The types of Preference Shares are depended on the predefined terms and conditions at the time of the issue of preference shares.

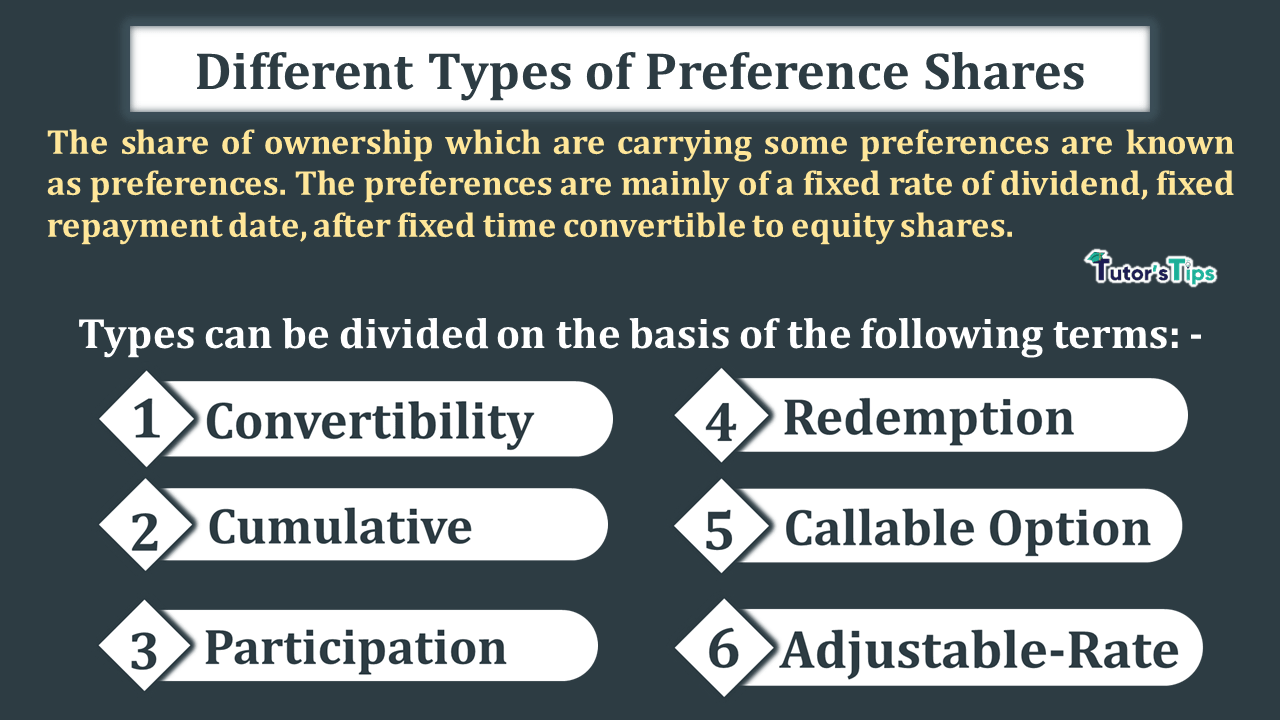

The shares of ownership issued in the share market with some predefined preferences are known as the Preference Shares. The shares of ownership which are carrying some preferences are known as preferences. The preferences are mainly of a fixed rate of dividend, fixed repayment date, after fixed time convertible to equity shares. The dividend of the preference shareholders is paid before the dividend on equity shares.

Types of Preference Shares

Preference share can be divided into 6 types on the basis of the following terms: –

1. Convertibility

The preference shares can be convertible into equity share capital if these are issued with the predefined conditions at the time of the issue of shares. These are maybe convertible or non-convertible.

Convertible Preference Share:

Convertible Preference shares are those which are issued on the predefined condition of conversion of these shares into equity share after some fixed period of time.

Non-Convertible Preference Share

Non-convertible Preference shares are those which do not have the predefined right of conversion of these shares into equity share. These shares are paid off after a fixed period of time.

2. Cumulative

The Cumulative preference shares mean when a business can not pay the dividend to the preference shareholders due to incurred loss in any financial year then the amount of dividend will be cumulated and will be paid in the upcoming profitable financial years.

Cumulative Preference Share

Cumulative Preference shares are those which has predefine right to the cumulation of dividend on preference shares capital.

Non-Cumulative Preference Share

Cumulative Preference shares are those which do not has predefine right to the cumulation of dividend on preference shares capital.

3. Participation

Participation means the right to participate in the distribution of remaining profit after payment of the dividend to the equity shareholder.

Participating Preference Share

Participating Preference Shares are those which have the right to participate in the distribution of profit which is remaining after the payment made to equity shareholders.

Non-Participating Preference Share

Participating Preference Shares are those which do not have the right to participate in the distribution of profit which is remaining after the payment made to equity shareholders.

4. Redemption

Redemption means making the payment to the shareholder after a fixed period of time which is already defined at the time of issue.

Redeemable Preference Share

The preference shares which have a predefined right to redeem after the already fixed maturity date (the maximum limit of up to 20 years from the date of issue) or by giving prior notice to the shareholders.

Irredeemable Preference Share

Irredeemable Preference Shares are those whose amount of capital total value of preference shares) will be paid by the business at the time of winding up.

5. Callable Option

Callable Preference Shares are those on which a business has the right to call for the buyback at any time.

6. Adjustable-Rate

The adjustable-rate Preference Shares are those whose rate of dividend is not fixed and it will depend on the current interest rate in the market.

Thanks for reading the topic.

please comment your feedback whatever you want. If you have any questions, please ask us by commenting.

References: –