Question 52 Chapter 6 of +2-A

52. Following is the Balance Sheet of Kusum, Sneh and Usha as on 31st March 2019, who have agreed to share profits and losses in the proportion of their capitals:

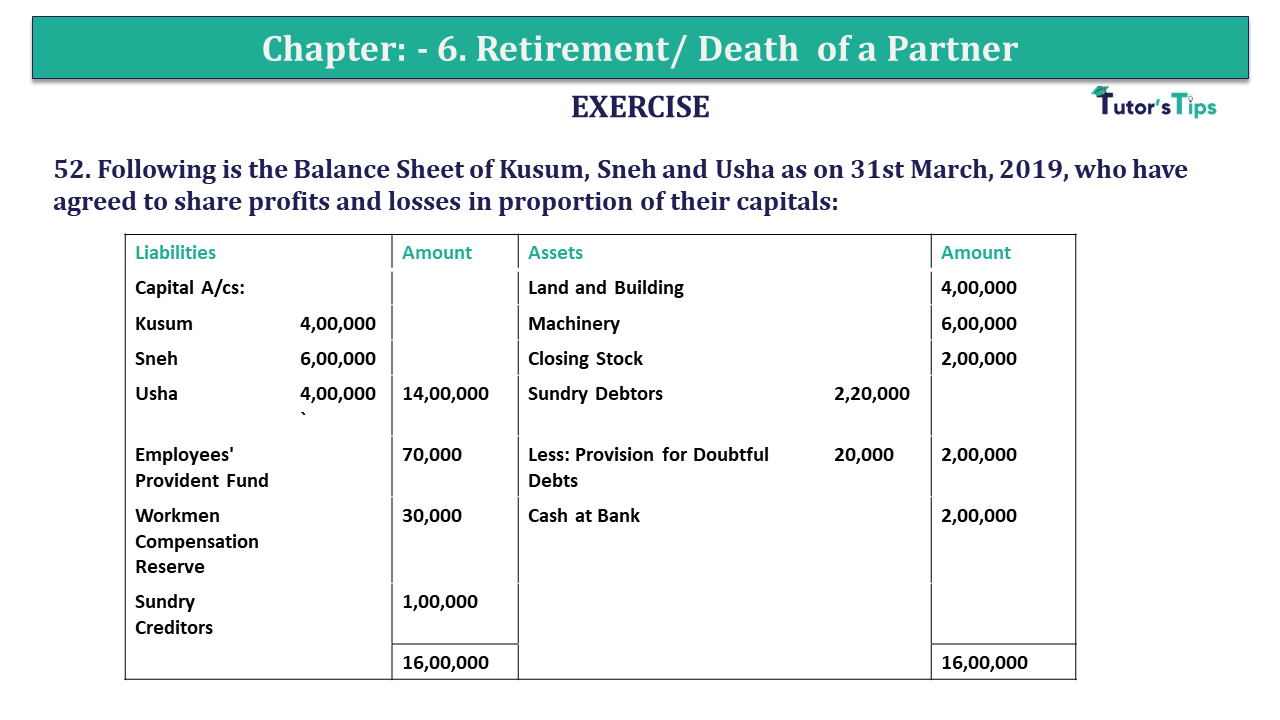

| Liabilities | Amount | Assets | Amount | ||

| Capital A/cs: | Land and Building | 4,00,000 | |||

| Kusum | 4,00,000 | Machinery | 6,00,000 | ||

| Sneh | 6,00,000 | Closing Stock | 2,00,000 | ||

| Usha | 4,00,000` | 14,00,000 | Sundry Debtors | 2,20,000 | |

| Employees’ Provident Fund | 70,000 | Less: Provision for Doubtful Debts | 20,000 | 2,00,000 | |

| Workmen Compensation Reserve | 30,000 | Cash at Bank | 2,00,000 | ||

| Sundry Creditors | 1,00,000 | ||||

| 16,00,000 | 16,00,000 |

On 1st April, 2019, Kusum retired from the firm and the remaining partners decided to carry on the business. It was agreed to revalue the assets and reassess the liabilities on that date, on the following basis:

a Land and Building be appreciated by 30%.

b Machinery be depreciated by 30%.

c There were Bad Debts of 35,000.

d The claim against Workmen Compensation Reserve was estimated at 15,000.

e Goodwill of the firm was valued at 2,80,000 and Kusum’s share of goodwill was adjusted against the Capital Accounts of the continuing partners Sneh and Usha who have decided to share future profits in the ratio of 3 : 4 respectively.

f Capital of the new firm in total will be the same as before the retirement of Kusum and will be in the new profit-sharing ratio of the continuing partners.

g Amount due to Kusum be settled by paying 1,00,000 in cash and balance by transferring to her Loan Account which will be paid later on.

Prepare Revaluation Account, Capital Accounts of Partners and Balance Sheet of the new firm after Kusum’s retirement.

The solution of Question 52 Chapter 6 of +2-A: –

| Revaluation Account |

|||||

| Particular |

Amount | Particular | Amount | ||

| To Machinery A/c | 1,80,000 | By Land and Building A/c | 1,20,000 | ||

| To Bad Debts A/c 35,000 – 20,000 | 15,000 | ||||

| By Loss transferred to: | |||||

| Kusum’s Capital A/c | 21,429 | ||||

| Sneh’s Capital A/c | 32,142 | ||||

| Usha’s Capital A/c | 21,429 | 75,000 | |||

| 1,95,000 | 1,95,000 | ||||

| Partners’ Capital Account |

|||||||

| Part. | Kusum | Sneh | Usha |

Part. |

Kusum | Sneh | Usha |

| To Revaluation A/c | 21,429 | 32,142 | 21,429 | By Balance B/d | 4,00,000 | 6,00,000 | 4,00,000 |

| To Usha’s Capital A/c | – | – | 80,000 | By Work men Compensa tion Fund A/c |

4,286 | 6,428 | 4,286 |

| To Bank A/c | 1,00,000 | – | _ | By Usha’s Capital A/c | 80,000 | – | – |

| To Kusum’s Loan A/c | 3,62,857 | – | – | By C’s Capital A/c | – | 1,833 |

– |

| To Balance c/d | 35,800 | 5,74,286 | 3,02,857 | ||||

| 4,84,286 | 6,06,428 | 4,04,286 | 4,84,286 | 6,06,428 | 4,04,286 | ||

| By Balance b/d | – | 5,74,286 | 3,02,857 | ||||

| To Balance c/d | – | 6,00,000 | 8,00,000 | By Cash A/c | – | 25,714 | 4,97,143 |

| – | 6,00,000 | 8,00,000 | – | 6,00,000 | 8,00,000 | ||

| Balance Sheet |

|||||

| Liabilities |

Amount | Assets | Amount | ||

| Creditors | 1,00,000 | Land & Building | 5,20,000 | ||

| Employee’s Provident Fund | 70,000 | Machinery | 6,00,000 | ||

| Workmen’s Compensation Claim | 15,000 | Less: Deprecition | 1,80,000 | 4,20,000 | |

| Kusum’s Loan | 3,62,857 | Stock | 2,00,000 | ||

| Capital: | Sundry Debtors 2,20,000 – 35,000 | 1,85,000 | |||

| Sneh | 6,00,000 | Bank | 6,22,857 | ||

| Usha | 8,00,000 | 14,00,000 | |||

| 19,47,857 | 19,47,857 | ||||

Working Notes:

Calculation of Profit-Sharing Ratio

Old Ratio Kusum, Sneh and Usha = 2:3:2

New Ratio Sneh and Usha = 3:4

Gaining Ratio = New Ratio – Old Ratio

Gaining Ratio = 3 : 1

| Sneh’s Gain | = | 3 | – | 3 |

| 7 | 7 | |||

| = | Nil |

| Usha’s Gain | = | 4 | – | 2 |

| 7 | 7 | |||

| = | 2 | |||

| 7 |

Adjustment of Goodwill

Total Goodwill of the Firm = 2,80,000

| Kusum’s Share of Goodwill | = | 2,80,000 | X | 2 |

| 7 | ||||

| = | Rs 80,000 |

It is to be adjusted by the Gaining partners i.e. only by Usha

Adjustment of Capital

Total Capital of Firm before Kusum’s Retirement = 14,00,000

New Ratio = 3:4

| Sneh’s Share of Goodwill | = | 14,00,000 | X | 3 |

| 7 | ||||

| = | Rs 6,00,000 |

| Usha’s Share of Goodwill | = | 14,00,000 | X | 4 |

| 7 | ||||

| = | Rs 8,00,000 |

| Balance Sheet |

|||

| Liabilities |

Sneh | Usha | |

| New Capital Balance | 6,00,000 | 8,00,000 | |

| Adjusted Old Capital Balance | 5,74,286 | 3,02,857 | |

| Cash brought in by the Partner | 25,7144 | 4,97,143 | |

| Cash Account |

|||||

| Particulars |

Amount | Particulars | Amount | ||

| Balance b/d | 2,00,000 | Kusum’s Capital A/c | 1,00,000 | ||

| Sneh’s Capital A/c | 25,714 | ||||

| Usha’s Capital A/c | 4,97,143 | ||||

| Balance c/d | 6,22,857 | ||||

| 7,22,857 | 7,22,857 | ||||

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication