Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

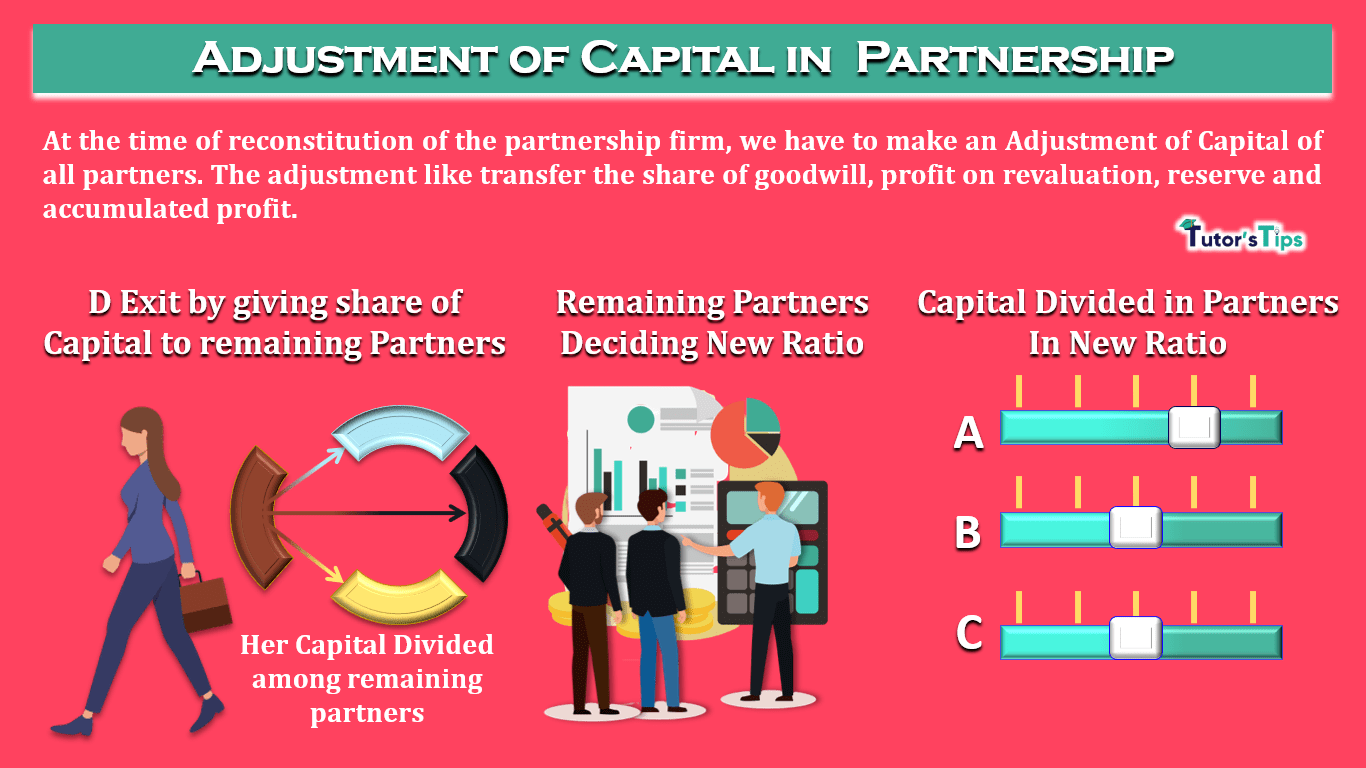

At the time of the reconstitution of the partnership firm, we have to make an Adjustment of Capital of all partners. The adjustment like transfer the share of goodwill, profit on revaluation, reserve, and accumulated profit.

The adjustment of capital in partnership means, making the share of capital according to the new profit sharing ratio as per decided by the partners. If there will be a required more amount of capital or less amount of capital as compared with the amount already invested in the partnership then partners will introduce or withdrawal their share of capital in cash respectively.

The required balance of the partner's capital account is changed because at the time of reconstitution of partnership firm the new profit sharing ratio is calculated and All old reserve or accumulated profit/loss, the difference of revaluation of assets and liabilities are divided among all partners (old partners in case of admission of new partner) in their old ratio. if one partner sacrifices his share of profit then he will be paid off by all other gaining partners. So, His balance of the capital account will be increased and will be more than the balance required as per his share of profit in the firm then he will withdrawal is share of capital to the extent to meet the requirement of capital only.

The journal entries of the balance of reserve or accumulated profit/loss account and revaluation of assets and liabilities already discussed in the previous articles. Please check by clicking in the link attached on their name. In this article, we will just discuss the journal entries of adjustment of capital shown as follows: -

| Date | Particulars |

L. F. | Debit | Credit | |

|---|---|---|---|---|---|

| (i) For excess capital withdrawn by the partner | |||||

| Partners' Capital A/c | Dr. | XXXX | |||

| To Cash/Bank A/c | XXXX | ||||

| (Being excess capital withdrawn by the partners ) | |||||

| (ii) For the amount of capital introduced by the partner | |||||

| Cash/Bank A/c | Dr. | XXXX | |||

| To Partners' Capital A/c | XXXX | ||||

| (Being adjustment made for transfer the balance of revaluation a/c to retiring partners' capital/current a/c) | |||||

Thanks for reading the topic

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

At the time of the reconstitution of the partnership firm, we have to make an Adjustment of Capital of all partners. The adjustment like transfer the share of…

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Advanced Financial Accounting.

Yes — this page includes a short interactive quiz so you can check your understanding straight away.