Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

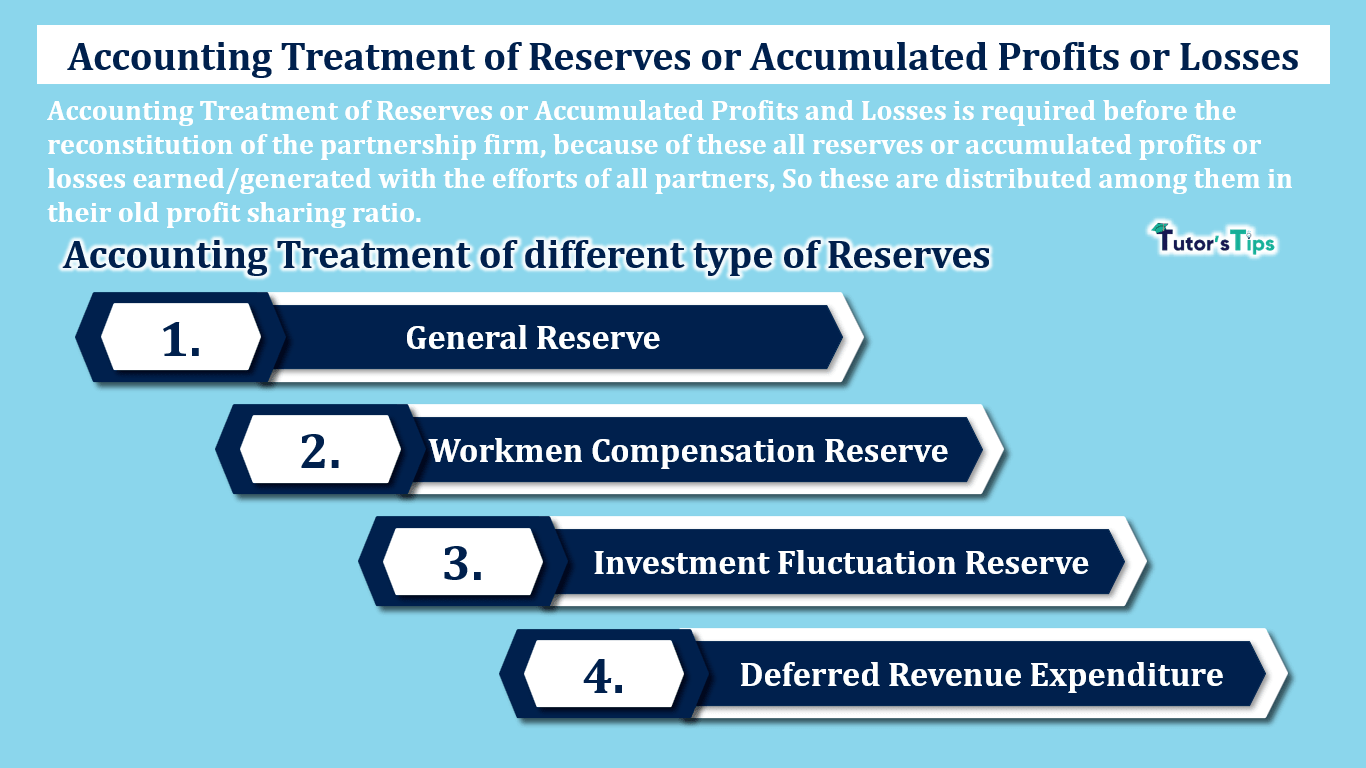

Accounting Treatment of Reserves or Accumulated Profits and Losses is required before the reconstitution of the partnership firm, because of these all reserves or accumulated profits or losses earned/generated with the efforts of all partners, old partners(in case of admission) or remaining Partners( in case of death or retirement) and these are distributed among them in their old profit sharing ratio.

A reserve or Accumulated Profits or Losses refers to the share of profit saved by the business/firm for future growth or expansion and to handle the situation of losses in the future.

https://tutorstips.com/reserve/

The total amount of Reserves or Accumulated Profits or Losses exists in the books as belonging to the partner in their old ratio. So, we have to distribute these amounts among all partners in their old ratio by crediting the share of the total amount to the particular partners capital account(in case of fluctuating) or Current Accounts (in case of fixed capital) before reconstitution of the partnership firm

The Journal Entries are shown as per the type of the reserve as follows: -

In this case, the following two journal entries are posted: -

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| (i) Journal Entry for Reserves Accumulated Profits: | |||||

| Reserves A/c | Dr. | XXXX | |||

| Profit or Loss A/c (Cr. Balance) | Dr. | XXXX | |||

| To Partners' Capital (Current) A/c | XXXX | ||||

| (Being adjustment of reserve made in old profit sharing ratio.) | |||||

| (ii) Journal Entry for Accumulated Losses: | |||||

| Partners' Capital (Current) A/c | Dr. | XXXX | |||

| To Profit or Loss A/c (Dr Balance) | XXXX | ||||

| (Being adjustment of reserve made in old profit sharing ratio.) | |||||

The Workmen Compensation Reserve is created to meet the liabilities on the account of compensation to employees in the accident cases. So, as per the meaning of workmen compensation reserve, it will be paid only in the case of an accident it means it may be or may not be paid. The firm can have funded in this reserve so it can be treated as follows: -

In the case, Where no claim exists against the reserve the full amount will be distributed among the partners in the old profit sharing ratio.

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Workmen Compensation Reserve A/c | Dr. | XXXX | |||

| To Partners' Capital (Current) A/c | XXXX | ||||

| (Being adjustment of reserve made in old profit sharing ratio.) | |||||

In the case, Where claim exists against the reserve then the treatment of the amount of reserve are different as per the following cases: -

(a) Where estimate amount of claim is equal to the total amount of Workmen Compensation Reserve: -

The total amount of reserve will be transferred to the Provision for the workmen compensation claim.

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Workmen Compensation Reserve A/c | Dr. | XXXX | |||

| To Provision for Workmen Compensation Claim A/c | XXXX | ||||

| (Being amount of reserves transferred to the provision account.) | |||||

(b) Where estimate amount of claim is less than the total amount of Workmen Compensation Reserve: -

The total amount of claim against reserve will be transferred to the Provision for the workmen compensation claim and the balance amount will be distributed among the partners in their old profit sharing ratio.

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Workmen Compensation Reserve A/c | Dr. | XXXX | |||

| To Provision for Workmen Compensation Claim A/c | XXXX | ||||

| To Partners' Capital (Current) A/c | XXXX | ||||

| (Being amount of reserves transferred to provision account and balance amount distributed among the partners.) | |||||

(c) Where estimate amount of claim is more than the total amount of Workmen Compensation Reserve: -

The total amount of claim against reserve will be transferred to the Provision for the workmen compensation claim and the balance amount will be distributed among the partners in their old profit sharing ratio.

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Workmen Compensation Reserve A/c | Dr. | XXXX | |||

| Revaluation A/c | Dr. | XXXX | |||

| To Provision for Workmen Compensation Claim A/c | XXXX | ||||

| (Being amount of reserves and balance amount from the revaluation equal to the amount of claim transferred to the provision account.) | |||||

The huge amount of revenue expenditure spent on any type of work which was not claimed in the related financial year and does not have any resealable value but provide benefit in future accounting year also is known as Deferred Revenue Expenditure. The advertisement is an example of these type of assets.

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Partners' Capital (Current) A/c | Dr. | XXXX | |||

| To Deferred Revenue Expenditure a/c | XXXX | ||||

| (Being Deferred revenue expenditure written off in old profit sharing ratio.) | |||||

Thanks for reading the topic

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

Accounting Treatment of Reserves or Accumulated Profits and Losses is required before the reconstitution of the partnership firm, because of these all reserves…

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Advanced Financial Accounting.

Yes — this page includes a short interactive quiz so you can check your understanding straight away.