Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

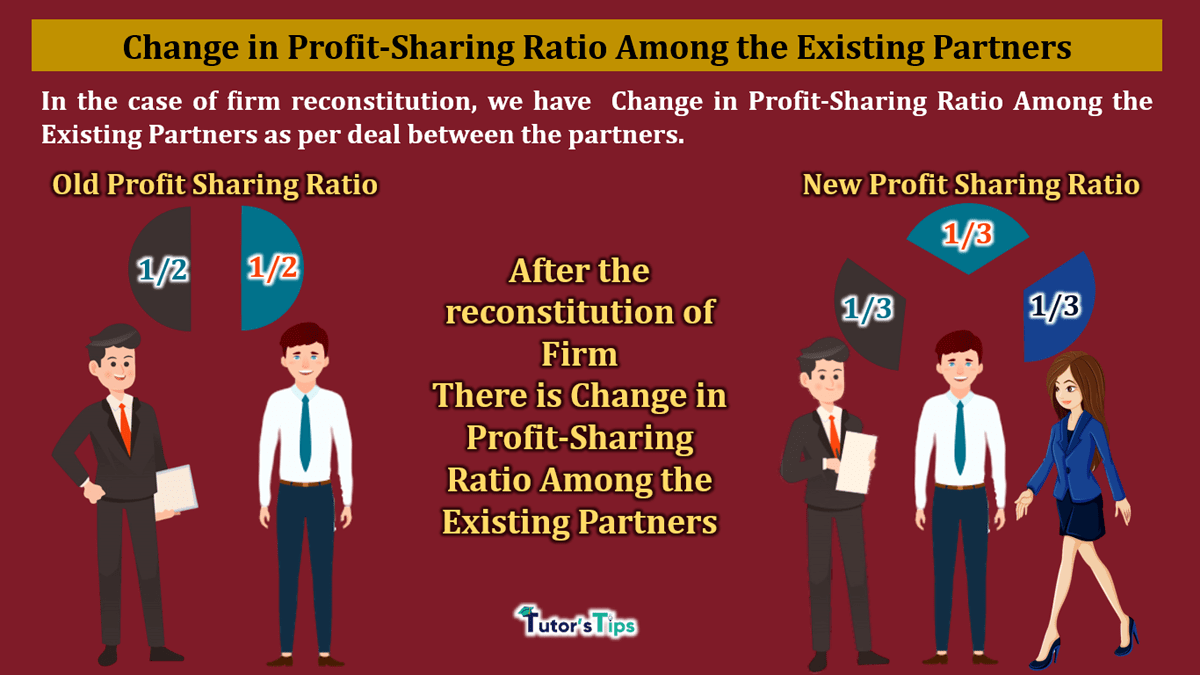

The partnership means when two or more than two persons are agreed to do business together and share of the profits/losses of the business in an equal or already specified ratio. In the case of firm reconstitution, we have Change in Profit-Sharing Ratio Among the Existing Partners as per deal between the partners.

"Partnership is the relation between persons who have agreed to share the profits of a business carried on by all or any of them acting for all"

-Section 4 of the Indian Partnership Act, 1932

Change in Profit-Sharing Ratio Among the Existing Partners means when one or more from the existing partners wants more share in the business profit then they mutually decide to change their profit sharing ratio from the earlier decided profit sharing ratio. This process is known as a reconstitution of the firm.

In this process, who want more share he will gain an equal amount to the sacrificing amount of another partner(s). So to calculate the amount of additional capital required to acquire the more share of profit, we have to calculate the gaining/sacrificing ratio of the partners. To calculate the gaining/sacrificing ratio we have to apply the following formula: -

Sacrificing/Gaining Share = Old Share - New Share

(both shares will be related to the partner whose Sacrificing/Gaining Share is calculating)

The result got from the above calculation, will be treated as sacrificing or gaining share as shown follows: -

A and B are the partner in the A&B Co. ltd. The shared profit of the firm in the ratio 2:1 but now they want to more the future profit in the equal ratio. So, you have to calculate the sacrificing and gaining ratio of both partners.

Sacrificing/Gaining Share = Old Share - New Share

| Sacrificing/Gaining Share of A | = | 2 | - | 1 |

| 3 | 2 |

| Sacrificing/Gaining Share of A | = | 4 - 3 |

| 6 |

| Sacrificing/Gaining Share of A | = | 1 | Sacrificing |

| 6 |

| Sacrificing/Gaining Share of B | = | 1 | - | 1 |

| 3 | 2 |

| Sacrificing/Gaining Share of B | = | 2 - 3 |

| 6 |

| Sacrificing/Gaining Share of B | = | - |

1 | Gaining |

| 6 |

There are five types of adjustment are made for the change in Profit-Sharing Ratio. These are shown below and every adjustment is explained with the help of illustration in a separate article.

First of all, To make any type of adjustment, we have to calculate the sacrificing/gaining ratio. With the help of this ratio, we will calculate the total amount of other adjustments. Both these ratios are explained further in the next article.

Goodwill means when one business acquired in a whole or some percentage of share of another business for the amount which is more than the total assets of that business. That amount of difference which is paid extra is known as goodwill. It is a tangible asset.

So, The gaining partner(s) have to pay the amount of goodwill to sacrifice partner(s). To pay this amount we will make the adjustment entries or make a cash payment to the sacrificing partner(s).

The gaining partner(s) will bring the share of goodwill equal to the his gaining share in the firm profit.

A reserve refers to that proportionate amount of net profit or surpluses which is retained for the future payments. In other words, the retention of the profit which is not for any known liability.

This amount is related to the past year that's why the sacrificing partner has a right on it. So, the Reserves and Accumulated Profits and Losses are divided in the old profit sharing ratio.

As per the accounting standard, we will show the all assets in the accounting books on original(cost) value but some of our assets will appreciate and some of them will have less market value as compared with book value.

So that's why we have to calculate the true/market value of the assets and liabilities and then distribute is amount of difference among the partners.

The adjustment of capital is must because the gaining partner(s) has to invest more to get the more profit share in the firm. So, the partner will bring the required amount of capital as per his(their) gaining Ratio.

and Sarcificing Partner(s) will withdrawal his(their) capital from the business because after reconstitution he(they) will have less share of profit that's why he(they) will invest as the share of profit in the business.

Thanks for reading the topic.

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

The partnership means when two or more than two persons are agreed to do business together and share of the profits/losses of the business in an equal or…

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Advanced Financial Accounting.

Yes — this page includes a short interactive quiz so you can check your understanding straight away.