Question No 20 Chapter No 4

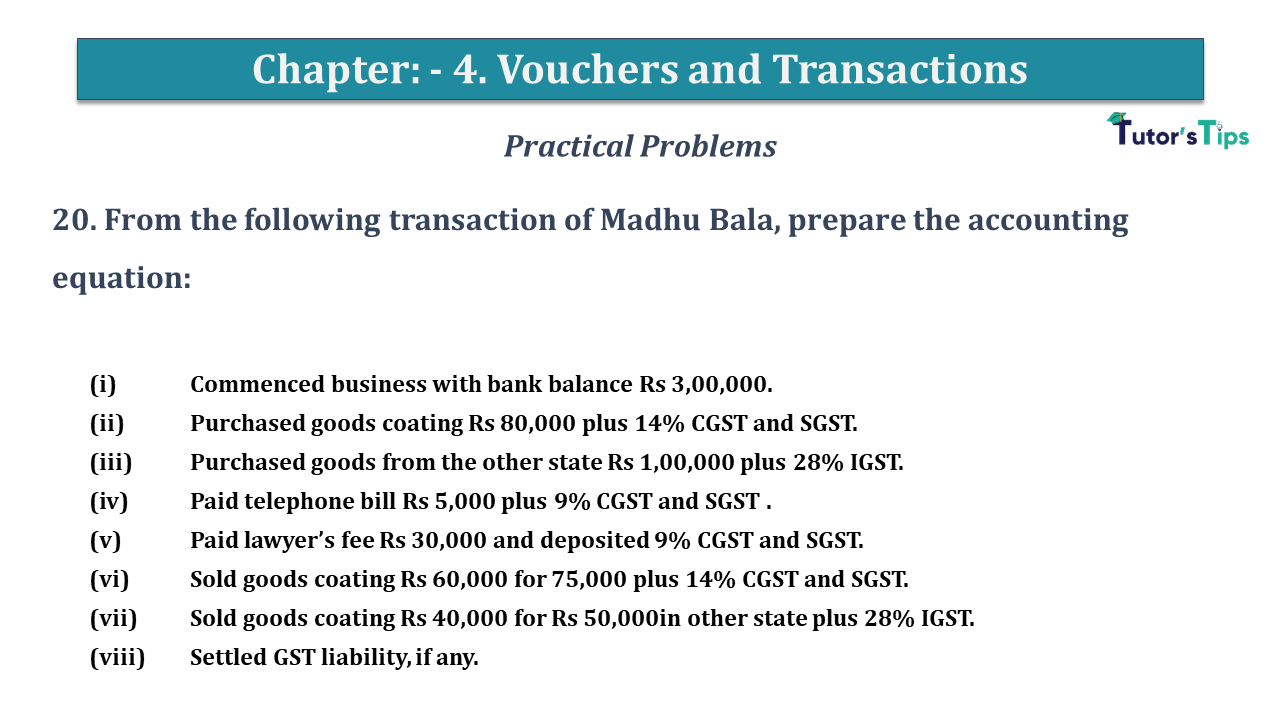

20. From the following transaction of Madhu Bala, prepare the accounting equation:

| (i) | Commenced business with bank balance Rs 3,00,000. |

| (ii) | Purchased goods coating Rs 80,000 plus 14% CGST and SGST. |

| (iii) | Purchased goods from the other state Rs 1,00,000 plus 28% IGST. |

| (iv) | Paid telephone bill Rs 5,000 plus 9% CGST and SGST . |

| (v) | Paid lawyer’s fee Rs 30,000 and deposited 9% CGST and SGST. |

| (vi) | Sold goods coating Rs 60,000 for 75,000 plus 14% CGST and SGST. |

| (vii) | Sold goods coating Rs 40,000 for Rs 50,000in other state plus 28% IGST. |

| (viii) | Settled GST liability, if any. |

The solution of Question No 20 Chapter No 4: –

| S. No. | Particulars | Assets |

||||

| Bank | +Stock | +Input CGST | +Input SGST |

+Input |

||

| i | Commenced business with cash | 3,00,000 | ||||

| 3,00,000 | ||||||

| ii | Purchased goods on credit plus CGST and SGST 14% | -1,02,400 | +80,000 | +11,200 | +11,200 | |

| 1,97,600 | +80,000 | +11,200 | +11,200 | |||

| iii | Purchased goods on cheque plus IGST 28% | -1,28,000 | +1,00,000 | +28,000 | ||

| 69,600 | +1,80,000 | +11,200 | +11,200 | +28,000 | ||

| iv | Paid telephone bill plus CGST and SGST 9% | -5,900 | +450 | +450 | ||

| 63,700 | +1,80,000 | +11,650 | +11,650 | +28,000 | ||

| v | paid to lawyer plus CGST and SGST 9% | -35,400 | +2,700 | +2,700 | ||

| 28,300 | +1,80,000 | +14,350 | +14,350 | +28,000 | ||

| vi | Sold goods on profit plus CGST and SGST 14% | +96,000 | -60,000 | |||

| 1,24,300 | 1,20,000 | +14,350 | +14,350 | +28,000 | ||

| vii | Sold goods on profit plus IGST 28% | +64,000 | -40,000 | |||

| 1,88,300 | + 80,000 | +14,350 | +14,350 | +28,000 | ||

| viii | Settled GST Liability | -10,500 | -10,500 | -14,000 | ||

| Total | 188,300 | + 80,000 |

+3,850 |

+3,850 |

+14,000 | |

| S. No. | Liabilities |

Capital | ||

| +Output CGST |

+Output SGST |

+Output IGST |

||

| i | – | 3,00,000 | ||

| – | 3,00,000 | |||

| ii | – | |||

| 3,00,000 | ||||

| iii | – | |||

| 3,00,000 | ||||

| iv | -5,000 | |||

| 2,95,000 | ||||

| v | -30,000 | |||

| 2,65,000 | ||||

| vi | 10,500 | 10,500 | +15,000 | |

| 10,500 | 10,500 | 2,80,000 | ||

| vii | +14,000 | +10,000 | ||

| 10,500 | 10,500 | +14,000 | 2,90,000 | |

| viii | -10,500 | -10,500 | -14,000 | -4,000 |

| – | – |

– |

2,90,000 | |

Answer: –

Assets = 1,88,300 + 80,000 + 3,850 + 3,850 + 14,000 = 2,90,000/-

Capital = 2,90,000/-

What is Accounting Equation | Example

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of all Chapters: –

Usha Publication – Elements of Book-Keeping PSEB (Class 11) – Solution

Chapter No. 2 – Theory Base of Accounting

Chapter No. 3 – Origin of Transactions

Chapter No. 4 – Vouchers and transactions

Chapter No. 6 – Accounting for Goods and Services Tax(GST)

Chapter No. 9 – Other Subsidiary Books

Chapter No. 10 – Journal Proper

Chapter No. 11 – Trial Balance

Chapter No. 12 – Bank Reconciliation Statement

Chapter No. 14 – Provisions and Reserves

Chapter No. 15 – Bills of Exchange

Chapter No. 16 – Rectification of Errors

Chapter No. 17 – Financial Statements – (Without Adjustments)

Chapter No. 18 – Financial Statements – (With Adjustments)