Question 16 Chapter 7 of +2-A

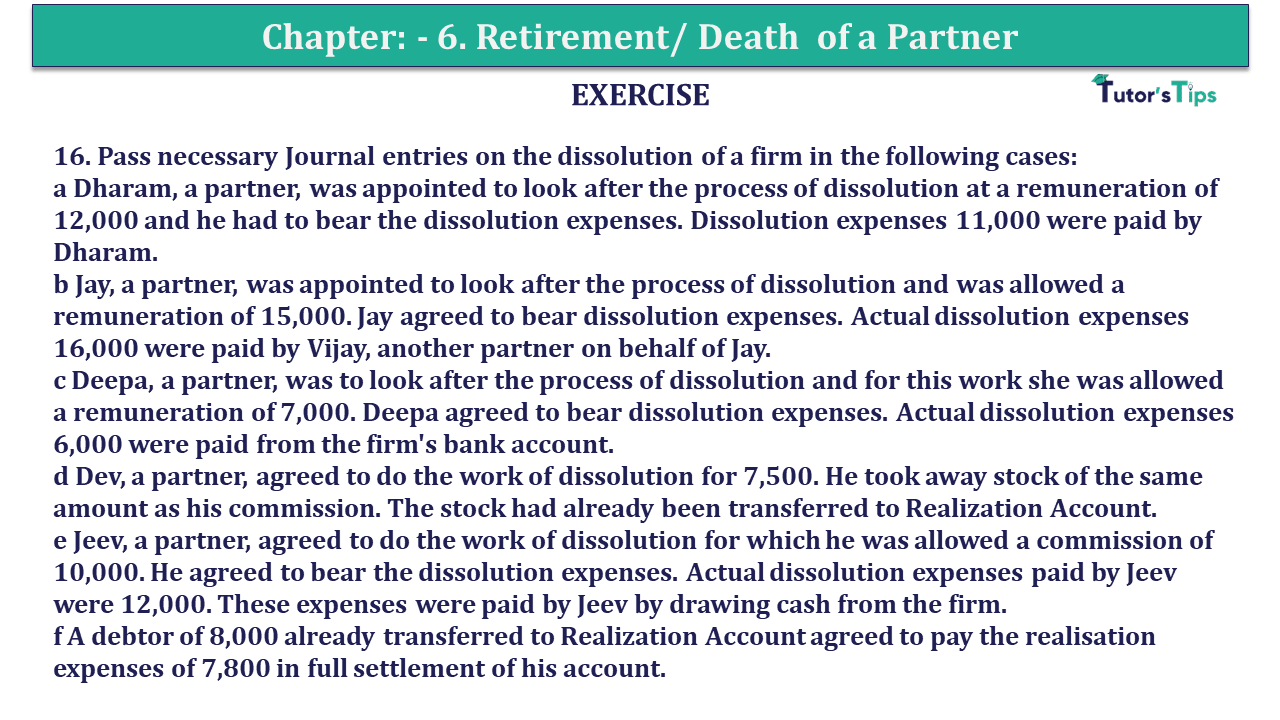

16. Pass necessary Journal entries on the dissolution of a firm in the following cases:

a Dharam, a partner, was appointed to look after the process of dissolution at a remuneration of 12,000 and he had to bear the dissolution expenses. Dissolution expenses 11,000 were paid by Dharam.

b Jay, a partner, was appointed to look after the process of dissolution and was allowed a remuneration of 15,000. Jay agreed to bear dissolution expenses. Actual dissolution expenses 16,000 were paid by Vijay, another partner on behalf of Jay.

c Deepa, a partner, was to look after the process of dissolution and for this work she was allowed a remuneration of 7,000. Deepa agreed to bear dissolution expenses. Actual dissolution expenses 6,000 were paid from the firm’s bank account.

d Dev, a partner, agreed to do the work of dissolution for 7,500. He took away stock of the same amount as his commission. The stock had already been transferred to Realization Account.

e Jeev, a partner, agreed to do the work of dissolution for which he was allowed a commission of 10,000. He agreed to bear the dissolution expenses. Actual dissolution expenses paid by Jeev were 12,000. These expenses were paid by Jeev by drawing cash from the firm.

f A debtor of 8,000 already transferred to Realization Account agreed to pay the realisation expenses of 7,800 in full settlement of his account.

The solution of Question 16 Chapter 7 of +2-A: –

| Date | Particulars |

L.F. | Debit | Credit | |

| a | Realization A/c | Dr. | 12,000 | ||

| To Dharam’s Capital A/c | 12,000 | ||||

| (Being Remuneration paid) | |||||

| b | Realization A/c | Dr. | 2,500 | ||

| To Jay’s’s Capital A/c | 2,500 | ||||

| (Being Liability discharged ) | |||||

| Jay’s Capital A/c | Dr. | 16,000 | |||

| To Vijay’s Capital A/c | 16,000 | ||||

| (Being Expenses borne by Jay, paid by Vijay) | |||||

| c | Realization A/c | Dr. | 7,000 | ||

| To Deepa’s Capital A/c | 7,000 | ||||

| ( Being Remuneration paid) | |||||

| Deepa’s Capital A/c | Dr. | 6,000 | |||

| To Bank A/c | 6,000 | ||||

| (Being Expenses paid by firm) | |||||

| d | No Entry | ||||

| e | Realization A/c | Dr. | 10,000 | ||

| To Jeev’s Capital A/c | 10,000 | ||||

| (Being Remuneration paid) | |||||

| Jeev’s Capital A/c | Dr. | 12,000 | |||

| To Jeev’s Capital A/c | 12,000 | ||||

| (Being Expenses paid by firm) | |||||

| f | No Entry | ||||

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication