Question No 18 Chapter No 13

Sale of Total Assets

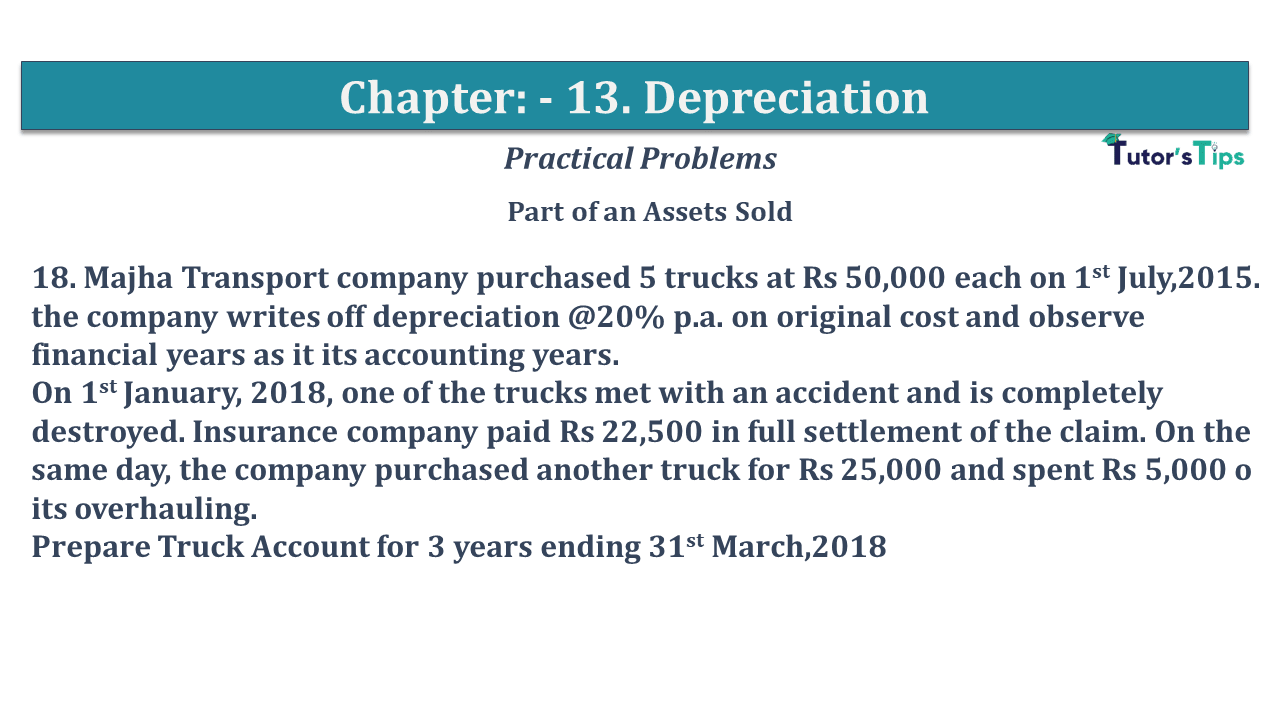

18. Majha Transport company purchased 5 trucks at Rs 50,000 each on 1st July,2015. the company writes off depreciation @20% p.a. on original cost and observe financial years as it its accounting years.

On 1st January, 2018, one of the trucks met with an accident and is completely destroyed. Insurance company paid Rs 22,500 in full settlement of the claim. On the same day, the company purchased another truck for Rs 25,000 and spent Rs 5,000 o its overhauling.

Prepare Truck Account for 3 years ending 31st March,2018

The solution of Question No 18 Chapter No 13:-

| Dr. | Truck A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 01/07/15 | To Cash A/c | 2,50,000 | 31/03/16 | By Deprecation A/c*1 | 37,500 | ||

| 31/03/16 | By Balance C/d | 2,12,500 | |||||

| 2,50,000 | 2,50,000 | ||||||

| 01/04/16 | To Balance b/d | 2,12,500 | 31/03/17 | By Deprecation A/c*2 | 50,000 | ||

| 31/03/17 | By Balance C/d | 1,62,500 | |||||

| 2,12,500 | 2,12,500 | ||||||

| 01/04/17 | To Balance b/d | 1,62,500 | 01/01/18 | By Bank A/c | 22,500 | ||

| 01/01/18 | To Profit/loss A/c | 30,000 | 01/01/18 | By Profit/Loss A/c | 2,500 | ||

| 01/01/18 | By Deprecation A/c | 7,500 | |||||

| 31/03/18 | By Deprecation A/c*3 | 41,500 | |||||

| 31/03/18 | By Balance C/d | 1,18,500 | |||||

| 1,92,500 | 1,92,500 | ||||||

Working note:-

*1:- Calculation of the amount of Depreciation on furniture for the year 2015-16

Machinery purchased on 1st Jul 2015

Depreciation = Value of Asset X Rate of Depreciation X Period

Value of Asset = 2,50,000

Rate of Depreciation = 20%

Period = from 01/07/2015 to 31/03/2016 i.e. 9 months

(from the date of purchase/Beginning balance to the end of the financial year)

= 2,50,000 X 20/100 X 9/ 12

Depreciation = 37,500

Total Depreciation for the year = 37,500

*2:– Calculation of the amount of Depreciation on furniture for year 2016-17

Machinery purchased on 1st Jul 2015

Depreciation = Value of Asset X Rate of Depreciation X Period

Value of Asset = 2,50,000

Rate of Depreciation = 20%

Period = from 01/04/2016 to 31/03/2017 i.e. 9 months

(from the date of purchase/Beginning balance to end of the financial year)

= 2,50,000 X 20/100 X 9/ 12

Depreciation = 50,000

Total Depreciation for the year 50,000

| Statement Showing profit or loss on the sale of Machinery | |

| Particulars |

Amount |

| Purchase value of machinery as on 1st July, 2015 | 50,000 |

| Less: – Amount of Depreciation charged on year 2015-16 | |

| 50,000*10%* 9/12 | 7,500 |

| Amount of Depreciation charged on year 2016-17 | |

| 50,000*10%* 12/12 | 10,000 |

| Amount of Depreciation charged on year 2017-18 | |

| 50,000*10%* 9/12 | 7,500 |

| Book value of the asset as on 1st January 2019 | 25,000 |

| Sale Price of Machinery | 22,500 |

| Loss on the sale of the asset | 2,500 |

*3:- Calculation of the amount of Depreciation on furniture for the year 2017-18

Machinery purchased on 1st Jul 2015

Depreciation = Value of Asset X Rate of Depreciation X Period

Value of Asset = 2,00,000

Rate of Depreciation = 20%

Period = from 01/04/2017 to 31/10/2018 i.e. 12 months

(from the date of purchase/Beginning balance to the end of the financial year)

= 2,00,000 X 20/100 X 12/ 12

Depreciation = 40,000

Machinery purchased on 1st October 2016

Value of Asset = 25,000

Rate of Depreciation = 20%

Period = from 01/01/2017 to 31/03/2017 i.e. 3 months

(from the date of purchase/Beginning balance to end of the financial year)

= 25,000 X 20/100 X 3/ 12

Depreciation =1.250

Total Depreciation for the year = 41,250

Depreciation | Meaning | Methods | Examples

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of all Chapters: –

Chapter No. 2 – Theory Base of Accounting

Chapter No. 3 – Vouchers and transactions

Chapter No. 4 – Journal

Chapter No. 5 – Ledger

Chapter No. 6 – Cash Book

Chapter No. 7 – Other Subsidiary Books

Chapter No. 8 – Journal Proper

Chapter No. 9 – Trial Balance

Chapter No. 10 – Bank Reconciliation Statement

Chapter No. 11 – Depreciation

Chapter No. 12 – Provisions and Reserves

Chapter No. 13 – Bills of Exchange

Chapter No. 14 – Rectification of Errors

Chapter No. 15 – Financial Statements – (Without Adjustments)

Chapter No. 16 – Financial Statements – (With Adjustments)