It is very easy to remember the journal entry for passing exams. You can remember it if you want to do so. But we always recommend that you have to understand the application of rules to the journal entry. Before passing the Journal Entry with the golden rules of accounting, you have to know the meaning of Discount Received, we have explained the meaning of discount and different type of transactions related to discount received in this article.

The Meaning of Discount Received:

The Discount Received is that amount which is paid less to the supplier for the purchase of goods from goods selling price. So, it is the gain of the buyer of the goods, according to Nominal rule, this amount will be credited in the books. This is also known as revenue or indirect income of the business.

For Example,

The Purchase price of the product is Rs 1,500/- but the Retailer offers us only for Rs.1,350/- after deducting a 10% discount. here the amount of discount received is Rs 150/-(1,500 – 1,350).

Journal Entry of Discount Received :

Now, We will discuss the Journal Entry for Discount Received in three different cases shown as following: –

1. Discount received and the net amount paid or the total amount payable is given:

Example No. 1:

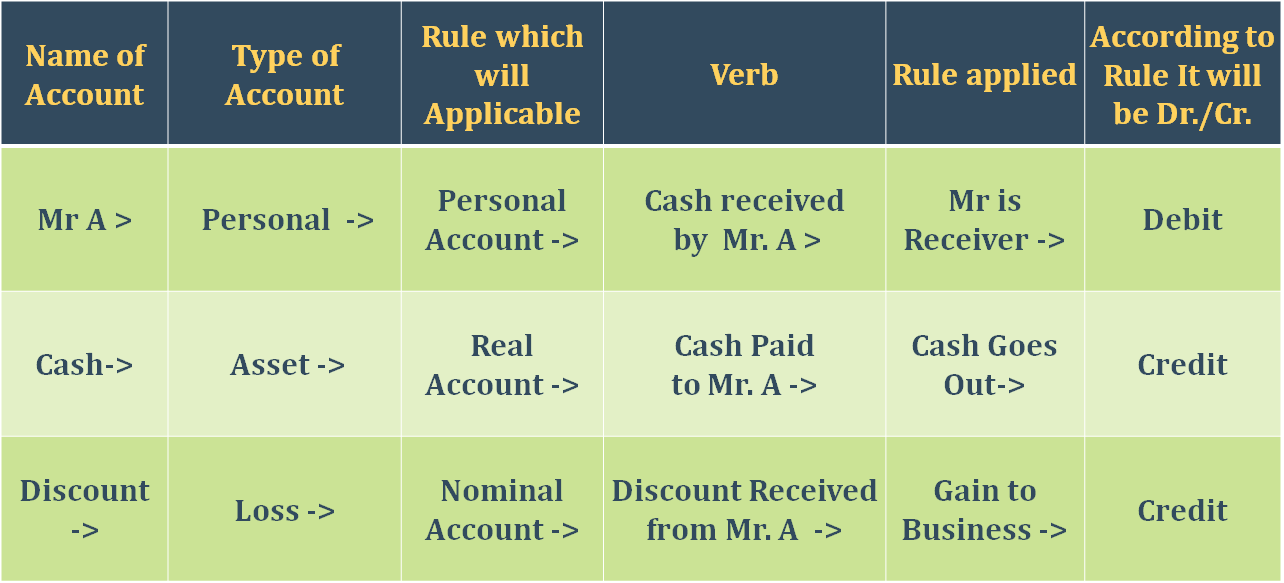

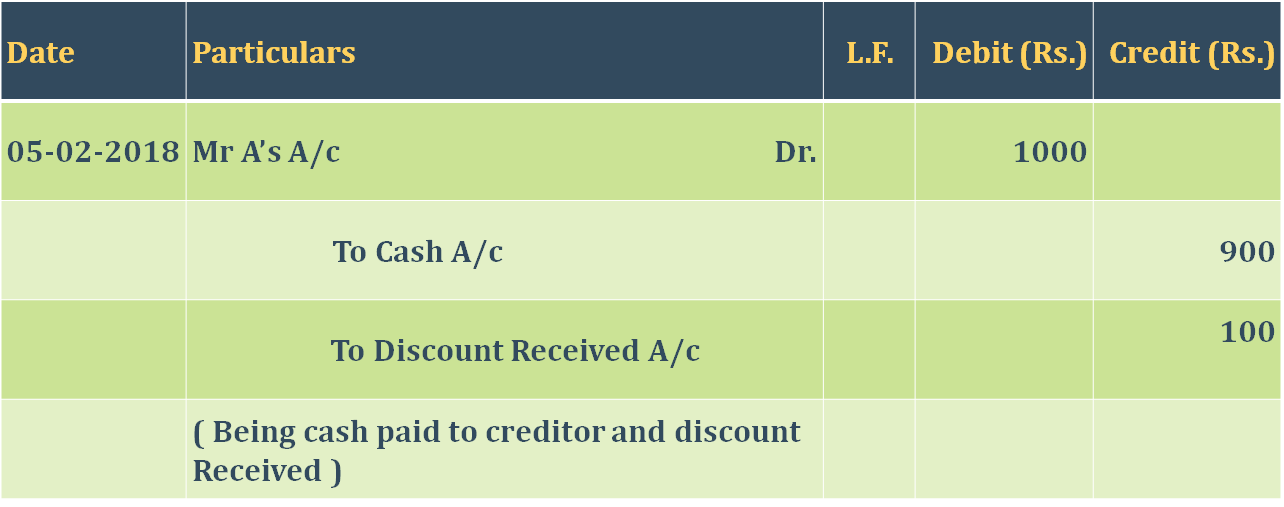

05/02/2018 Amount paid to Mr. A of Rs 900/- and he allowed a discount of Rs 100/-.

Or

Example No. 2:

05/02/2018 The amount payable to Mr. A of Rs 1,000/- and he allowed a discount of Rs 100/-.

Both Journal Entry for Discount Received are the same and treated as the following:

2. The Percentage of discount received and the total amount payable is given:

Example No. 3:

05/02/2018 The amount payable to Mr. A of Rs 1,000/- and he allowed a discount @ 10%.

In this transaction, you have to calculate discount first as the following:

1000*10/100 = 100/-

Journal Entry remains the same as above.

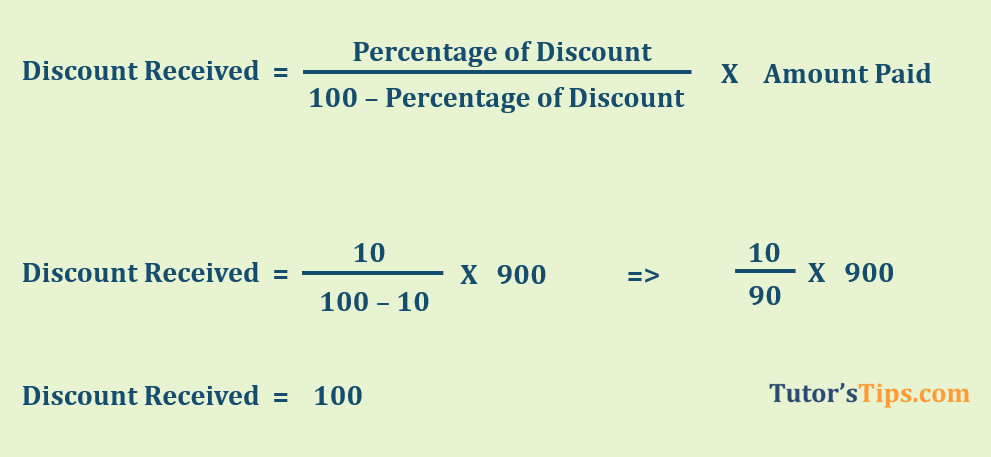

3. The percentage of discount received and the total amount paid is given:

Example No. 4:

05/02/2018 Amount paid to Mr. A of Rs 900/- and he allowed a discount @ 10%.

In this transaction, you also have to calculate the amount discount first as the following:

if the amount paid is given then we have to use the following formula to calculate the amount of discount the same as we calculate the discount allowed in the previous topic.

Percentage of Discount/100 – Percentage Rate of Discount (we will show you it in the Image below)

Journal Entry remains the same as above.

Check out Financial Accounting Books @ Amazon.in