Question 38 Chapter 7 of +2-A

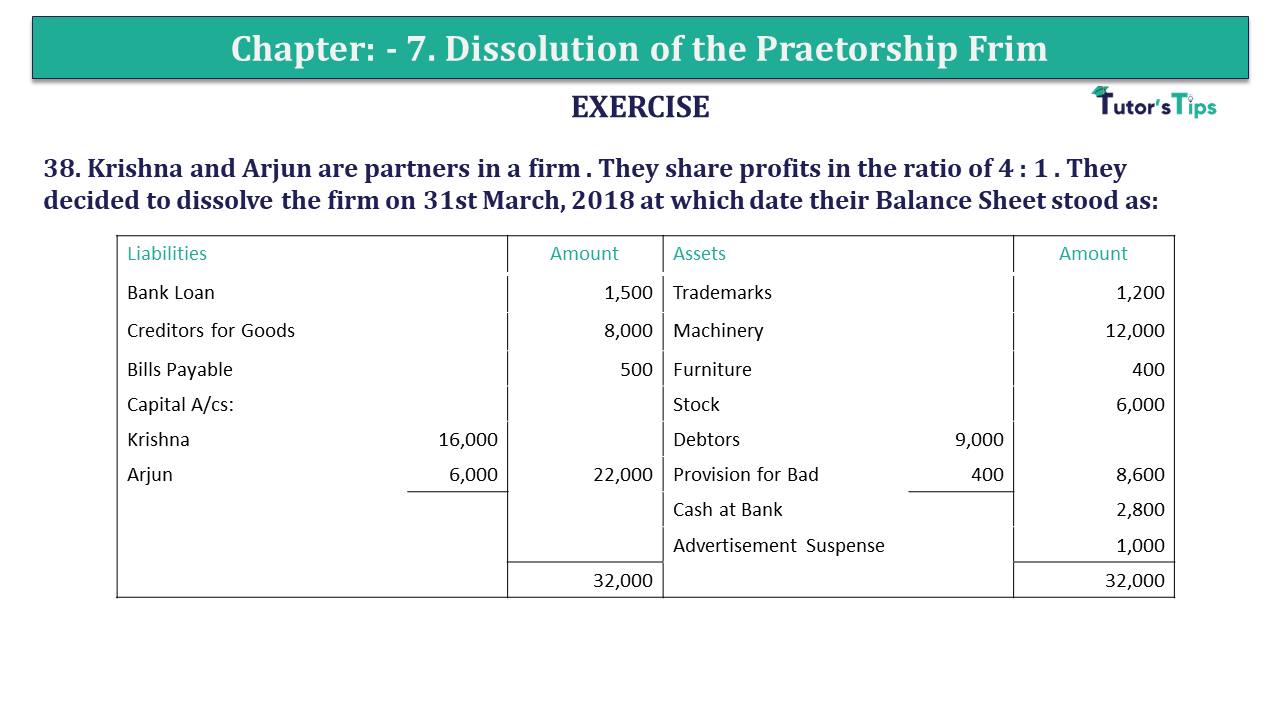

38. Krishna and Arjun are partners in a firm. They share profits in the ratio of 4: 1. They decided to dissolve the firm on 31st March 2018 at which date their Balance Sheet stood as:

| Liabilities | Amount | Assets | Amount | ||

| Bank Loan | 1,500 | Trademarks | 1,200 | ||

| Creditors for Goods | 8,000 | Machinery | 12,000 | ||

| Bills Payable | 500 | Furniture | 400 | ||

| Capital A/cs: | Stock | 6,000 | |||

| Krishna | 16,000 | Debtors | 9,000 | ||

| Arjun | 6,000 | 22,000 | Provision for Bad | 400 | 8,600 |

| Cash at Bank | 2,800 | ||||

| Advertisement Suspense | 1,000 | ||||

| 32,000 | 32,000 |

The realization shows the following results:

a Goodwill was sold for 1,000.

b Debtors were realized at book value less 10%.

c Trademarks were realized for 800.

d Machinery and Stock-in-Trade were taken over by Krishna for 14,400 and 3,600 respectively.

e An unrecorded asset estimated at 500 was sold for 200.

f Creditors for goods were settled at a discount of 80. The expenses on realization were 800.

Prepare Realization Account, Partners’ Capital Accounts and Bank Account.

The solution of Question 38 Chapter 7 of +2-A: –

| Realization Account |

|||||

| Particular |

Amount | Particular | Amount | ||

| Trade Marks | 1,200 | Provision for Doubtful Debts | 3,000 | ||

| Machinery | 12,000 | Bank Loan | 45,000 | ||

| Furniture | 400 | Creditors for Goods | 12,000 | ||

| Stock | 6,000 | Bills Payable | 7,500 | ||

| Debtors | 9,000 | ||||

| Bank A/c: | |||||

| Bank A/c :- | Goodwill | 1,000 | |||

| Bank Loan | 1,500 | Debtors | 8,100 | ||

| Creditors | 7,920 | Trade Marks | 800 | ||

| Bills Payable | 500 | Unrecorded Assets | 2000 | 10,100 | |

| Expense | 800 | Krishna’s Capital A/c: | |||

| Machinery | 14,400 | ||||

| Stock in Trade | 3,600 | 18,000 | |||

| Loss on Revaluation | |||||

| Krishna’s Capital A/c | 656 | ||||

| Arjun’s Capital A/c | 164 | 820 | |||

| 39,320 | 39,320 | ||||

| Partners’ Capital Account |

|||||

| Part. | Krishna | Arjun |

Part. |

Krishna | Arjun |

| To Advertisement Suspense A/c | 800 | 200 | By Balance B/d | 16,000 | 6,000 |

| To Realization A/c Assets | 18,000 | – | By Realization A/c | 38,000 | – |

| To Realization A/c Loss | 656 | 164 | |||

| To Cash A/c | 5,363 | By cash A/c | 3,456 | ||

| 19,456 | 6,000 | 19,456 | 6,000 | ||

| Bank Account |

|||||

| Particular |

Amount | Particular | Amount | ||

| Balance b/d | 2,800 | Realization A/c | 10,720 | ||

| Krishna’s Capital A/c | 10,100 | Arjun’s Capital A/c | 5,636 | ||

| Realization A/c | 3,456 | ||||

| 16,356 | 16,356 | ||||

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication