Discount or loss on issue of debentures is the types of capital loss for the business. we will discuss the meaning of these both terms separately shown as follows:

What is the Discount on the issue of Debentures?

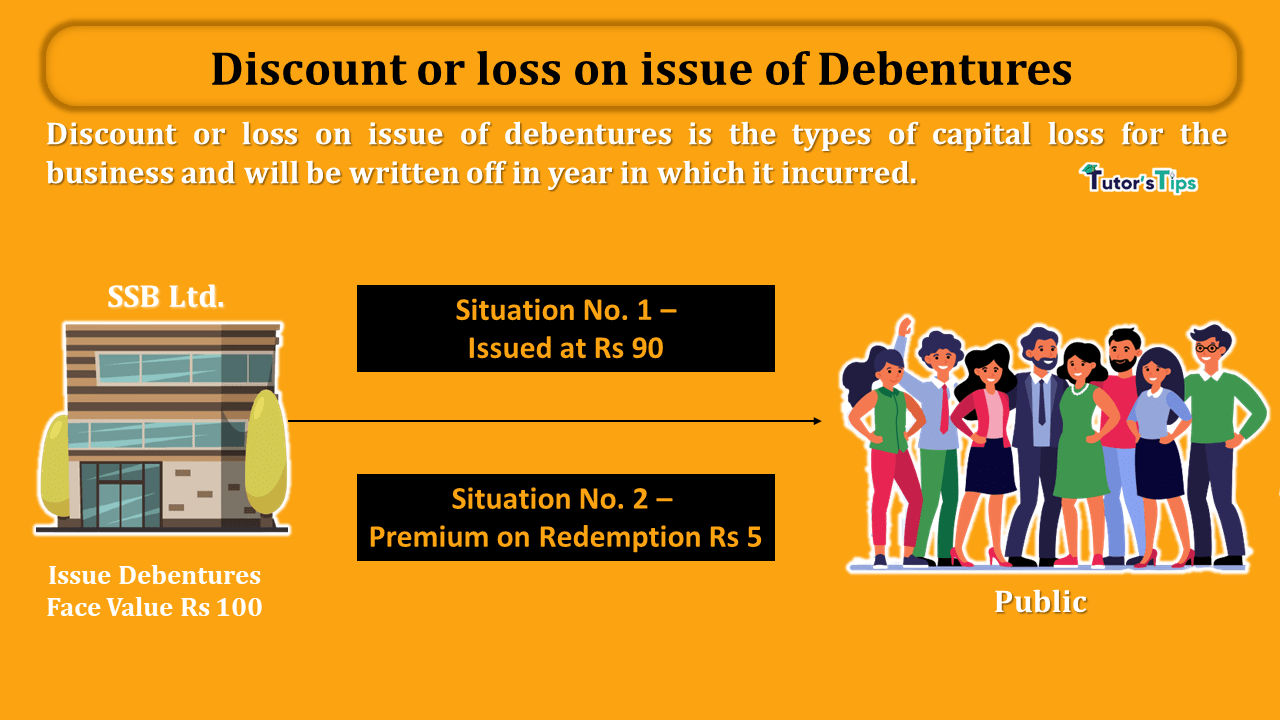

In the situation where the debentures are issued on the value which is less than the face(nominal) value then the amount of difference between the face value and issue value is known as a discount on the issue of debentures.

For Example:

ABC Co. limited issued 10,000 debenture face value of Rs 100 at a discount of 10% of face value. Calculate the amount of the Discount on the issue of the debentures.

Solution:

Discount on issue of debenture(per deb.) = Face Value * Rate of Discount

= 100 * 10%

= Rs 10/- (per deb.)

The total amount of Discount = Number of Deb. * Amount of Discount (per deb.)

= 10,000 * 10

= Rs. 1,00,000/-

check journal entries for discount on the issue of debentures:

Issue of Debenture – Methods and accounting treatment

What is the loss on issue of debentures?

In the situation where the debentures are issued with the promise or condition of that the issued debentures will be redeemed at a premium then the amount of premium promised will be treated as a loss on the issue of debentures. it can be claimed after the allotment of the debentures against the security premium reserve or profit for the year.

For Example:

ABC Co. limited issued 10,000 debenture face value of Rs 100 at a premium on redemption of 5% of face value. Calculate the amount of the loss on the issue of the debentures.

Solution:

Loss on the issue of debenture(per deb.) = Face Value * Rate of Premium of Red.

= 100 * 5%

= Rs 5/- (per deb.)

The total amount of loss = Number of Deb. * Amount of loss (per deb.)

= 10,000 * 5

= Rs. 50,000/-

check journal entries for loss on the issue of debentures:

Issue of Debentures from the point of view of Redemption

How to write off the Discount or loss on issue of debentures?

The discount or loss on issue of debentures can be written off in the year in which these are incurred. It means the year in which debentures were issued. It can be written off from the following accounts’ balance:

- Security Premium Reserve account

- Profit or Loss account

Firstly it will be written off from the amount of discount or loss on issue of debentures from the Security Premium Reserve account and if the balance of the Security Premium Reserve account is short or less then the amount of discount or loss then the balance amount will be written off from the profit or loss account.

The Accounting treatment of the writing off the discount or loss on issue of debentures.

I am explaining treatments of the discount or loss on issue of debentures in the journal as well as a balance sheet. This is shown as follows:

Journal entries

| Date | Particulars |

L. F. | Debit | Credit | |

| Security Premium Reserve A/c | Dr. | ***** | |||

| To Discount or loss on issue of deb. A/c | ***** | ||||

| (Being the amount of discount or loss on issue of deb. is written off from the security premium account up to the extent of the balance of the account) | |||||

| Profit or Loss A/c | Dr. | ***** | |||

| To Discount or loss on issue of deb. A/c | ***** | ||||

| (Being the balance amount of discount or loss on issue of deb. is written off from the profit and loss account (if any)) | |||||

How shown in the balance sheet:

The amount of the discount or loss on the issue of the debentures will be written off in the year in which it is incurred. so it will be shown in the note to balance sheet only. The Notes to balance sheet is shown as following:

Balance Sheet(Extract)

| Particulars |

Note No. | Amount | |

| 1. | Equity and Liabilities | ||

| Shareholders’ Funds | |||

| Reserves and Surplus | * | **** | |

Note to Accounts:

1. If written off from Security Premium Reserve Account only.

| Particulars |

Details | Amount | |

| 1. | Reserves and Surplus | ||

| Security Premium Reserve A/c | **** | ||

| less: Discount or loss on issue of Debentures | *** | ||

| *** | |||

2. if written off from Security Premium Reserve Account and Profit or loss account also:

| Particulars |

Details | Amount | |

| 1. | Reserves and Surplus | ||

| Security Premium Reserve A/c | *** | ||

| less: Discount or loss on issue of Debentures | *** | ||

| 0 | |||

| Profit or Loss A/c | *** | ||

| less: Discount or loss on issue of Debentures | ** | ||

| ** | |||

Thanks for reading the topic.

please comment your feedback whatever you want. If you have any questions, please ask us by commenting.

References: –