Liabilities Ledger account means those specific ledger accounts which are related to that amount which is payable or pending to pay. These amounts are known as Liabilities and Capital.

The Following are the name of the Liabilities and Capital account: –

- Capital

- Bank Loan

- Bank Overdraft

- Loan from ____________. ( Name of any person or institution)

- Debenture

- Trade payables

- Bills payables

- Outstanding Expenses

- Advance received income

- Advance from customers

- All reserves and surplus accounts

- Security Deposited from Employees

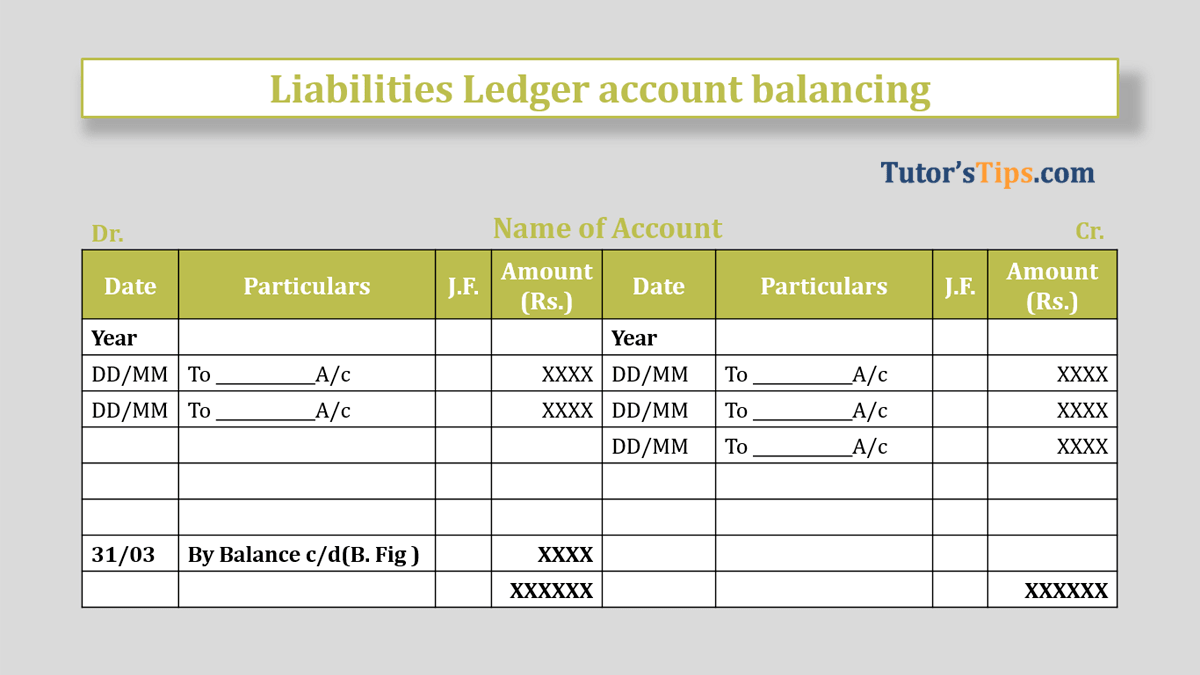

Closing of Liability Ledger account:-

It is also known as Closing of Liability Ledger account for the specific account. The closing of ledger accounts is included in the following steps : –

- 1st Step: Totaling both sides.

- 2nd Step: Writes the total of the largest side on both sides.

- 3rd Step: Subtract the shorter side total from the larger side total.

- 4th Step: Now, Write a balanced amount of larger side which we get after subtracting it from the shorter side on the shorter side of the ledger account.

Note: –

- Liabilities account always has a “Credit balance”

- Liabilities Ledger account balance will always carry forward to the next financial year.

Now we will explain it further with the help of the following illustration.

We will show only transactions related to the particular Liabilities account.

Illustration:

Prepare Bank A/c for the Month of Jan-18.

| Date | Transaction | Amount |

| 01/01/18 | Credit balance in the Bank a/c | 300,000 |

| 08/01/18 | Purchase goods from Ramu and paid with a cheque | 150,000 |

| 22/01/18 | Salary paid to Employees | 175,000 |

| 31/01/18 | Goods sold to Priyanka and payment received by cheque | 250,000 |

Solution:

After posting all the transaction in the journal and then posted it in the ledger we will get ledger account as shown below:

Bank A/c

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 31/01/18 | To Sale a/c | 250,000 | 05/01/18 | By Balance b/d | 300,000 | ||

| 12/01/18 | By Purchase a/c | 150,000 | |||||

| 21/01/18 | By Salary a/c | 175,000 | |||||

2nd Step: Writes the total of the largest side on both sides. So,

Bank A/c

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 31/01/18 | To Sale a/c | 250,000 | 05/01/18 | By Balance b/d | 300,000 | ||

| 12/01/18 | By Purchase a/c | 150,000 | |||||

| 21/01/18 | By Salary a/c | 175,000 | |||||

| 625,000 | 625,000 |

Total of the debit side(Largest side) subtracted from the credit side total(shortest)

we got 400000 – 0 = 400,000/-

4th Step: Now, Write balance amount of larger side which we get after subtracting it from the shorter side on the shorter side of the ledger account as shown below.

Bank A/c

| Date | Particulars | J.F. | Amount | Date | Particulars | J.F. | Amount |

| 31/01/18 | To Sale a/c | 250,000 | 05/01/18 | By Balance b/d | 300,000 | ||

| 12/01/18 | By Purchase a/c | 150,000 | |||||

| 21/01/18 | By Salary a/c | 175,000 | |||||

| 31/03/18 | By balance c/d (B. Fig) | 375,000 | |||||

| 625,000 | 625,000 |

Thanks for reading the topic of Income Ledger account balancing, please comment your feedback whatever you want.

Or

If you have any question please ask us by commenting.

Please Share and spread it