Usha 2024 – Class 12

Usha-2024-Part I – Solution

Usha-2024-Part II – Solution

Book Solutions

Class +1 – Accountancy

Usha Publication Book’s Solution – PSEB

Unimax Publications Book’s Solution – PSEB

D K Goel Book’s Solution – ISC

T.S. Grewal’s Book’s Solution – CBSE

Class +2 – Accountancy

Usha Publication – Part I – Solution

Usha Publication – Part II – Solution

Unimax Publications Part 1 – Solution

Unimax Publications Part 2 – Solution

T.S. Grewal’s Book Part – A Vol. I – Solution

T.S. Grewal’s Book Part – A Vol. II – Solution

T.S. Grewal’s Book Part B – Solution

V K Publications Part B– Solution

Video Lectures

Video Lectures Class 11

Accounts

Business Studies

Economics

Video Lectures Class 12

Accounts

Business Studies

Economics

Store

Balance Sheets Terms

Ads loading…

What is Inventory – Types of Inventories – Example

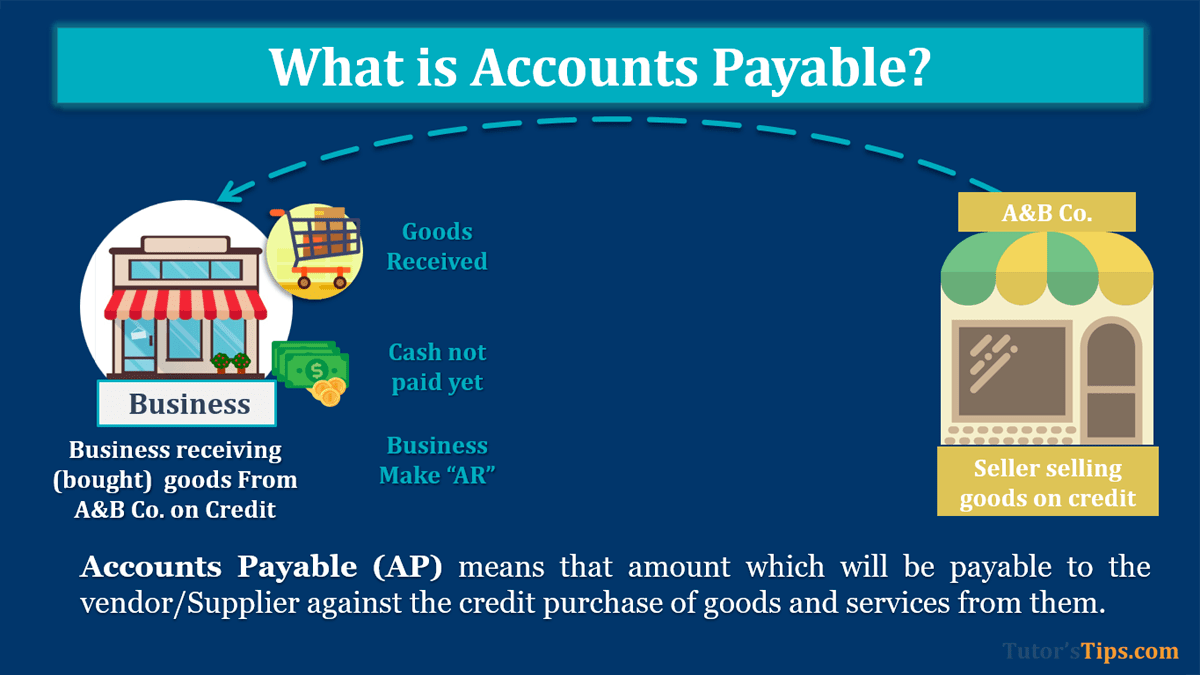

What is Accounts Payable (AP) – Explanation

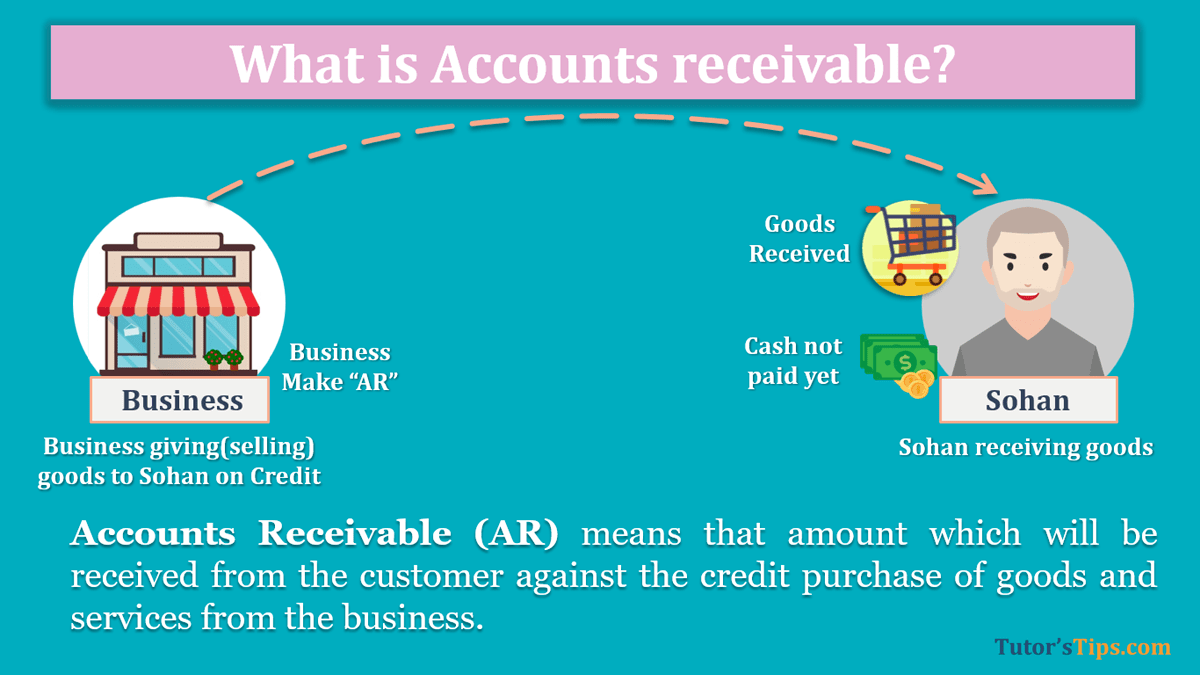

What is Accounts Receivable (AR) – Explanation

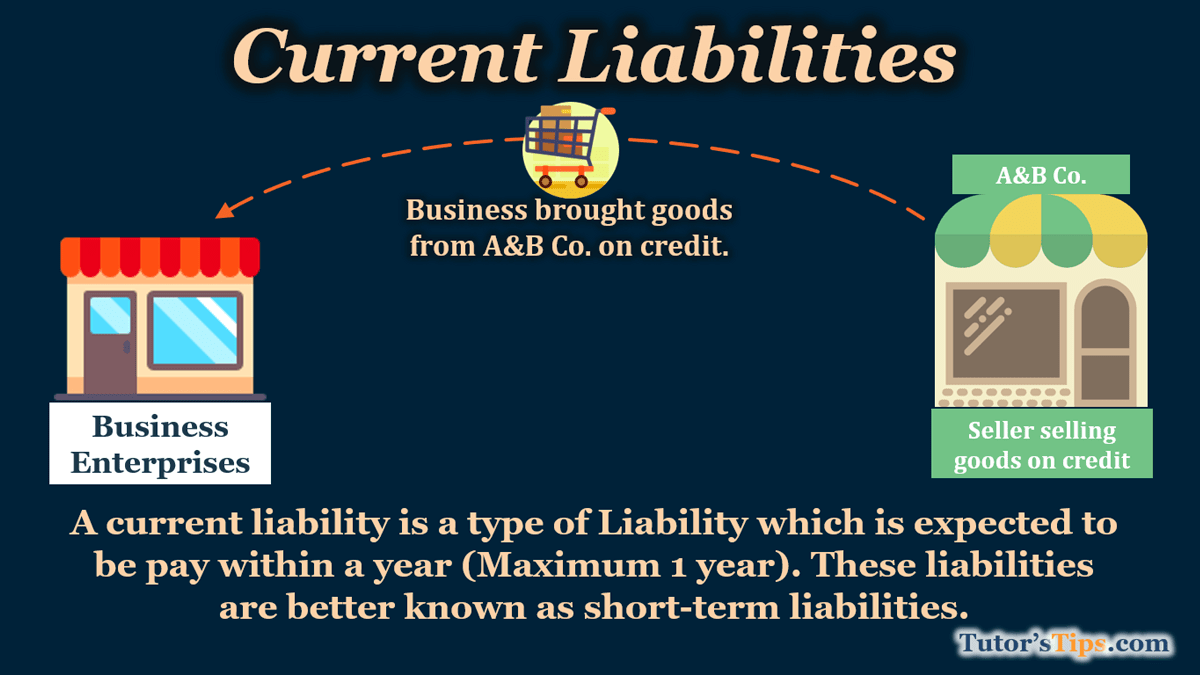

What are Current liabilities – Explained with Examples

Non Current liabilities – Explained with Examples

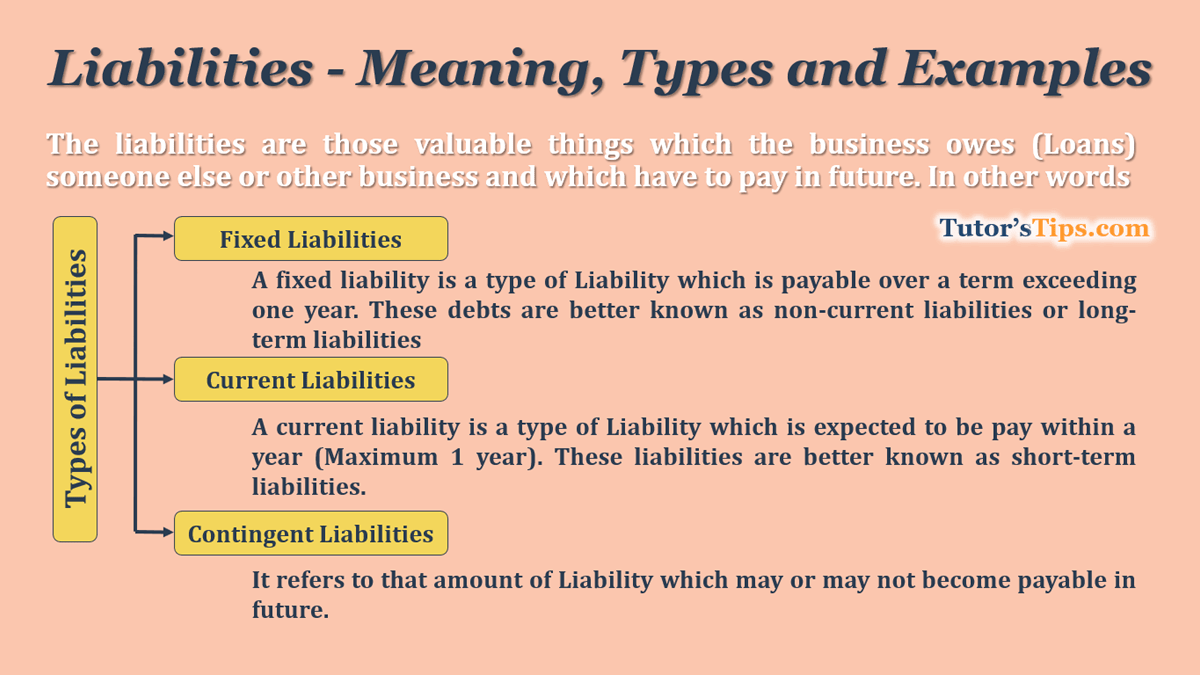

Liabilities – Meaning, Types and Examples

What is Drawing – Meaning and Examples

What is Capital – Meaning and Example

Non Performing Assets or NPA- Meaning and Examples

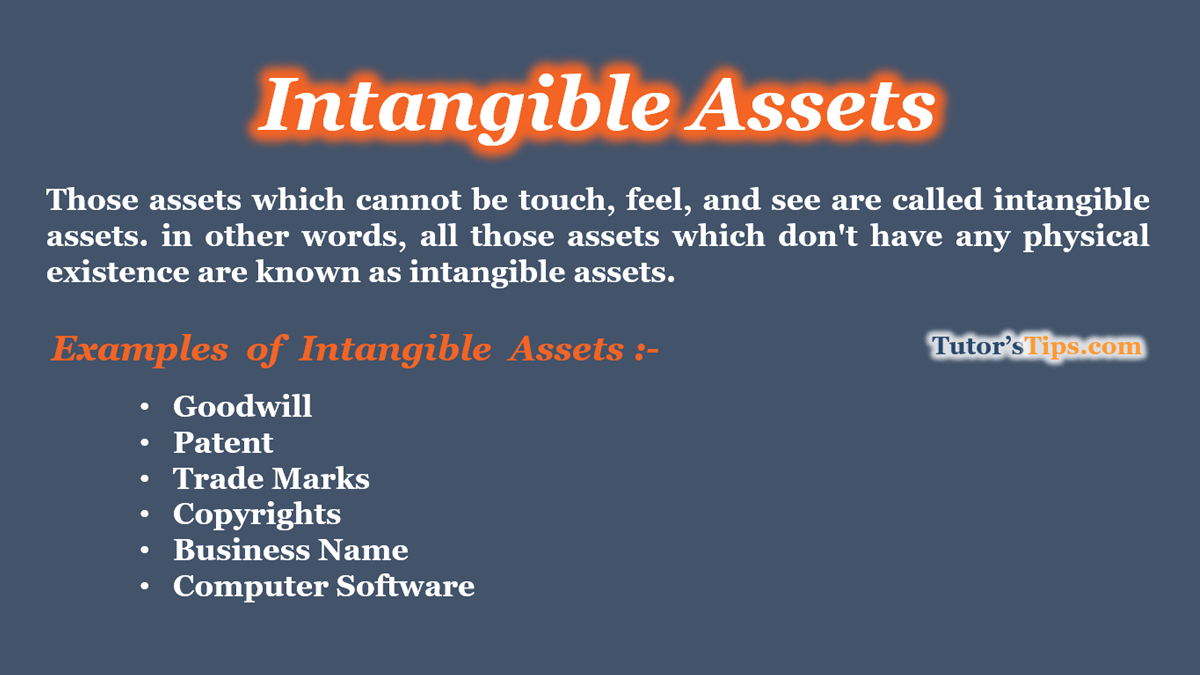

Intangible Assets – Explained with example

Ads loading…

Advertisement

1

2

Crazy Pachinko bonus

statistiky Crazy Time

Crazy Time live Italia

Coin Flip Crazy Time

hur spelar man Crazy Time

Royal Reels casino

Crazy Time strategies UK

ATG App Sverige

error:

Content is protected !!