Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

The accounting treatment in the case of Death of a Partner is the same as the retirement of a partner.

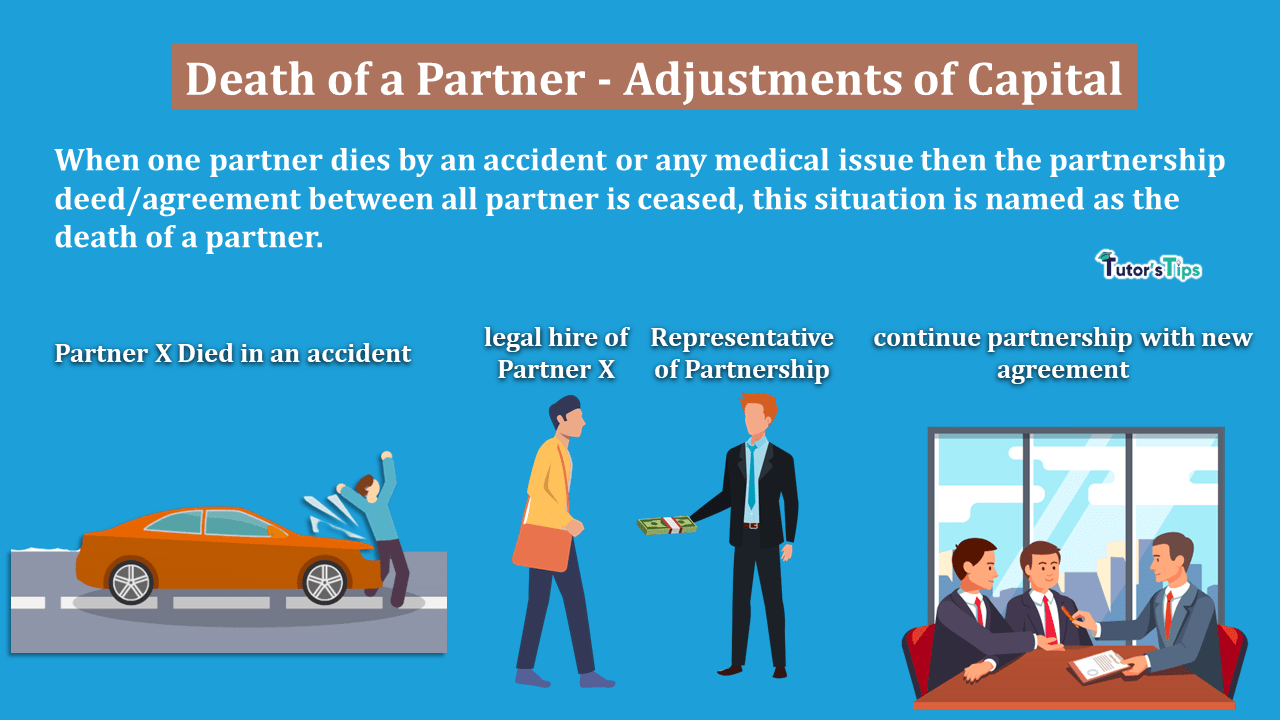

When one partner dies by an accident or any medical issue then the partnership deed/agreement between all partners is ceased this situation is named as the death of a partner. The partnership deed is ended, but the partnership firm can continue its operation if the remaining partners want to continue the partnership firm.

When a partner dies, His legal heirs will be eligible to collect his due amount from the firm. it included capital, goodwill, and profit share of the deceased partner. The total amount becomes due to the heirs of the deceased partner will be calculated as per the retirement of the partner. In both cases, one partner left the partnership firm. In the retirement case, it is planned but in the death cases, it will happen. All the conditions or amounts are payable to heirs in case of death of a partner already written in the partnership deed. So, it will be treated as per the partnership deed. The commonly the legal heirs of the deceased partner are entitled to the following: -

and the following amount will be debited to his account.

There will be the numbers of effects affecting the partnership and some of them are shown as follows: -

There should be a new partnership Deed/agreement between remaining partners with all of the new terms and conditions acceptable to all partners. The old agreement will be abolished.

As per the agreement between the remaining partners, the Remaining partner has to pay to retire partner his share of capital and goodwill in the firm as per his share of profits of the firm.

The shares of the reserve and accumulated profit/loss will also be paid to all partners including heirs of the deceased partner. Accumulated profit/loss will be distributed in the old profit sharing ratio of all partners because these items are related to the period before retirement.

At the time of death of any partner, if the remaining partners decide to know the true financial position of the firm then there will need to reevaluate all assets and liabilities of the firm.

At the time of the retirement of the parter Following adjustment will take into consideration and these all are already explained in the previous articles, So please click on the name and check out these all articles one by one.

Thanks for reading the topic.

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

The accounting treatment in the case of Death of a Partner is the same as the retirement of a partner. What is the Death of a Partner : When one partner dies…

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Advanced Financial Accounting.

Yes — this page includes a short interactive quiz so you can check your understanding straight away.