for 3 Months. Ramesh accepts the B/R On maturity B/R met.

Journal Entry for it shown below:

In the Books of Mr Ramesh ( Drawer )

1. Sold goods for Rs 10,000/-

01/04/2018 Suresh A/c Dr. 10,000

To Sale A/c 10,000

(Being Goods Sold to Suresh )

2. Acceptance of B/R received from Suresh

01/04/2018 B/R A/c Dr. 10,000

To Suresh A/c 10,000

(Being acceptance received )

3. On Maturity: payment met

04/07/2018 Bank A/c Dr. 10,000

To B/R A/c 10,000

(Being payment Received against B/R on maturity )

*Note: Maturity Date will we calculated as following

| Date of accepting B/R | 01/04/2018 |

| Add: Period of B/R | 3 Months |

| 01-07-2018 | |

| Add: 3 Days of grace | 3 Days |

| Maturity Date | 04/07/2018 |

We have only single B/R, I will show u how to post it into the B/R Books

If you have any questions about this topic of Petty Cash Book please ask it in the comment section below.

Thanks

Check out Financial Accounting Books @ Amazon.in