Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Dividing the activities of the business related to cash and cash equivalents is known as Classification of Cash Flow Statement.

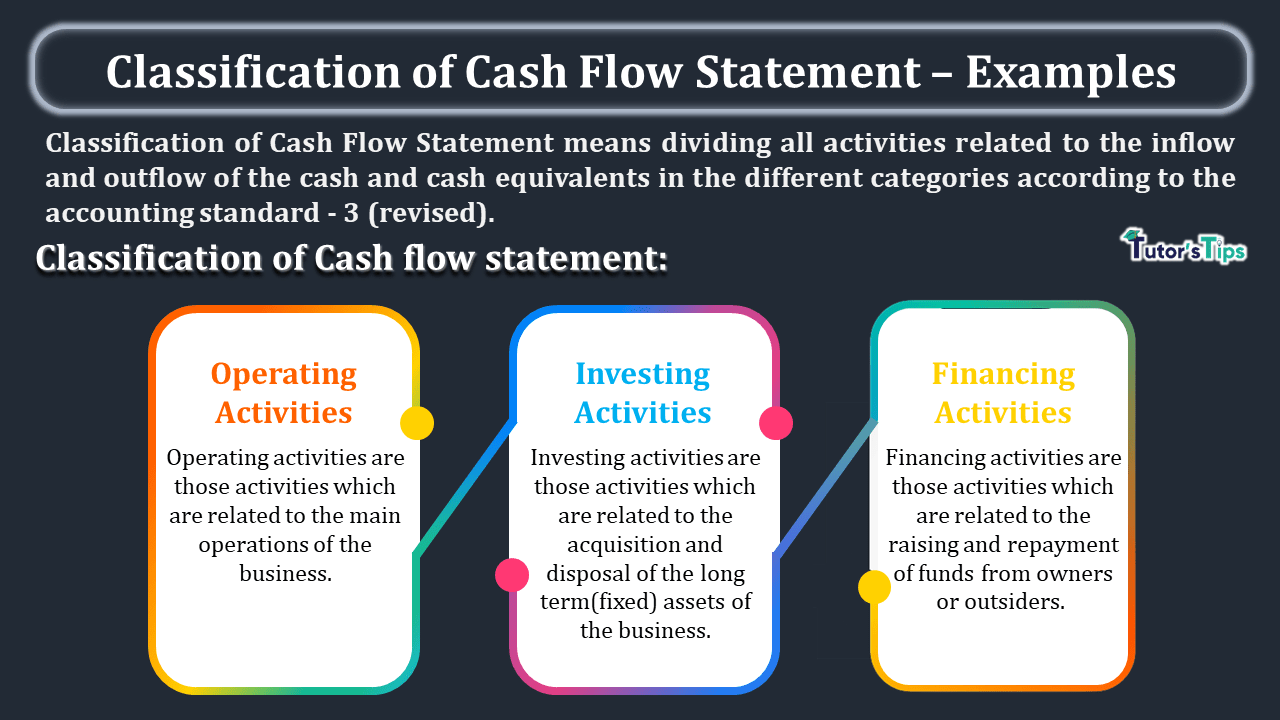

Classification of Cash Flow Statement means dividing all activities related to the inflow and outflow of the cash and cash equivalents in the different categories according to the accounting standard - 3 (revised).

The activities of the business which are related to the cash and cash equivalent are classified as follows:

Operating activities are those activities that are related to the main operations of the business. The main operations mean the operations from which the business earn their principle revenue by spending the amount on the expenditure related to the principle revenue.

The main source of cash inflow in the operating activities is from the selling of final product (it may be cash or in the form of a received from the debtors) and cash outflow on the purchase of raw material and payment of various expenses which are required to make a final product. check out the examples of the cash inflow and outflow in the operating activities as follows:

We can divide the examples into the two types of companies shown as follows:

1. For Non-financial Companies: -

2. For Financial Companies: -

We can divide the examples into the two types of companies shown as follows:

1. For Non-financial Companies: -

2. For Financial Companies: -

Investing activities are those activities that are related to the acquisition and disposal of the long-term (fixed) assets of the business. In other words, These activities include the purchase and sale of fixed assets i.e. plant and machine, building, land, furniture, and investment(Not a current investment).

We can divide the examples into the two types of companies shown as follows:

Financing activities are those activities that are related to the raising and repayment of funds from owners or outsiders. In other words, These activities include the issues of share capital, debenture, raising bank loan, buyback of shares capital, the redemption of debentures, and repayment of loans.

We can divide the examples into the two types of companies shown as follows:

Thanks for reading the topic.

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

Dividing the activities of the business related to cash and cash equivalents is known as Classification of Cash Flow Statement. What is the Classification of…

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Advanced Financial Accounting.

Yes — this page includes a short interactive quiz so you can check your understanding straight away.