Question No 5 Chapter No 10

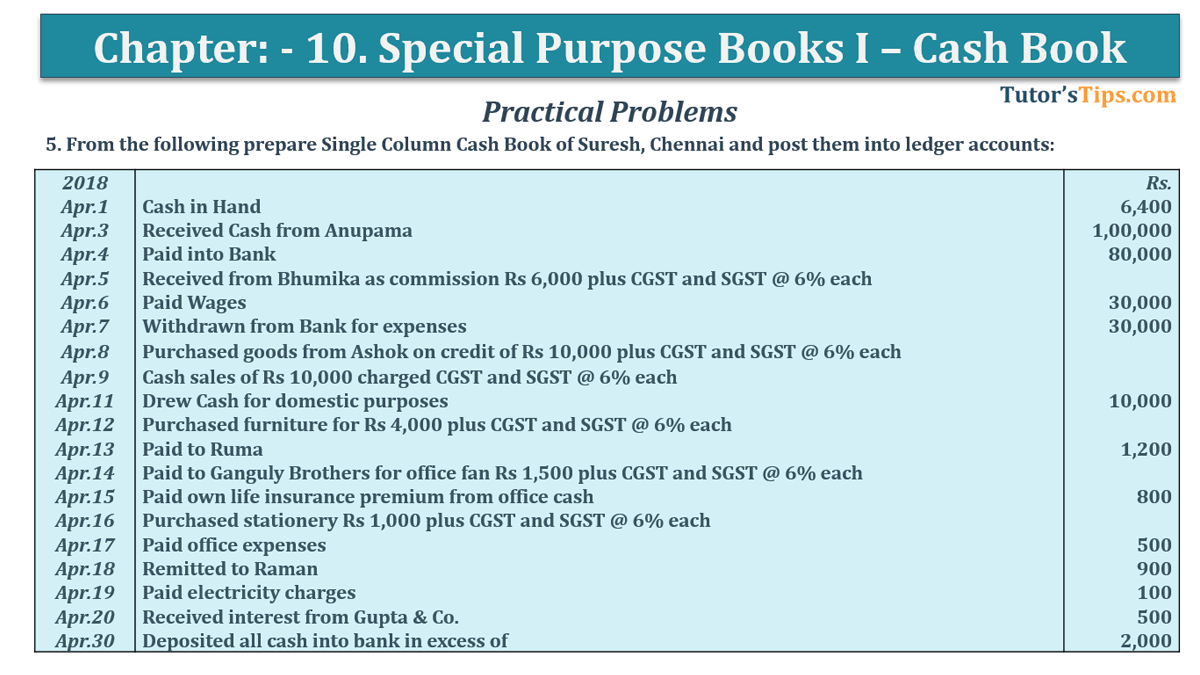

From the following prepare Single Column Cash Book of Suresh, Chennai and post them into ledger accounts:

| 2018 | Rs. | |

| Apr.1 | Cash in Hand | 6,400 |

| Apr.3 | Received Cash from Anupama | 1,00,000 |

| Apr.4 | Paid into Bank | 80,000 |

| Apr.5 | Received from Bhumika as commission Rs 6,000 plus CGST and SGST @ 6% each | |

| Apr.6 | Paid Wages | 30,000 |

| Apr.7 | Withdrawn from Bank for expenses | 30,000 |

| Apr.8 | Purchased goods from Ashok on the credit of Rs 10,000 plus CGST and SGST @ 6% each | |

| Apr.9 | Cash sales of Rs 10,000 charged CGST and SGST @ 6% each | |

| Apr.11 | Drew Cash for domestic purposes | 10,000 |

| Apr.12 | Purchased furniture for Rs 4,000 plus CGST and SGST @ 6% each | |

| Apr.13 | Paid to Ruma | 1,200 |

| Apr.14 | Paid to Ganguly Brothers for office fan Rs 1,500 plus CGST and SGST @ 6% each | |

| Apr.15 | Paid own life insurance premium from office cash | 800 |

| Apr.16 | Purchased stationery Rs 1,000 plus CGST and SGST @ 6% each | |

| Apr.17 | Paid office expenses | 500 |

| Apr.18 | Remitted to Raman | 900 |

| Apr.19 | Paid electricity charges | 100 |

| Apr.20 | Received interest from Gupta & Co. | 500 |

| Apr.30 | Deposited all cash into the bank in excess of | 2,000 |

The solution of Question No 5 Chapter No 10:-

In the Books of Suresh, Chennai

| Dr. | Cash Book | Cr. | |||||

| Date | Particulars |

L.F. | Amount | Date | Particulars |

L.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 1 | To Balance B/d | 6,400 | Apr. 4 | By Bank A/c | 80,000 | ||

| Apr. 3 | To Anupama A/c | 1,00,000 | Apr. 6 | By Wages A/c | 30,000 | ||

| Apr. 5 | To Commission A/c* | 6,000 | Apr. 11 | By Drawing A/c | 1,200 | ||

| Apr. 5 | To Output CGST A/c | 360 | Apr. 12 | By Office Furniture A/c* | 4,000 | ||

| Apr. 5 | To Output SGST A/c | 360 | Apr. 12 | By Input CGST A/c | 240 | ||

| Apr. 7 | To Bank A/c | 30,000 | Apr. 12 | By Input SGST A/c | 240 | ||

| Apr. 9 | To Sales A/c* | 10,000 | Apr. 13 | By Ruma A/c | 1,200 | ||

| Apr. 9 | To Output CGST A/c | 600 | Apr. 14 | By Electric Fitting A/c* | 1,500 | ||

| Apr. 9 | To Output SGST A/c | 600 | Apr. 14 | By Input CGST A/c | 90 | ||

| Apr. 20 | To Interest Received A/c | 500 | Apr. 14 | By Input SGST A/c | 90 | ||

| Apr. 15 | By Drawing A/c | 800 | |||||

| Apr. 16 | By Stationery A/c* | 1,000 | |||||

| Apr. 16 | By Input CGST A/c | 60 | |||||

| Apr. 16 | By Input SGST A/c | 60 | |||||

| Apr. 17 | By Office Expenses A/c | 2,000 | |||||

| Apr. 18 | By Raman A/c | 900 | |||||

| Apr. 19 | By Electricity Charges A/c | 100 | |||||

| Apr. 30 | By Bank A/c (Bal. Fig.) | 22,040 | |||||

| Apr. 30 | By Balance C/d | 2,000 | |||||

| 1,54,820 | 1,54,820 | ||||||

All transactions which are highlighted with (*) are explained as following as follows: –

*Apr.5 Received from Bhumika as commission Rs 6,000 plus CGST and SGST @ 6% each

The calculation of Amount of CGST and SGST @ 6% each.

6,000 * 6% = 360/- each

*Apr.9 Cash sales of Rs 10,000 charged CGST and SGST @ 6% each

The calculation of Amount of CGST and SGST @ 6% each.

10,000 * 6% = 600/- each

*Apr.12 Purchased furniture for Rs 4,000 plus CGST and SGST @ 6% each

The calculation of Amount of CGST and SGST @ 6% each.

4,000 * 6% = 240/- each

*Apr.14 Paid to Ganguly Brothers for office fan Rs 1,500 plus CGST and SGST @ 6% each

The calculation of Amount of CGST and SGST @ 6% each.

1,500 * 6% = 90/- each

*Apr.16 Purchased stationery Rs 1,000 plus CGST and SGST @ 6% each

The calculation of Amount of CGST and SGST @ 6% each.

1,000 * 6% = 60/- each

To understand more about cash book please check out following links: –

Cash Book | Types of Cash Book | Subsidiary Books

Single Column Cash Book | Explained with Example

Double Column Cash Book | Explained with Example

Triple Column Cash Book | Explained with Example

Petty Cash Book | Example | Subsidiary Books

Thanks Please share with your friends

Comment if you have any question.

Also, Check out previous Chapters: –

- Chapter No. 5 – Accounting Equation

- Chapter No. 6 – Accounting Procedures – Rules of Debit and Credit

- Goods and Services Tax(GST)

- Chapter No. 8 – Journal

- Chapter No. 9 – Ledger

Check out T.S. Grewal +1 Book 2019 @ Official Website of Sultan Chand Publication

T.S. Grewal’s Double Entry Book Keeping