Advertisement

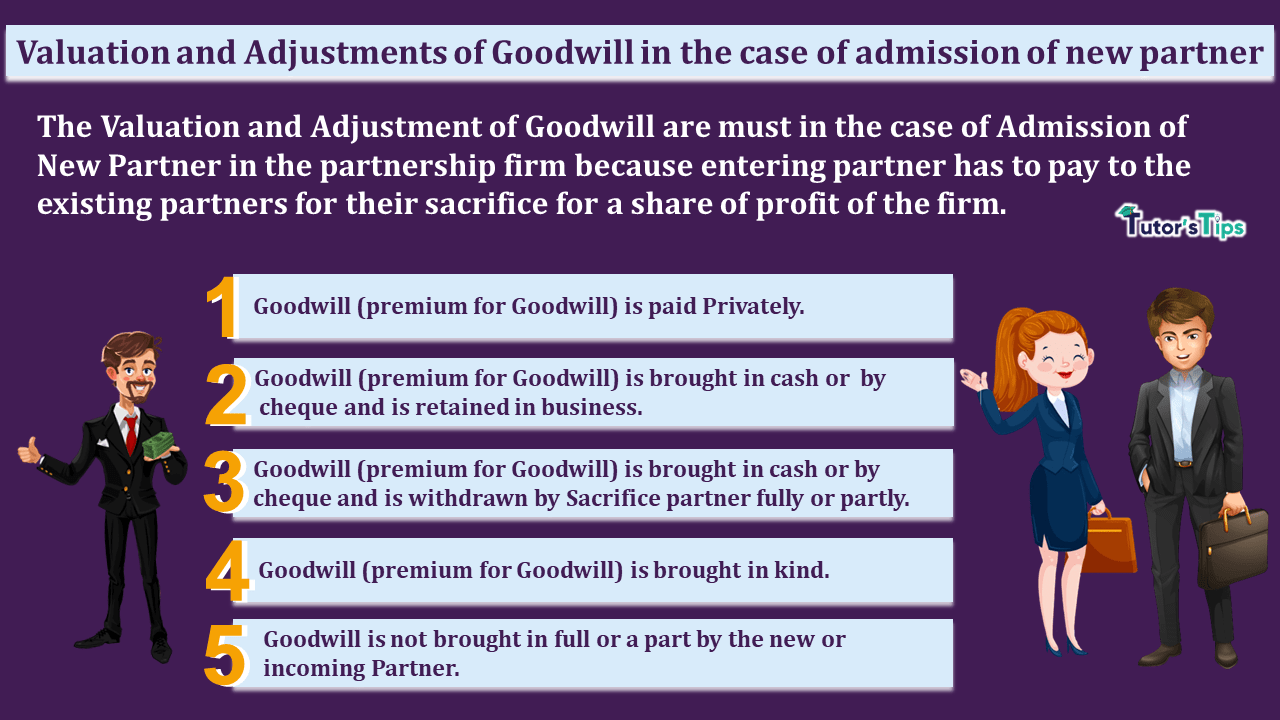

The Valuation and Adjustment of Goodwill are must in the case of Admission of New Partner in the partnership firm because entering partner has to pay to the existing partners for their sacrifice for a share of profit of the firm.

Advertisement

Goodwill is a super profit of the firm means that profit which is earned extra by the firm from the normal profit earned by the other businesses in the same industry. The firm earned extra profit because of efforts made by existing the past. So that’s why they want the share of that goodwill for the entering partner.

What is the Valuation of Goodwill:

Every aged business has brand value, the faith of customers and satisfaction of employees. Any business who wants to purchase another business it has to pay some amount for all these above factors, this extra amount is known as goodwill. So at the time of selling and buying the business has to calculate the valuation of goodwill. There is a various method to calculate the value of Goodwill which are explained in the following article:-

Methods of Valuation of Goodwill – Explained with illustrations

What is the Adjustment of Goodwill: –

Advertisement-X

The goodwill of the firm will be adjustment among the old partners because this is belonging to them. The adjustment entries are recorded in the books of account for adjustment of goodwill. The adjustment entries are different and recorded on the basis of treatment of goodwill, in the case of admission of the new partner. The various accounting treatment of Goodwill as shown as follows: –

1. Paid it privately to the existing partner: –

When the goodwill is paid by the new partner privately to the existing or sacrificing partners, In this case, the journal will be posted in the books of accounts.

2. Brought it in cash or by cheque by the New partner and retained in the business.

When the New partner brought his share of goodwill or premium for goodwill in cash or by cheque and existing partners decide to retain the goodwill in the business then it will be transfers

Journal Entries: –

| Date | Particulars | L. F. | Debit | Credit | |

| Goodwill brought in cash by a new partner | |||||

| 1. | Cash/Bank A/c | Dr. | XXXX | ||

| To premium for goodwill A/c | XXXX | ||||

| (Being New/entering partner bring his share of goodwill in cash) | |||||

| Capital brought in cash by a new partner | |||||

| 2. | Cash/Bank A/c | Dr. | XXXX | ||

| To New Partner Capital A/c | XXXX | ||||

| (Being cash received against the issue of capital to new Partner) | |||||

| Share of goodwill distributed among the sacrificing partners | |||||

| 3. | Premium for goodwill A/c | Dr. | XXXX | ||

| To Sacrifice Partner Capital/Current A/c | XXXX | ||||

| (Being premium for goodwill brought by new partner distributed by the sacrificing partner in the sacrificing ratio) | |||||

Note: – Current Account will be treated when there is an account of capital has fixed in nature.

Alternative Journal Entries: –

| Date | Particulars | L. F. | Debit | Credit | |

| Combine entry for both brought in cash by a new partner | |||||

| 1. | Cash/Bank A/c | Dr. | XXXX | ||

| To premium for goodwill A/c | XXXX | ||||

| To New Partner Capital A/c | XXXX | ||||

| (Being New/entering partner bring his share of goodwill and capital in cash) | |||||

| Share of goodwill distributed among the sacrificing partners | |||||

| 2. | Premium for goodwill A/c | Dr. | XXXX | ||

| To Sacrifice Partner Capital/Current A/c | XXXX | ||||

| (Being premium for goodwill brought by new partner distributed by the sacrificing partner in the sacrificing ratio) | |||||

3. Brought it in cash or by cheque by the New partner and withdrawn by the Sacrificing Partners fully or partly: –

When the New partner brought his share of goodwill or premium for goodwill in cash or by cheque and it will distribute among the existing/sacrificing partners in their sacrificing ratio. The existing/ Sacrificing partners have the right to withdraw the amount of goodwill in full or partly. All the above journal entries as explained in the above treatment will remain the same just one new journal entry will be recorded in the books, this is shown as follows: –

Journal Entries: –

| Date | Particulars | L. F. | Debit | Credit | |

| Amount of Goodwill withdrawal by the sacrificing partner in Cash | |||||

| 1. | Premium for goodwill A/c | Dr. | XXXX | ||

| To Cash/Bank A/c | XXXX | ||||

| (Being amount of Goodwill withdrawal by the sacrificing partner in cash) | |||||

Note: – The amount can be withdrawal fully or partly. The will be debited and credited as per withdrawal by the sacrificing partner.

4. When brought in Kind: –

Advertisement-X

When the New partner brought his share of goodwill or premium for goodwill and his capital in kind and existing partners decide to retain the goodwill in the business then it will be transfers

Journal Entries: –

| Date | Particulars | L. F. | Debit | Credit | |

| Goodwill brought in Kind by a new partner | |||||

| 1. | Asset A/c | Dr. | XXXX | ||

| To premium for goodwill A/c | XXXX | ||||

| (Being New/entering partner bring his share of goodwill in-kind ) | |||||

| Capital brought in Kind by a new partner | |||||

| 2. | Asset A/c | Dr. | XXXX | ||

| To New Partner Capital A/c | XXXX | ||||

| (Being Asset received against the issue of capital to new Partner) | |||||

| Share of goodwill distributed among the sacrificing partners | |||||

| 3. | Premium for goodwill A/c | Dr. | XXXX | ||

| To Sacrifice Partner Capital/Current A/c | XXXX | ||||

| (Being premium for goodwill brought by new partner distributed by the sacrificing partner in the sacrificing ratio) | |||||

Note: – Current Account will be treated when there is an account of capital has fixed in nature.

Alternative Journal Entries: –

| Date | Particulars | L. F. | Debit | Credit | |

| Combine entry for both brought in cash by a new partner | |||||

| 1. | Asset A/c | Dr. | XXXX | ||

| To premium for goodwill A/c | XXXX | ||||

| To New Partner Capital A/c | XXXX | ||||

| (Being New/entering partner bring his share of goodwill and capital in cash) | |||||

| Share of goodwill distributed among the sacrificing partners | |||||

| 2. | Premium for goodwill A/c | Dr. | XXXX | ||

| To Sacrifice Partner Capital/Current A/c | XXXX | ||||

| (Being premium for goodwill brought by new partner distributed by the sacrificing partner in the sacrificing ratio) | |||||

5. When not brought in full or part by the new partner: –

When the New partner brought his share of goodwill or premium for goodwill less then the actual amount due then the balance amount will be debited from his/her capital/current account. The journal entries are shown as follows: –

Journal Entries: –

| Date | Particulars | L. F. | Debit | Credit | |

| Combine entry for both brought in cash by a new partner | |||||

| 1. | Cash/Bank A/c | Dr. | XXXX | ||

| To premium for goodwill A/c | XXXX | ||||

| To New Partner Capital A/c | XXXX | ||||

| (Being New/entering partner bring his share of goodwill and capital in cash) | |||||

| Share of goodwill distributed among the sacrificing partners | |||||

| 2. | Premium for goodwill A/c | Dr. | XXXX | ||

| New Partner Capital/Current A/c | Dr. | XXXX | |||

| To Sacrifice Partner Capital/Current A/c | XXXX | ||||

| (Being premium for goodwill brought by new partner distributed by the sacrificing partner in the sacrificing ratio) | |||||

Note: – Current Account will be treated when there is an account of capital has fixed in nature.

Thanks for reading the topic.

please comment your feedback whatever you want. If you have any question please ask us by commenting.

Advertisement-X

Check out T.S. Grewal’s +2 Book 2020 @ Official Website of Sultan Chand Publication

Advertisement-Y