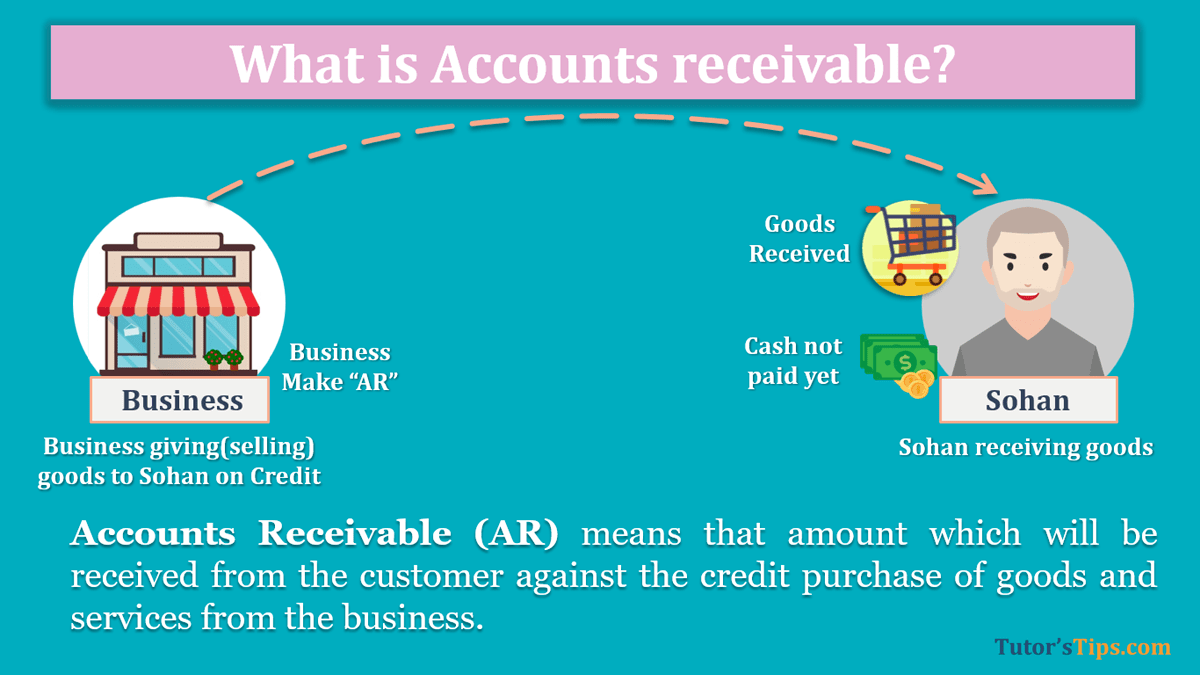

Accounts Receivable (AR) means that amount which will be received from the customer against the credit purchase of goods and services from the business. At the end of the financial year, the total amount of AR is shown on the balance sheet under the group of Current Assets.

Normally, AR is also known as Trade Receivable, But AR is the part of Trade Receivable. Trade Receivable also include Promissory Notes Receivable. So, we can divide Trade Receivable into two major types. These are shown below:

- Accounts Receivable

- Promissory Notes Receivable

1. Accounts Receivable:

AR is that amount of receivables which has no maturity date. it will receive after 1 week or after 1 year, it depends on the customer who purchased goods on credit.

2. Promissory Notes Receivable:

Promissory Notes Receivable is that amount of receivables which has a maturity date. It can be encashed on or after the maturity date in full. If you want to encash it before the maturity, then you have to pay some amount of interest to the payee(Bank). Bills Receivable is the main example of Promissory Nated receivables.

Examples of Accounts Receivable: –

A&B Co. sold goods to the C&D co. worth Rs 1,00,000 on credit. So, C&D Co. has now become an account receivable for the A&B Co. till the date of payment.

Benefits of Accounts Receivable: –

AR provides a lot of benefits to the business. It plays a vital role in the growth of the business because of it the part of current assets. So, current assets use while calculating the liquidity ratio of the business. AR shows that the business will receive that amount in future.

You can also read the following topics : –

- Assets – Meaning, Definition, Types and Examples

- Liabilities – Meaning, Types and Examples

- What is Capital – Meaning and Example

Thanks Please share with your friends

Comment if you have any question

Check out Financial Accounting Books @ Amazon.in