Question 13 Chapter 6 – Unimax

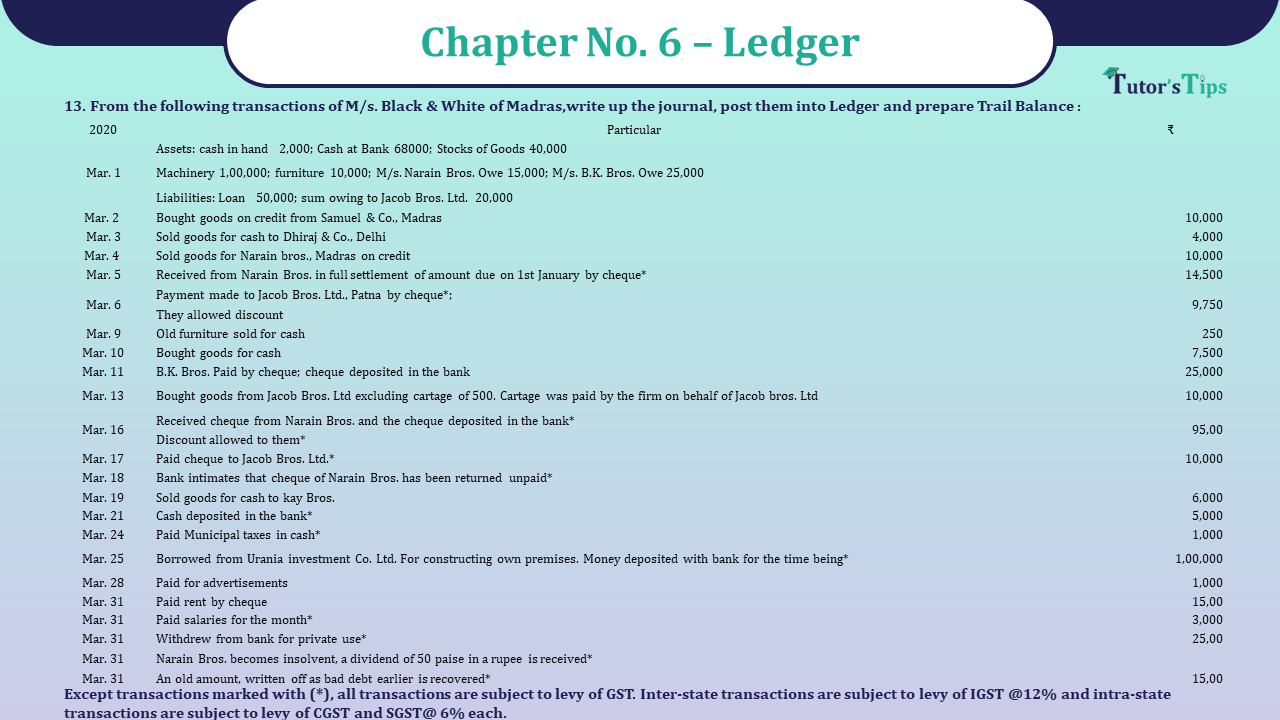

Question 13. From the following transactions of M/s. Black & White of Madras,write up the journal, post them into Ledger and prepare Trail Balance :

| 2020 | Particular | ₹ |

| Mar. 1 | Assets: cash in hand 2,000; Cash at Bank 68000; Stocks of Goods 40,000 | |

| Machinery 1,00,000; furniture 10,000; M/s. Narain Bros. Owe 15,000; M/s. B.K. Bros. Owe 25,000 | ||

| Liabilities: Loan 50,000; sum owing to Jacob Bros. Ltd. 20,000 | ||

| Mar. 2 | Bought goods on credit from Samuel & Co., Madras | 10,000 |

| Mar. 3 | Sold goods for cash to Dhiraj & Co., Delhi | 4,000 |

| Mar. 4 | Sold goods for Narain bros., Madras on credit | 10,000 |

| Mar. 5 | Received from Narain Bros. in full settlement of amount due on 1st January by cheque* | 14,500 |

| Mar. 6 | Payment made to Jacob Bros. Ltd., Patna by cheque*; | 9,750 |

| They allowed discount | ||

| Mar. 9 | Old furniture sold for cash | 250 |

| Mar. 10 | Bought goods for cash | 7,500 |

| Mar. 11 | B.K. Bros. Paid by cheque; cheque deposited in the bank | 25,000 |

| Mar. 13 | Bought goods from Jacob Bros. Ltd excluding cartage of 500. Cartage was paid by the firm on behalf of Jacob bros. Ltd | 10,000 |

| Mar. 16 | Received cheque from Narain Bros. and the cheque deposited in the bank* | 95,00 |

| Discount allowed to them* | ||

| Mar. 17 | Paid cheque to Jacob Bros. Ltd.* | 10,000 |

| Mar. 18 | Bank intimates that cheque of Narain Bros. has been returned unpaid* | |

| Mar. 19 | Sold goods for cash to kay Bros. | 6,000 |

| Mar. 21 | Cash deposited in the bank* | 5,000 |

| Mar. 24 | Paid Municipal taxes in cash* | 1,000 |

| Mar. 25 | Borrowed from Urania investment Co. Ltd. For constructing own premises. Money deposited with bank for the time being* | 1,00,000 |

| Mar. 28 | Paid for advertisements | 1,000 |

| Mar. 31 | Paid rent by cheque | 15,00 |

| Mar. 31 | Paid salaries for the month* | 3,000 |

| Mar. 31 | Withdrew from bank for private use* | 25,00 |

| Mar. 31 | Narain Bros. becomes insolvent, a dividend of 50 paise in a rupee is received* | |

| Mar. 31 | An old amount, written off as bad debt earlier is recovered* | 15,00 |

Except transactions marked with (*), all transactions are subject to levy of GST. Inter-state transactions are subject to levy of IGST @12% and intra-state transactions are subject to levy of CGST and SGST@ 6% each.

The solution of Question 13 Chapter 6 – Unimax:

IN THE BOOKS OF KAMAL, DELHI JOURNAL

Journal

| Date | Particular | L.F. | Dr. | Cr. | |

| 2020 | Cash A/c | Dr. | 2 | 2,000 | |

| Mar. 1 | Stock A/c | Dr. | 4 | 40,000 | |

| Machinery A/c | Dr. | 5 | 1,00,000 | ||

| Furniture A/c | Dr. | 6 | 10,000 | ||

| M/s Narain bros. | Dr. | 7 | 15,000 | ||

| M/s. B.K. Bros. | Dr. | 8 | 25,000 | ||

| To Loan A/c | 9 | 50,000 | |||

| To Jacob Bros. Ltd. | 10 | 20,000 | |||

| To Captial A/c (Balancing Amount) | 1 | 1,90,000 | |||

| (Being the assets and liabilities brought forward from last year, capital found by deducting liabilities from assets 9i.e., 2,60,000- 70,0000) | |||||

| Mar. 2 | Purchases A/c | Dr. | 4 | 10,000 | |

| Input CGST A/c | Dr. | 24 | 600 | ||

| Input SGST A/c | Dr. | 24 | 600 | ||

| To Samuel & Co. | 11 | 11,200 | |||

| (Being the intra-state Purchase of goods from Samuel & Co., Payable CGST and SGST @ 6% each) | |||||

| Mar. 3 | Cash A/c | Dr. | 2 | 4,480 | |

| To Sale A/c | 4 | 4,000 | |||

| To Output IGST A/c | 25 | 480 | |||

| (Being the intra-state Sale of goods for cash to Dhiraj & Co., charged IGST @ 12% each) | |||||

| Mar. 4 | Narain Bros. | Dr. | 7 | 11,200 | |

| To sales A/c | 4 | 10,000 | |||

| To Output CGST A/c | 25 | 600 | |||

| To Output SGST A/c | 25 | 600 | |||

| (Being the Intra-State of goods to Narain & Bros., charged CGST and SGST @ 6% each) | |||||

| Mar. 5 | Cash A/c | Dr. | 3 | 14,500 | |

| Discount allowed A/c | Dr. | 13 | 500 | ||

| To Narain Bros. | 7 | 15,000 | |||

| (Being the amount of 14,000 received in payment for a debt of 15,000; discount allowed 500 | |||||

| Mar. 6 | Jacob Bros. Ltd. A/c | Dr. | 10 | 10,000 | |

| To Bank A/c | 3 | 9,750 | |||

| To Discount Received A/c | 14 | 250 | |||

| (Being the amount paid by cheque to Jacob Bros. Ltd. Patna who allowed discount of ₹ 250) | |||||

| Mar. 9 | Cash A/c | Dr. | 2 | 1,120 | |

| To FurnitureA/c | 6 | 1,000 | |||

| To Output CGST A/c | 25 | 60 | |||

| To Output SGST A/c | 25 | 60 | |||

| (Being the sale of (Ai furniture, the payment received in cash charged CGST and SGST 0 6% each) | |||||

| Mar. 10 | Purchases A/c | Dr. | 4 | 7,500 | |

| Input CGST A/c | Dr. | 24 | 450 | ||

| Input SGST A/c | Dr. | 24 | 450 | ||

| To Cash A/c | 2 | 8,400 | |||

| (Being the intra-State purchase of goods for cash, paid CGST and SGST@ 6% each) | |||||

| Mar. 11 | Bank A/c | Dr. | 3 | 25,000 | |

| To B.K. Bros. | 8 | 25,000 | |||

| (Being the cheque received from B.K. Bros. and deposited in Bank) | |||||

| Mar. 11 | Repairs A/c | Dr. | 15 | 1,000 | |

| Input CGST A/c | Dr. | 60 | |||

| Input SGST A/c | Dr. | 60 | |||

| To Cash A/c | 2 | 1,120 | |||

| (Being the amount of repairs of machinery, paid CGST and SGST @ 6% each) | |||||

| Mar. 13 | Purchases A/c | Dr. | 4 | 10,000 | |

| Input IGST A/c | Dr. | 25 | 1,200 | ||

| To Jacob Bros. Ltd. | 10 | 11,200 | |||

| (Being the inter-state purchase of goods from Jacob Bros. Ltd. plus IGST @ 12%) | |||||

| Mar. 13 | Jacob Bros. Ltd. | Dr. | 16 | 500 | |

| To Cash A/c | 2 | 500 | |||

| (Being the cartage on goods paid on behalf of Jacob Bros. Ltd.) | |||||

| Mar. 16 | Bank A/c | Dr. | 3 | 9,500 | |

| Discount Allowed A/c | Dr. | 13 | 500 | ||

| To Narain Bros. | 7 | 10,000 | |||

| (Being the cheque received and deposited in Bank; discount allowed 500) | |||||

| Mar. 17 | Jacob Bros. Ltd. | Dr. | 10 | 10,000 | |

| To Bank A/c | 3 | 10,000 | |||

| (Being the amount paid by cheque to Jacob Bros. Ltd.) | |||||

| Mar. 18 | Narain Bros. | Dr. | 7 | 10,000 | |

| To Bank A/c | 3 | 9,500 | |||

| To Discount Allowed A/c | 13 | 500 | |||

| (Being the cheque received from Narain Bros. returned dishonoured) (Note 2) | |||||

| Mar. 19 | Cash A/c | Dr. | 6,720 | ||

| To Sales A/c | 6,000 | ||||

| To Output CGST A/c | 360 | ||||

| To Output SGST A/c | 360 | ||||

| (Being the intra-state sale of goods cash, charged CGST and SGST @ 6% each) | |||||

| Mar. 21 | Bank A/c | Dr. | 5,000 | ||

| To Cash A/c | 5,000 | ||||

| (Being the cash deposited in the bank) | |||||

| Mar. 24 | Municipal Taxes A/c | Dr. | 1,000 | ||

| To Cash A/c | 1,000 | ||||

| (Being the amount paid as tax) | |||||

| Mar. 25 | Bank A/c | Dr. | 1,00,000 | ||

| To Loan A/c | 1,00,000 | ||||

| (Being the amount borrowed from Urania Investment Co. Ltd.) | |||||

| Mar. 28 | Advertisement A/c | Dr. | 1,000 | ||

| Input CGST A/c | Dr. | 60 | |||

| Input SGST A/c | Dr. | 60 | |||

| To Cash A/c | 1,120 | ||||

| (Being the payment for advertisements, paid CGST and SGST @ 6% each) | |||||

| Mar. 31 | Rent A/c | Dr. | 1,500 | ||

| Input CGST A/c | Dr. | 90 | |||

| Input SGST A/c | Dr. | 90 | |||

| To Bank A/c | 1,680 | ||||

| (Being the rent paid along with CGST and SGST @ 6% each) | |||||

| Mar. 31 | Salaries A/c | Dr. | 3,000 | ||

| To Cash A/c | 3,000 | ||||

| (Being the salaries paid for the month) | |||||

| Mar. 31 | Drawings A/c | Dr. | 2,500 | ||

| To Bank a/c | 2,500 | ||||

| (Being the amount drawn out of bank by the proprietor for private use) | |||||

| Mar. 31 | Cash A/c | Dr. | 5,600 | ||

| Bad Debts A/c | Dr. | 5,600 | |||

| To Narain Bros. | 11,200 | ||||

| (Being half the sum due from Narain Bros. received in cash and the other half written off as being irrecoverable) | |||||

| Mar. 31 | Cash A/c | Dr. | 1,500 | ||

| To Bad Debts Recovered A/c | 1,500 | ||||

| (Being the sum previously treated as bad debts, now recovered—it is a gain) | |||||

| Total | 5,22,940 | 5,22,940 | |||

LEDGER :

CASH ACCOUNT

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 1 | To Balance b/d | 11 | 2,000 | Mar. 10 | By Purchases A/c | 11 | 7,500 |

| Mar. 3 | To Sales A/c | 11 | 4,000 | Mar. 10 | By Input CGST A/C | 11 | 450 |

| Mar. 3 | To Output IGST A/c | 11 | 480 | Mar. 10 | By Input SGST A/C | 11 | 450 |

| Mar. 5 | To Narain bros. A/c | 12 | 14,500 | Mar. 11 | By Repairs A/C | 12 | 1,000 |

| Mar. 9 | To Furniture A/c | 12 | 1,000 | Mar. 11 | By Input CGST A/C | 12 | 60 |

| Mar. 9 | To Output CGST A/c | 12 | 60 | Mar. 11 | By Input SGST A/C | 12 | 60 |

| Mar. 9 | To Output SGST A/c | 12 | 60 | Mar. 13 | By Jacobs Bros. Ltd. | 12 | 500 |

| Mar. 19 | To Sales A/c | 13 | 6,000 | Mar. 21 | By Bank A/c | 13 | 5,000 |

| Mar. 19 | To Output CGST A/c | 13 | 360 | Mar. 24 | By Municipal Taxes A/c | 13 | 1,000 |

| Mar. 19 | To Output SGST A/c | 13 | 360 | Mar. 28 | By Advertisement A/c | 13 | 1,000 |

| Mar. 31 | To Narain Bros. | 13 | 5,600 | Mar. 28 | By Input CGST A/C | 13 | 60 |

| Mar. 31 | To Bad Debts Recovered A/c | 13 | 1,500 | Mar. 28 | By Input SGST A/C | 13 | 60 |

| Mar. 31 | By Salaries A/c | 13 | 3,000 | ||||

| Mar. 31 | By Balance c/d | 13 | 15,780 | ||||

| 35,920 | 35,920 | ||||||

| Apr. 1 | To Balance b/d | 15,780 |

CAPITAL ACCOUNT

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 31 | To Balance c/d | 1,90,000 | Mar. 1 | By Balance b/d | 11 | 1,90,000 | |

| 1,90,000 | 1,90,000 | ||||||

| Apr. 1 | By Balance b/d | 1,90,000 |

DRAWINGS ACCOUNT

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 31 | To Bank A/c | 13 | 2,500 | Mar. 31 | By Balance c/d | 2,500 | |

| 2,500 | 2,500 | ||||||

| Apr. 1 | To Balance b/d | 2,500 |

BANK ACCOUNT

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 1 | To Balance b/d | 68000 | Mar. 6 | By Jacob Bros. Ltd. | 12 | 9,750 | |

| Mar. 11 | To B.K. Bros. | 25,000 | Mar. 17 | By Jacob Bros. Ltd. | 12 | 10,000 | |

| Mar. 16 | To Narain Bros. | 9,500 | Mar. 18 | By Narain Bros. | 13 | 9,500 | |

| Mar. 21 | To Cash A/c | 5,000 | Mar. 31 | By Rent A/c | 13 | 1,500 | |

| Mar. 25 | To Loan A/c | 1,00,000 | Mar. 31 | By Input CGST A/c | 13 | 90 | |

| Mar. 31 | By Input SGST A/c | 13 | 90 | ||||

| Mar. 31 | By Drawings A/c | 13 | 2,500 | ||||

| Mar. 31 | By balance c/d | 13 | 1,74,070 | ||||

| 2,07,500 | 2,07,500 | ||||||

| Apr. 1 | To Balance b/d | 1,74,070 |

MACHINERY ACCOUNT

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 1 | To Balance b/d | 11 | 1,00,00 | Mar. 31 | By Balance c/d | 1,00,000 | |

| 1,00,000 | 1,00,000 | ||||||

| Apr. 1 | To Balance b/d | 1,00,000 |

Furniture Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 1 | To Balance b/d | 11 | 10,000 | Mar. 1 | By Cash A/c | 1,000 | |

| Mar. 31 | By Balance c/d | 9,000 | |||||

| 10,000 | 10,000 | ||||||

| Apr. 1 | To Balance b/d | 9,000 |

Stock Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 1 | To Balance b/d | 11 | 40,000 | ||||

| Mar. 31 | By Balance c/d | 40,000 | |||||

| 40,000 | 40,000 | ||||||

| Apr. 1 | To Balance b/d | 40,000 |

Purchases Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 2 | To Samuel & Co. | 11 | 10,000 | ||||

| Mar. 10 | To Cash A/c | 12 | 7,500 | ||||

| Mar. 13 | To Jacob bros. Ltd. | 12 | 10,000 | Mar. 31 | By Balance c/d | 27,500 | |

| 27,500 | 27,500 | ||||||

| Apr. 1 | To Balance b/d | 27,500 |

Sales Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 31 | To Balance c/d | 20,000 | Mar. 3 | By Cash A/c | 11 | 4,000 | |

| Mar. 4 | By Narain Bros. A/c | 11 | 10,000 | ||||

| Mar. 19 | By Balance c/d | 13 | 6,000 | ||||

| 20,000 | 20,000 | ||||||

| Apr. 1 | By Balance b/d | 20,000 |

M/S. Narain Bros. Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 1 | To Balance b/d | 11 | 15,000 | Mar. | By Cash A/c | 11 | 14,500 |

| Mar. 4 | To Sales A/c | 11 | 10,000 | Mar. | By Discount Allowed A/c | 11 | 500 |

| Mar. 4 | To Output CGST A/c | 11 | 600 | Mar. | By Bank A/c | 13 | 9,500 |

| Mar. 4 | To Output SGST A/c | 11 | 600 | Mar. | By Discount Allowed A/c | 500 | |

| Mar. 18 | To Bank A/c | 13 | 9,500 | Mar. | By Cash A/c | 5,600 | |

| Mar. 18 | To Discount Allowed A/c | 500 | Mar. | By Bad Debts A/c | 5,600 | ||

| 36,200 | 36,200 | ||||||

| Apr. 1 | By Balance b/d | 20,000 |

M/S. B.K. Bros. Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 1 | To Balance b/d | 11 | 25,000 | Mar. 11 | By Bank A/c | 12 | 25,000 |

| 36,200 | 25,000 | ||||||

Loan Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 31 | To Balance c/d | 1,50,000 | Mar. 11 | By Balance b/d | 1 | 50,000 | |

| Mar. 25 | By Bank A/c | 13 | 1,00,000 | ||||

| 1,50,000 | 1,50,000 | ||||||

| Apr. 1 | By balance b/d | 1,50,000 |

Jacob Bros. Ltd. Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 6 | To Bank A/c | 12 | 9,750 | Mar. 1 | By Balance b/d | 1 | 20,000 |

| Mar. 6 | To Discount Received A/c | 12 | 250 | Mar. 13 | By Purchases A/c | 12 | 10,000 |

| Mar. 13 | To Cash A/c | 12 | 500 | Mar. 13 | By Input IGST A/c | 12 | 1,200 |

| Mar. 17 | To Bank A/c | 12 | 10,000 | ||||

| Mar. 31 | To Balance c/d | 10,700 | |||||

| 31,200 | 31,200 | ||||||

| Apr. 1 | By balance b/d | 10,700 |

Samuel & Co. Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 2 | By Purchases A/c | 11 | 10,000 | ||||

| Mar. 2 | By Input CGST A/c | 11 | 600 | ||||

| Mar. 2 | By Input SGST A/c | 11 | 600 | ||||

| Mar. 31 | To Balance c/d | 11,200 | |||||

| 11,200 | 11,200 | ||||||

| Apr. 1 | By Balance b/d | 11,200 |

Discount Allowed Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 5 | To Narain Bros. A/c | 500 | Mar. 2 | By Narain Bros. A/c | 11 | 500 | |

| To Narain Bros. A/c | 500 | Mar. 2 | By Balance c/d | 11 | 500 | ||

| 1,000 | 1,000 | ||||||

| Apr. 1 | To Balance b/d | 500 |

Discount Received Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 31 | To Balance c/d | 250 | Mar. 6 | By Jacob Bros. A/c | 12 | 250 | |

| 250 | 250 | ||||||

| Apr. 1 | By Balance b/d | 250 |

Repairs Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 11 | To Cash A/c | 12 | 1,000 | Mar. 6 | By Balance c/d | 1,000 | |

| 1,000 | 1,000 | ||||||

| Apr. 1 | To Balance b/d | 1,000 |

Municipal Tax Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 11 | To Cash A/c | 13 | 1,000 | Mar. 31 | By Balance c/d | 1,000 | |

| 1,000 | 1,000 | ||||||

| Apr. 1 | To Balance b/d | 1,000 |

Advertisement Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 28 | To Cash A/c | 13 | 1,000 | Mar. 31 | By Balance c/d | 1,000 | |

| 1,000 | 1,000 | ||||||

| Apr. 1 | To Balance b/d | 1,000 |

Rent Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 31 | To Bank A/c | 13 | 1,500 | Mar. 31 | By Balance c/d | 1,500 | |

| 1,500 | 1,500 | ||||||

| Apr. 1 | To Balance b/d | 1,500 |

Salaries Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 31 | To Bank A/c | 13 | 3,000 | Mar. 31 | By Balance c/d | 3,000 | |

| 3,000 | 3,000 | ||||||

| Apr. 1 | To Balance b/d | 3,000 |

Bad Debts Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 31 | To Narain Bros. A/c | 13 | 5,600 | Mar. 31 | By Balance c/d | 5,600 | |

| 5,600 | 5,600 | ||||||

| Apr. 1 | To Balance b/d | 5,600 |

Bad Debts Recovered Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 31 | By Cash A/c | 13 | 1,500 | ||||

| Mar. 31 | By Balance c/d | 1,500 | |||||

| 1,500 | 1,500 | ||||||

| Apr. 1 | By Balance b/d | 1,500 |

Input CGST Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 2 | To Samuel & Co. (Purchase) | 11 | 600 | Mar. 31 | By Balance c/d | 13 | 1,260 |

| Mar. 10 | To Cash A/c (Purchase) | 11 | 450 | ||||

| Mar. 11 | To Cash A/c (Repairs) | 12 | 60 | ||||

| Mar. 28 | To Cash A/c (Advertisement) | 13 | 60 | ||||

| Mar. 31 | To Bank A/c (Rent) | 13 | 90 | ||||

| 1,260 | 1,260 |

Input SGST Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 2 | To Samuel & Co. (Purchase) | 11 | 600 | Mar. 31 | By Balance c/d | 13 | 1,260 |

| Mar. 10 | To Cash A/c (Purchase) | 11 | 450 | ||||

| Mar. 11 | To Cash A/c (Repairs) | 12 | 60 | ||||

| Mar. 28 | To Cash A/c (Advertisement) | 13 | 60 | ||||

| Mar. 31 | To Bank A/c (Rent) | 13 | 90 | ||||

| 1,260 | 1,260 |

Input IGST Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 13 | To Jacob Bros. Ltd. (Purchase) | 12 | 1,200 | Mar. 31 | By Balance c/d | 1,200 | |

| 1,200 | 1,200 |

Output IGST Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 31 | To Balance c/d | 12 | 1,200 | Mar. 31 | By Cash A/c (Sales) | 1,200 | |

| 1,200 | 1,200 |

Output CGST Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 31 | To Balance c/d | 1,020 | Mar. 4 | By Narain Bros. A/c | 11 | 600 | |

| By Cash A/c (Furniture) | 11 | 60 | |||||

| By Cash A/c (Sales) | 13 | 360 | |||||

| 1,020 | 1,020 |

Output SGST Account

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 2020 | 2020 | ||||||

| Mar. 31 | To Balance c/d | 1,020 | Mar. 4 | By Narain Bros. A/c | 11 | 600 | |

| By Cash A/c (Furniture) | 11 | 60 | |||||

| By Cash A/c (Sales) | 13 | 360 | |||||

| 1,020 | 1,020 |

This is all about question 13 Chapter 6 – Unimax. You can check out the following article to better understand:

Ledger balancing or Closing of ledger account | Ledger

You Can also read all the above articles in Hindi on our Hindi Website

Ledger balancing or Closing of ledger account | Ledger – In Hindi

Thanks, Please Like and share with your friends

Comment if you have any doubt in question 13 Chapter 6 – Unimax.

You can also Check out the solved question of other Chapters: –

Advanced Accountancy – Unimax Class 11 – 2021 – Solution.

Part-I

- Chapter No. 1 – Introduction of Accounting

- Chapter No. 2 – Theory Base of Accounting

- Chapter No. 3 – Vouchers and Transactions

- Chapter No. 4 – Journal

- Chapter No. 5 – Goods and Services Tax (GST) : An Introduction

- Chapter No. 6 – Ledger

- Chapter No. 7 – Special Purpose Book – Cash Book

- Chapter No. 8 – Other Subsidiary Books

- Chapter No. 9 – Trial Balance

- Chapter No. 10 – Rectification of Errors

- Chapter No. 11 – Depreciation

- Chapter No. 12 – Provision and Reserves

- Chapter No. 13 – Bank Reconciliation Statement

- Chapter No. 14 – Bills of Exchange

Students may Choose only one part from the Part II and Part III

Part-II

- Chapter No. 15 – Financial Statements (Without Adjustments)

- Chapter No. 16 – Financial Statements (With Adjustments)

- Chapter No. 17 – Accounts from Incomplete Records – Single Entry System

Part-III

- Chapter No. 18 – Introduction to Compurters and Accounting information System

- Chapter No. 19 – Computerised Accounting

- Chapter No. 20 – Accounting Software : Tally

- Chapter No. 21 – Data Base System

- Chapter No. 22 – Concept of Entity and Relationship

You can also Check out the other Books’ Solution: –