Question 11 Chapter 7 of +2-A

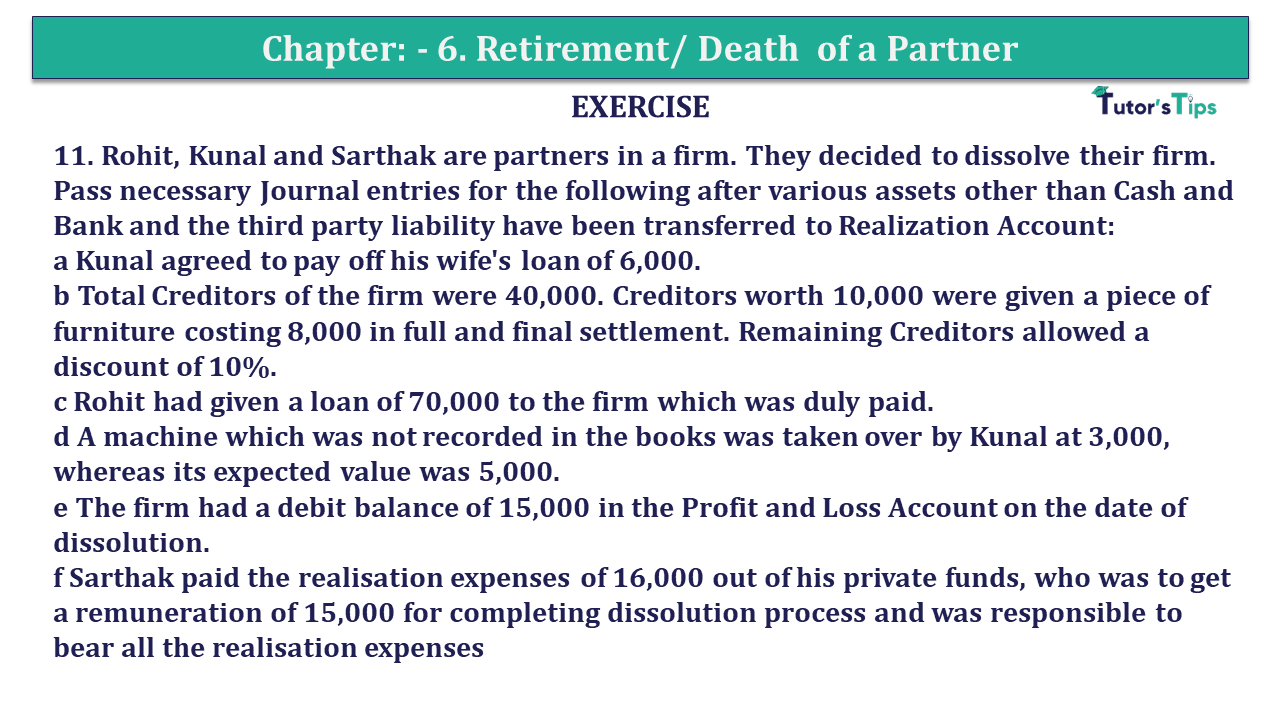

11. Rohit, Kunal and Sarthak are partners in a firm. They decided to dissolve their firm. Pass necessary Journal entries for the following after various assets other than Cash and Bank and the third party liability have been transferred to Realization Account:

a Kunal agreed to pay off his wife’s loan of 6,000.

b Total Creditors of the firm were 40,000. Creditors worth 10,000 were given a piece of furniture costing 8,000 in full and final settlement. Remaining Creditors allowed a discount of 10%.

c Rohit had given a loan of 70,000 to the firm which was duly paid.

d A machine which was not recorded in the books was taken over by Kunal at 3,000, whereas its expected value was 5,000.

e The firm had a debit balance of 15,000 in the Profit and Loss Account on the date of dissolution.

f Sarthak paid the realisation expenses of 16,000 out of his private funds, who was to get a remuneration of 15,000 for completing dissolution process and was responsible to bear all the realisation expenses

The solution of Question 11 Chapter 7 of +2-A: –

| Date | Particulars |

L.F. | Debit | Credit | |

| a | Realization A/c | Dr. | 6,000 | ||

| To Kunal’s Capital A/c | 6,000 | ||||

| (Being Kunal agrees to pay off his wife ′s loan) | |||||

| b | Realization A/c | Dr. | 27,000 | ||

| To Cash A/c | 27,000 | ||||

| (Being Creditors worth Rs30,000 paid off at a discount of 10) | |||||

| c | Rohit’s Loan A/c | Dr. | 70,000 | ||

| To Cash A/c | 70,000 | ||||

| (Being Loan paid by the firm) | |||||

| Bank A/c | Dr. | 1,200 | |||

| To Realization A/c | 1,200 | ||||

| (Being Unrecorded assets realized) | |||||

| d | Kunal’s Capital A/c | Dr. | 3,000 | ||

| To Realization A/c | 3,000 | ||||

| (Being Realization expenses paid by Q) | |||||

| e | Rohit’s Capital A/c | Dr. | 5,000 | ||

| Kunal’s Capital A/c | Dr. | 5,000 | |||

| Sarthak’s Capital A/c | Dr. | 5,000 | |||

| To Profit and Loss A/c | 15,000 | ||||

| (Being Realisation Profit distributed) | |||||

| f | Realization A/c | Dr. | 15,000 | ||

| To Sarthak’s Capital A/c | 15,000 | ||||

| (Being remuneration of Rs15,000 paid for completion of dissolution process) | |||||

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication