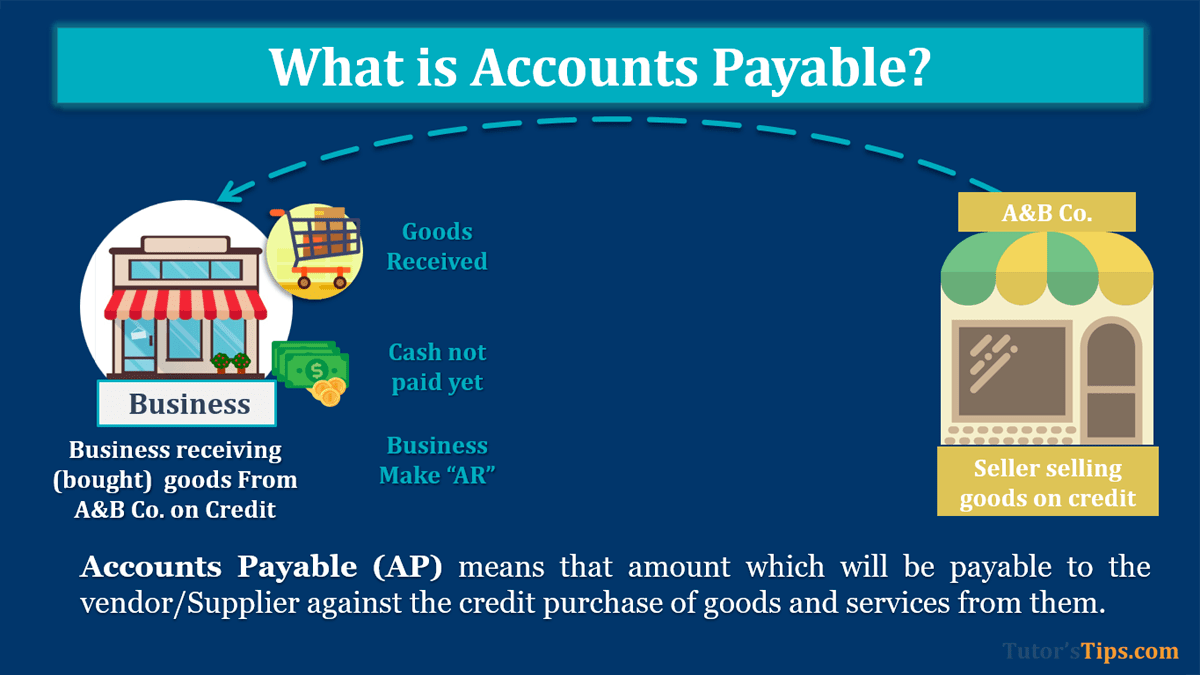

Accounts Payable (AP) means that amount which will be payable to the vendor/Supplier against the credit purchase of goods and services from them. At the end of the financial year, the total amount of AP is shown on the balance sheet under the group of Current Liabilities.

Normally, AP is also known as Trade Payable, But AP is the part of Trade Payable. Trade Payable also include Promissory Notes Payable. So, we can divide Trade Payable into two major types. These are shown below:

- Accounts Payable

- Promissory Notes Payable

1. Accounts Payable:

AP is that amount of payables which has no maturity date. it will pay after 1 week or after 1 year, it depends on the availability of the funds.

2. Promissory Notes Payable:

Promissory Notes Payable is that amount of Payable which has a maturity date. It will have to be paid on the maturity date in full. If a business fails to pay the due amount of Bills payables then the business has to pay some additional charges to the vendor/supplier. Bills Payable is the main example of Promissory Notes Payable.

Examples of Accounts Payable: –

A&B Co. Purchase goods to the C&D co. worth Rs 1,00,000 on credit. So, C&D Co. has now become an account Payable for the A&B Co. till the date of payment.

Benefits of Accounts Payable: –

AP provides a lot of benefits to the business. It plays a vital role in the growth of the business because it is part of current liabilities. So, current liabilities use while calculating the liquidity ratio of the business. AP shows that the business will pay that amount in future.

Placement of a Accounts Payable in the balance sheet: –

The placement of a Accounts Payable in the balance sheet should be shown under the group Current Liabilities. These are shown in the following format of the balance sheet and highlighted with orange colour: –

| Name of the Entity | |||

| Balance Sheet as on 31st March, _______ |

|||

| Liabilities | Amount | Assets | Amount |

| Current Liabilities | Current Assets | ||

| Trade Creditors | Cash in hand | ||

| Bills Payable | Cash at Bank | ||

| Outstanding Expenses | Inventories | ||

| Advance/Unearned Incomes | Bills payable | ||

| Short term loans | Sundry Debtors | ||

| Non-Current Liabilities | Prepaid Expenses | ||

| long terms loans | Accrued Incomes | ||

| Debentures | Fixed/Non-Current Assets | ||

| Capital | Building | ||

| Add: Net profit | Land | ||

| interest on Capital |

Plant & machine | ||

| Less: Drawings | Furniture & fixture | ||

| Net Loss | Goodwill | ||

You can also read the following topics : –

- Assets – Meaning, Definition, Types and Examples

- Liabilities – Meaning, Types and Examples

- What is Capital – Meaning and Example

Thanks Please share with your friends

Comment if you have any question

Check out Financial Accounting Books @ Amazon.in